Building on yesterday’s discussion of the digital divide turning into a human divide*, I find it intriguing how we talk incessantly about financial inclusion and how technology will bank the unbanked. It is our dream. But is it just a dream?

The reason for thinking this is that poverty and inclusion is yet another area, like identity and clearing and settlement, where technology is not the solution. It can assist in creating a solution, but it’s just part of the solution. The first part – before the technology – is the willingness to use the technology to create a solution.

We have things bubbling away to do that, like the United Nations Digital Identity Project, but it’s going to take a long time. Bear in mind 1.5 billion don’t officially exist – their births have never been recorded – and there are still 757 million adults (including 115 million 15-24 year olds) who cannot read or write a simple sentence. That’s a sizeable portion of the world’s population who, even if you gave them the technology, may not be able to use it effectively.

That is changing however. There are many programmes being implemented to use technology to reduce poverty, from the Bill & Melinda Gates Foundation to the World Economic Forum. A few examples:

- The Poverty Stoplight assessment tool to alleviate poverty in developing countries

- The Europe 2020 Flagship Initiative

- Financial Services for the Poor by the Bill & Melinda Gates Foundation

- Consultative Group to Assist the Poor (CGAP)

The bottom-line of all of these groups is that today, access to finance for the poor is the most expensive. It should be the other way around. I see this regularly as a point of issue. Those who need money most proportionately pay the most for it. It goes with the old saying of banks give loans to those who can’t afford them, and then make them pay and pay and pay. Those with the least money are the most likely to be overdrawn, and pay and pay and pay. Those with the least money are the most likely to use payday loans and pay and pay and pay.

This is particularly well illustrated in the book Debt by David Graeber. To illustrate his contention. This book is a must for any bookshelf, and lays out the history of debt as the force for humans to order societies from those who control to those who serve. A small number (the 1%) control the majority who owe them (the 99%). Once in debt, the book contends, you can never really get out of it unless violence changes the order of the system: a revolution, a civil war, a war between nations. For example, here are just two paragraphs of the 100,000 word book that struck me as enlightening:

Nowadays, for example, military aggression is defined as a crime against humanity, and international courts, when they are brought to bear, usually demand that aggressors pay compensation. Germany had to pay massive reparations after World War I, and Iraq is still paying Kuwait for Saddam Hussein's invasion in 1990. Yet the Third World debt, the debt of countries like Madagascar, Bolivia, and the Philippines, seems to work precisely the other way around. Third World debtor nations are almost exclusively countries that have at one time been attacked and conquered by European countries — often, the very countries to whom they now owe money. In 1895, for example, France invaded Madagascar, disbanded the government of then-Queen Ranavalona III, and declared the country a French colony. One of the first things General Gallieni did after "pacification," as they liked to call it then, was to impose heavy taxes on the Malagasy population, in part so they could reimburse the costs of having been invaded, but also, since French colonies were supposed to be fiscally self-supporting, to defray the costs of building the railroads, highways, bridges, plantations, and so forth that the French regime wished to build. Malagasy taxpayers were never asked whether they wanted these railroads, high- ways, bridges, and plantations, or allowed much input into where and how they were built. 1 To the contrary: over the next half century, the French army and police slaughtered quite a number of Malagasy who objected too strongly to the arrangement (upwards of half a million, by some reports, during one revolt in 1947). It's not as if Madagascar has ever done any comparable damage to France. Despite this, from the be- ginning, the Malagasy people were told they owed France money, and to this day, the Malagasy people are still held to owe France money, and the rest of the world accepts the justice of this arrangement. When the "international community" does perceive a moral issue, it's usually when they feel the Malagasy government is being slow to pay their debts. But debt is not just victor's justice; it can also be a way of punishing winners who weren't supposed to win. The most spectacular example of this is the history of the Republic of Haiti — the first poor country to be placed in permanent debt peonage.

The most spectacular example of this is the history of the Republic of Haiti — the first poor country to be placed in permanent debt peonage. Haiti was a nation founded by former plantation slaves who had the temerity not only to rise up in rebellion, amidst grand declarations of universal rights and freedoms, but to defeat Napoleon's armies sent to return them to bondage. France immediately insisted that the new republic owed it 150 million francs in damages for the expropriated plantations, as well as the expenses of outfitting the failed military expeditions, and all other nations, including the United States, agreed to impose an embargo on the country until it was paid. The sum was intentionally impossible (equivalent to about 18 billion dollars), and the resultant embargo ensured that the name "Haiti" has been a synonym for debt, poverty, and human misery ever since.

