Apparently, I am a miscreant. I am the one guy who managed to break PayPal. What? OK, here’s the story. The next 2,000 words tell the story but, if you’d rather miss that and cut to the chase, jump to the end.

Most of my customers wire me the money. American customers are more of a pain as they send me paper checks – America hasn’t heard of electronic payments yet – but I forgive them as most of the checks are honoured. Thanks. Then a few customers ask if they can pay me by card. Now, I’m a simple guy and think the easiest way to get a card payment is through PayPal. The fees hurt, but it’s the simplest way to send an invoice asking for a card payment.

So far, so good.

Then I got a client in South America who hasn’t received a PayPal invoice before and, when he got mine, decided to a pay via PayPal rather than his credit card. Simple. He didn’t need to open a PayPal account – when you get a PayPal invoice there is an option to pay direct with a credit card, but he didn’t see that bit. So he thought he had to open a PayPal account to pay by card.

So far, so good.

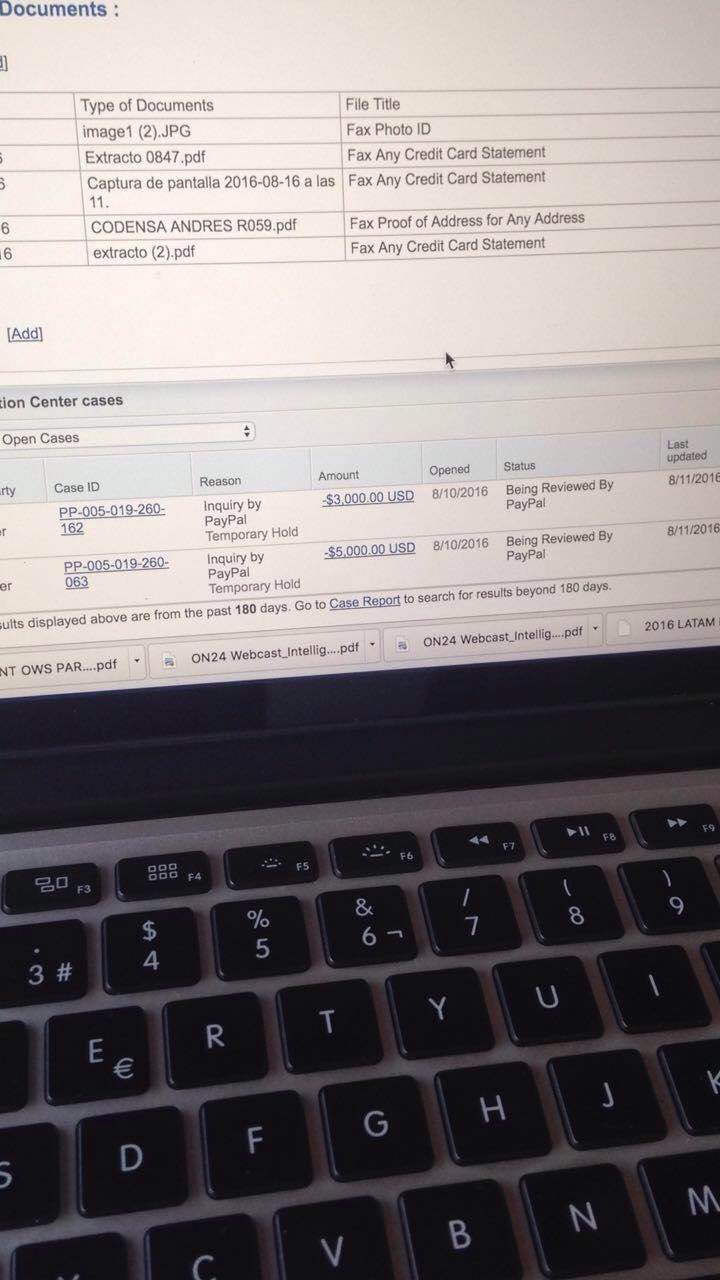

Payments were sent and I received them in my PayPal account on August 9. On August 10, seeing the money in my account - $8,000 – I decided to move $7,000 to my bank account. That worked, with my account showing £5,230.48 had been sent (we had a terrible exchange rate on August 10), but then the problems began when PayPal determined that the $8,000 transfer from South America needed more authentication. As a result, the money that had been in my account for a day was placed under a Temporary Hold whilst there was a PayPal Inquiry. In doing so, they reversed my bank transfer request of $7,000 (£5,230.48) and cancelled it.

Fair enough. Irritating, but hey, problems sometimes arise.

