Frank Partnoy wrote a fascinating opinion piece in yesterday’s FT about the coming world of smaller banks.

If you’re not familiar with Mr. Partnoy, he is a Professor at the University of San Diego but, more importantly, the author of many books analysing the whys and wherefores of the financial markets with “Infectious Greed” and “F.I.A.S.C.O” being two of the most notable.

He’s well worth reading if you get a chance.

Frank’s article yesterday talks about the age of the big bank being over, as too many staff and inefficiency exists in their system.

He asks the question: “How many people does it take to operate a modern bank and how much should such a bank’s shares be worth?” and answers it by saying that “in the future, improved technology will reduce the number of human beings needed to allocate capital, as it has done in other service industries … contrast the employment numbers for banks and technology firms. HSBC and Google obviously differ in substance but both companies are focused on innovation and service, and also have roughly similar market capitalisations. The striking difference is that Google generates these numbers with fewer than 30,000 employees – not even as many people as HSBC is laying off.”

This led me to beg the question: who generates more value and how?

Frank is right to equate banks to technology firms, as many of them are just that. John Reed, the CEO of Citigroup in the 1980s, said that “banks are just bits and bytes”, a quote I use regularly in all my presentations and on this blog.

If banks are just bits and bytes, then why are they so excessively over-manned.

Well, it’s obvious I guess: because they have branches.

Banks are large-scale retailers with many stores that serve consumers and businesses.

Without that store network, banks would obviously be able to run as pure tech machines, and some already are and some will.

I regularly cite firms like Chi-X, ING Direct and others as firms that are getting the technology platforms and processes right.

And maybe one of the best examples is eBank, in Japan, who presented in 2009 that their bank supports over three million customers with just 193 staff.

15,000 customers per member of staff is the dream for an ultimately automated bank.

Right now, those numbers for most banks would be more like 1,500 customers or less per staff member.

Equally, revenues and profits per employee should be more akin to tech firms than current banks.

But this is predicated on the basis that the banks have no branches and therefore need far fewer people … and banks have not let that paradigm shift happen yet.

It is why so many new entrants – like Banksimple and Movenbank – are moving into banks territory on the basis of fully automated offers, as the banks have left that competitive space wide open.

Like book retailers, music retailers, holiday retailers and more, financial retailers will start to feel the full force of the technology shift of consumers to remote banking via mobile internet.

And what does that mean for a bank?

That they should be more like Google.

No.

Google has around 23,000 employees worldwide and nearly all of them are developers.

If Frank Partnoy thinks that all of the world’s banks can move to being pure development shops, then think again.

Banks have to offer direct customer support through people, as they are service companies.

Google is not a service company – it is a pure technology play.

I don’t see an 0800 number to call when my Google search goes wrong, but I need that when my payment is messed up or my payment card hasn’t arrived.

This is why I would contend the more salient model for a bank to emulate, and most banks agree, is Apple.

Apple has stores.

They have cool stores.

They have genius bars for advice.

They have great staff and highly automated point of sale.

They are engaging in store and online.

Their user experience is second to none.

Sure, they have issues – all firms do – but Apple wouldn’t be the world’s most valuable company – their market cap exceeded Exxon’s for the first time this week to make them the most valuable company in the world – if they weren’t doing something right.

And the thing about Apple is that they cover all the bases – they are developers, deployers, distributors and drivers of consumer technology – just as most banks are for finance.

That is why banks need to model their future on Apple.

Taking the Apple model, their stores need to be re-energised to be cool and engaging.

The number of stores must be reduced to a tenth of today’s numbers – would Apple really have a store on every main street? – which will reduce staff numbers by similar levels.

Their online, mobile internet services have to be so easy and engaging to operate, that customers are more comfortable dealing with a bank through these remote services than with any other, even for complex requirements.

Then banks will absolutely realise their value and achieve Frank’s vision of a world of bank efficiencies.

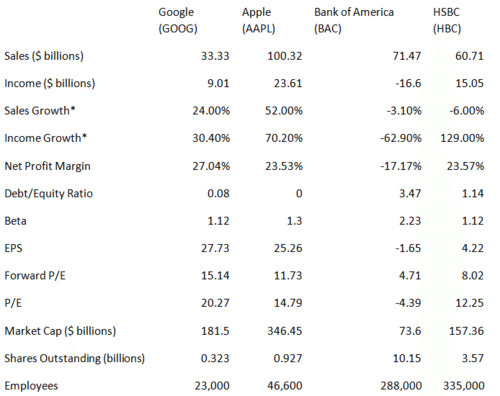

And just in case you think the numbers aren’t as damning as Frank’s opinion piece opines, here’s a direct comparison of Apple, Google, Bank of America (the Banker Magazine’s #1 Bank in the World 2011) and HSBC (doubleclick image for larger chart):

The last line speaks volumes:

- Google generates around $1.5m in revenue and $391,000 income per annum per employee;

- Apple generates over $2m revenue and $513,000 ncome per annum per employee; whilst

- Bank of America generates under $250,000 revenue and almost $60,000 loss per employee per year; and

- HSBC makes $181,000 revenue and just $44,000 income per employee per year.

This is the point as to why the industry has to change.

The numbers just don’t stack up and if there were free rein of competitive forces in banking, then the technology oriented new entrants would have decimated the banks by now.

For example, take PayPal.

PayPal’s employee numbers aren’t generally made available for example, but I’m guessing they employ a maximum of 3,000 people worldwide – the most quoted number is that PayPal employs 2,000 of the 17,700 total eBay workforce – and will make a revenue of $100 billion and income of around $7 billion this year.

That would equate to $50m revenue per annum per employee generating $3.5m income each.

Sounds much more like the bank of the future end game.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...