We seemingly spend all of our time bashing banks these days, me included.

They’re either slow, unresponsive and ignorant of change, or they’re greedy, arrogant and screwing the economy.

You can’t win.

That’s why my new book was going to be called: “don’t tell my mum I work for a bank … she thinks I’m a piano player in a whorehouse”, but that title’s already taken.

Now however, there is some good news.

There is one UK mainstream bank that is leading the pack.

They’re innovating on the high street, in their card operations and in their mainstream banking services.

Which bank?

Barclays.

It’s hard to praise Barclays when they are 1000% tax-evasive, but when you see innovative bank services you have to fez up and applaud.

Why am I so effusive about Barclays?

Because they actually get it.

Barclaycard caught my attention some time ago.

First, there was the major campaign for contactless payments from waterslides to rollercoasters which was an integrated campaign with social media games via facebook and iPhone competitions.

They were the first bank to introduce mobile contactless in the UK, and they’re also running innovative programs around crowdsourcing customer views in the USA with Barclaycard Ring.

But it’s not just the card operations as there was also the Barclays branch of the future in Leicester Square, and more.

Now, there’s Pingit.

I saw the new ad for the first time yesterday:

It immediately made me download the app, and it’s pretty simple although they ask for a lot of upfront security processes which will put off a number of users.

The real power of Pingit is that it is a really simple idea – use Barclays to send mobile payments – and, more than this, that it’s a method of capturing the consumers’ and corporates’ attention.

The reason being that the app sits on your phone with Barclays branding all over it, whether you are a Barclays customer or not.

Simple but brilliant.

And if you don’t believe Barclays innovation strategy is working, here’s an email trail I received recently from an innovative friend:

From: Go Getter, innovator

To: Mrs. Y, Commercial Banking, ABC Bank

Hello Y

I was wondering why your bank reporting on the client account never shows transactions falling on a weekend? I believe under Faster Payments banks can clear payments during weekends. It looks like all the weekend transactions show up on the following Monday.

Is this a limitation within your bank or the type of account – and can it be changed?

Many thanks,

GG

From: Mr. X, Commercial Banking, ABC Bank

To: Go Getter, innovator

Dear GG

I work alongside Mrs. Y who passed on your query to me. I have spoken with our super helpful support desk people this morning who confirmed that even with Faster Payments they only clear the next business working day. They also advised that its not even anything to do with the type of account or their software and therefore cannot be amended. If you have any further questions or require technical assistance in the future then its best to call our super helpful support desk people on 0870 321 5432 (calls cost £85 per minute).

Regards, Mr. X

From: Go Getter, innovator

To: Entrepreneur, CEO

I’ve been thinking about our banking relationship with ABC Bank, and would like to seriously consider changing banking partner.

ABC do not strike me as interested in innovations for consumers or businesses. They’re also somewhat insipid. As an example: what Mr. X is telling me below is unhelpful, because Faster Payments is a 24/7 service and as a consumer I can both send and receive on a weekend – and whilst I followed up immediately, I suspect I won’t hear back from him any time soon.

I get the impression that of all the banks, Barclays are the ones with the most ‘innovation’ in terms of services and applications – they launched the PingIt app very recently, for example, and I also know from dealing with our BACS software suppliers that Barclays tend to do more for small-medium sized businesses. Both of our competitors are with Barclays, which in itself is interesting – perhaps they have a desire to take on innovative businesses as part of a drive to be the most forward-thinking.

It’s working.

For more on Barclays innovation strategy, read the interview with their COO Shaygan Kheradpir.

Postnote:

Jon Durant notes on his blog that Barclays has been an innovative bank for many years:

Barclays has a strong tradition of firsts and innovation: it launched the first credit card in the UK back in 1966, the first loyalty scheme in 1986, the first to accept bill payments via the internet in 1997 and the first to support contactless payments in Europe in 2011.

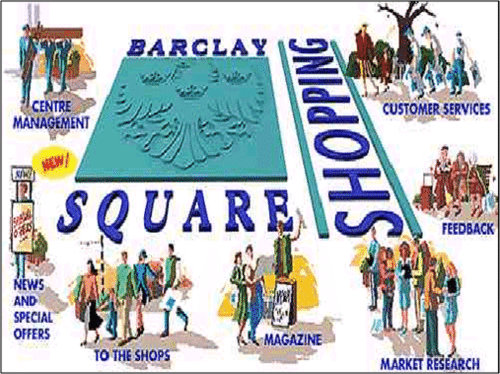

This reminded me of the innovative loyalty scheme they launched in 1995 called BarclaySquare.

I wrote a detailed research paper about industry alliances way back then, when the internet was still in its fledgling days. Here's a little more about this innovation for those who enjoy memory lane:

Another perspective of cross-industry operation is the virtual alliance, e.g. a joint venture within an electronic channel.

Banks are no longer islands of delivery - they are combining resources and efforts to leverage their position, specifically on the Internet.

This means that the more a bank can deliver in the consumer value chain - either through in-house delivery capability (e.g. managing consumer’s tax returns) or through joint venture alliances where the bank manages the partnership and extended value chain - the more they will do so.

Barclays Bank in the UK is an example of an early such alliance.

In the UK it is estimated that four million people have access to the Internet, but of those, only 1.5 million are using the Web on a regular basis. This seems a fairly limited audience, but that underestimates the value of this market. According to Money World, this audience is almost 100% ABC1, 80% male and 66% between ages 25-44, all segments financial services want to reach.

Barclays decided to differentiate their site by adding non-financial services to its Internet site.

Through BarclaySquare, the UK Internet Site for the Bank, the bank has teamed with retailers to leverage the bank’s card base. As well as getting information on Barclays products and giving feedback, customers can go to the shops or buy airline or train tickets.

Barclays aim is through a virtual alliance to be the Internet Brand.

As Consumers remember that the site they shop at is called Barclaysquare from Barclays Bank, the shopping mall, brought together by the Bank, becomes the brand.

It is only once you go through the bank’s gateway that you find a florist - Interflora; a clothes shop, Debenhams; a catalogue merchant of durable goods, Argos; a Toy company, Toys ‘r’ Us; an insurance company, Sun Alliance; and a telecoms company, BT.

Launched in June 1995, BarclaySquare allows consumers to pay for a range of goods on the Web using Barclay’s own Visa or MasterCard.

The early results have been pretty good.

From June-November 1995, Barclaysquare had 100,000 visitors; 600,000 page requests; 400+ retailer enquiries; and 3,000 e-mail messages.

In December 1995, over 15,000 visitors used the system.

In 1996, it had 1.5 million page requests and the first quarter of 1997 created 500,000 hits, a 10% increase.

More than 20 retailers work with BarclaySquare including Sainsbury's, Victoria Wine, Interflora, Argos, Eurostar, British Telecom (BT), Toys 'R Us, Victoria Wines and the Airline Network.

"The Barclays (Bank) Web page is contained within BarclaySquare and some people browse at that as well on visits," said a Barclays spokeswoman. "It has proved very popular and is an innovative and pioneering way of Web site marketing."

Barclays is planning to boost the profile of the scheme by mailing its 3 million credit cardholders with a magazine promoting the scheme's advantages. "We are also encouraging more retailers to join," he said.

If you're wondering what happened to BarclaySquare (a pun on Berkeley Square), it didn't get the takeup as Barclays is not Amazon ... so it's up for sale.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...