One problem now is that my account was showing that I owed PayPal £262 for the fees of processing the payment. It also showed $7,000 was due back. I wasn’t sure how that could be as my bank transfer of $7,000 had been cancelled by PayPal, and my bank account never received a credit for the funds. However, the key problem was that neither I nor my client knew why PayPal had placed the payment on hold.

I duly filled in the details of why I was receiving the payment, and thought things would clear. Two days later, they hadn’t, so I called PayPal to find out why and was told that the payee had not responded to their request for information.

I emailed my client, and he promised to contact PayPal to sort it out. My client emailed me on August 15 and said they had talked with PayPal and all should be clear. It wasn’t. I rang PayPal and they said the client still had not responded to their request for information.

Weird.

They then said that if it wasn’t sorted out by August 17, they would cancel the whole thing. So I’m pretty annoyed now as the implication was that PayPal would cancel all and leave me -£262 worse off in fees.

I finally call my client. They say they’ve done everything that’s been asked and email me a screen shot of their PayPal account page.

I now see the issue: PayPal is asking them for KYC information. They’ve asked for a passport or driving licence photo ID and proof of residence. I call the client again and ask if they’ve done this. No. Reason being: they don’t speak English, have never used PayPal before and didn’t realise that they had to do this.

I tell them what to do. They do it. And Hallelujah, PayPal release the funds.

It still stinks however.

For an $8,000 payment they’ve charged over $500 in processing fees (almost 7% on the transaction) and, to top it all off, when I get the money released on August 17 the exchange rate has changed so much that instead of the $7,000 transfer being worth £5,230.48, they’ve now calculated it’s only worth £4,873.52. So I’m £356.96 worse off due to currency conversion. Add the fee charges and a total loss of almost £600 on the true value of the transaction. Should have used TransferWise but hey, I’m a luddite.

Ah well, job done. Nothing worth blogging about. Just make sure I don’t use PayPal again for this sort of transaction.

But the story doesn’t end there.

You may remember that I mentioned my account showed $7,000 debt due and, unbeknownst to me, this was flagged on my account because when PayPal reversed the transaction on August 10, they issued an echeque request to my bank to return the funds. Basically, the echeque was to reverse the $ payment. They had already reversed the payment however in £'s, as noted above.

echeques take 7-10 days to process and hence when I checked my bank account to see that I had successfully transferred the £4,873.52, I got a real shock. The day before, PayPal had taken £5,590.28 from my bank account. That was the echeque clearing $7,000, and a higher amount due to buying versus selling dollars (more currency conversion losses).

The echeque had taken three working days to process, and the £5,590 taken from my bank account was for the transaction from August 10. The transaction that was never completed because PayPal cancelled it.

So I’m now livid and call PayPal to find out what they’ve done and why. The lady on the customer service team cannot explain it, and tells me that it’s been sent to the Executive Escalation Team, whatever that is.

The next day, no contact, and I call to find out what’s going on. The customer service rep tells me he can’t talk with me as it’s with Executive Escalations, and they’ll be in contact.

Meantime, I’m livid. Having blocked a payment for over a week with no adequate explanation, causing embarrassment with my client and forcing them to do things that I really didn’t want to have them do, they’ve now stolen £5,590 from my bank.

I call my bank and, under the direct debit indemnity scheme, tell them that the PayPal transfer was an error. My bank tells me that they will get the money back in 7-10 days but, if it is a justified payment, the requester can legally take me to court. Am I comfortable with that? I say absolutely.

Deal done and the money should come back.

Meantime, later that day, I get a call from the PayPal Executive Escalations team. James tells me that he’s listened to all the phone calls I’ve made and reviewed all the details, and that things are strange. In fact, he tells me that I created a PayPal Perfect Storm, and he’s never seen anything like this in his years in the company.

Here’s why.

First, he tells me it wasn’t due to KYC that the payment was on hold. I beg to differ as I tell him I’ve seen the screen shot. He says that he can’t discuss a third party accountholder’s information, but that PayPal inquiries are usually routine. The issue here is that the PayPal inquiry started almost 24 hours after crediting my account with the funds. As a result, and unusually, I had taken money out of the account and that had caused the problem.

The key issue was that not only did I withdraw the funds but that the funds also involved currency conversions from $’s to £’s. This meant that some transactions were in dollars and some in pounds, and dependent upon what part of the process was involved, resulted in some residuals in dollars and some in pounds.

When I did the funds transfer, that’s the reason why it showed $7,000 was due back, and this was sent as an echeque to my bank. He tells me that echeque had not cleared and, if it had, the funds would show as a balance on my PayPal account. I tell him the cheque has cleared, the funds left my account the day before according to my bank and no funds were ever received from PayPal before that. In other words, I believe PayPal has stolen the money.

He assures me that’s not the case as the echeque has not cleared. I tell him it has. Stalemate. Luckily, I revert to the fact that my bank has requested return of those funds under the direct debit indemnity scheme, as I can see that James has no idea why funds have left my account and not appeared in his PayPal world.

Anyways, he then does his best to calm me down, promising that he’ll refund the loss on the currency conversion and cancel all fees for processing these payments.

I’ve calmed down.

He tells me that the Perfect Storm was created by the mixture of $’s and £’s, the funds transfer, the echeque request and the inquiry all occurring in a 24-hour period, and he’s never seen that before.

But it still doesn’t answer why £5,590 left my bank account and yet PayPal claim they never saw it. Whatever. Funds have been returned, payment has been processed, fees have been waived and I’m a much happier bunny.

Mind you, I did wonder whether the email from their press department asking me what’s wrong when I tweeted #PayPalSucks might be the reason why I got such a resolution.

I've discovered why so many say #PayPal sucks. Blog coming up soon. They are a disaster. Totally useless on all fronts and thieves #wuzafan

— Chris Skinner (@Chris_Skinner) 17 August 2016

So that’s that … not quite.

The next day my bank sends me a text saying that my case review on my direct debit request has been resolved. I check my balance and … no funds received. I ring the bank. They tell me that I can’t have the money back because I issued the echeque. I tell them I didn’t. They tell me that’s what PayPal have told them and there’s nothing they can do about it. So much for a direct debit indemnity guarantee.

Now the situation is that on 10th August, PayPal reversed the $7,000 transaction I requested, sent no funds to my account and issued an echeque for the return of the $7,000. The echeque was processed by my bank on 17th August, and converted to £5,590. I speak to PayPal and they tell me the echeque has not been cleared or it would show on my account. I speak to the bank and tell them to get that money back, but they can’t. They tell me it’s a PayPal issue. I go back to PayPal who say that they will investigate but, being Friday afternoon, it will be after the weekend.

Great. So far, I’ve spent about 8 hours in phone calls between my bank and PayPal trying to get the situation resolved, and have had $10,000 delayed by a week followed by PayPal stealing $7,000 from my bank account without authorisation. Not a happy bunny.

After the weekend, everything magically resolved itself when the echeque that came out of my bank account on the Wednesday landed in my PayPal account on the Saturday. One click and it’s back in my bank via a faster payment from PayPal. It does make me wonder why the bank sent the payment via BACS and hey, it just goes to show that an echeque raised on 10 August took ten days to clear. Why use echeques? It seems so last century.

So that’s that …

… oh no it isn’t. On the Monday I find $7,000 added to my PayPal account, yay. Suddenly having been over £5,000 down on an unauthorised transaction, I’m now over £5,000 up. Just in case PayPal spot it, I don’t spend the money straight away and, sure enough, on the Tuesday PayPal spot it. Unlike my 10-day trauma however, they immediately take the money back and demand that I also send them the $700 I’d spent during the Monday.

I thought about saying no but hey, they had tried hard to rectify the problems they caused by crediting me with a free transaction … and all this just because my client thought they had to open a PayPal account, due to sending them a PayPal invoice that they could have just paid with a credit card.

Here’s how I broke the PayPal system.

The backdrop to the above is the reversal charge that PayPal actioned, when they suspended the account of my payee whilst KYC checks were performed. Unfortunately, this involved two currencies – dollars and pounds – and amazingly, the PayPal back office systems aren’t geared for this. Hence, they reversed the transaction twice – once in dollars and a second time in pounds.

This is why, after the UK pounds were returned in real-time, the system generated a $7,000 echeque and showed my account with $7,000 due back whilst the echeque was being processed. The echeque takes around ten days to process, and was drawn on August 10; processed by my bank on August 14; shown on my PayPal account as UK pounds sterling on August 20; and then converted to $’s on August 22. By that time, my balance was cleared and so now, having taken two charges, it had credited me back with two charges.

I’m sure PayPal is a very effective innovator in their Venmo and Braintree operations but, what this story implies, is that their core PayPal processing engine is unfit for purpose. That is either because it is old – PayPal was started in 1999 – or, and more likely, that I’m the first guy who has had a US dollar reversal when my main currency is not the US dollar. I find that hard to believe – how many merchants use PayPal – but will give them the benefit of the doubt this once.

A final word from PayPal themselves …

“For the vast majority of the millions of payments PayPal processes every day across the world, the payments happen without incident and our customers have access to their funds immediately. In this instance, we should have done more to help Mr. Skinner deal with a particularly complex set of circumstances. We don’t always get things right, and we’re sorry for the inconvenience caused. We have refunded the associated fees and compensated Mr. Skinner for any loss due to currency fluctuations.”

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...