The book was made into a radio series by the BBC and there are several lengthy lectures on YouTube. It’s a great book. Hasn’t changed anything, but it’s a great book.

Why am I writing this today? I’m writing it not for any altruistic reasons or for a cause, but because we often debate free banking in Britain, and there’s no such thing. Banking in Britain works on the basis that the poorest pay all the charges so that the richest can have free accounts. You don’t believe me?

Free bank accounts are unfair to poor customers and form an unsustainable foundation for the banking system, according to Post Office Money’s chief executive, Nicholas Kennett, who wants to see the industry charge customers regular fees instead.

He believes it is unfair that customers who have to use their overdrafts are charged high fees, which are then used by the bank to offer free accounts to the better-off who rarely pay any fees.

The system also makes it hard for new banks to challenge the incumbents, as the cross-subsidy makes it hard for customers to work out which account offers better value.

This was addressed in the recently released Competition and Markets Authority report, who introduced “measures to enable personal customers to take more control over their use of overdraft services as well as improving the switching process for these customers.

First, customers need to be given clear notice when they are going into overdraft. We will therefore require banks to alert their customers, for example by sending a text message, when they are going into unarranged overdraft.

Second, customers need to be given the opportunity to avoid incurring charges. The alerts that banks will be required to provide will also inform customers of a ‘grace period’ during which they have an opportunity to avoid charges.

Third, banks will be required to set a ceiling on their unarranged overdraft charges, in the form of a monthly maximum charge (MMC). A bank’s MMC will specify a maximum amount that the bank can charge a customer during any given month, taking together all unarranged overdraft charges including debit interest and unpaid items fees that the bank charges. Banks will be required to disclose the MMC associated with each of their accounts, so that customers are fully aware and can use it to compare providers.

Fourth, we are recommending that Bacs and the FCA explore ways to make it easier for overdraft users to shop around and switch banks including online overdraft eligibility tools.”

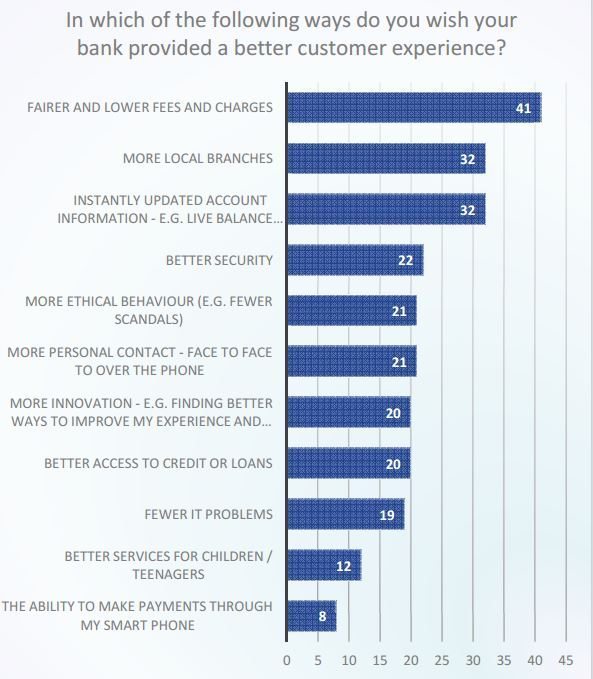

Great. But that still doesn’t address the issues of poverty and financial inclusion in Britain, as highlighted by a report from Neopay. The report concludes that the biggest opportunity for challenger banks is to (1) have fairer and lower fees and charges and (2) have more branches.

More branches????

Yep. According to the report, bank branch closures (1,700 in the last five years) hit lower income families, the elderly and those with disabilities the most. The reason is that many of these groups do not have access to online banking, lack digital literacy and have issues travelling to branches further afield. As a result, they are hit the hardest by bank branch closures.

Scott Dawson at Neopay summarises it well:

“A clear message is being delivered to traditional banks from consumers, and indeed from campaigners such as Age UK and Campaign for Community Banking Service (CCBS), that branch closures are frustrating and only serving to alienate groups that are in need.

“Bigger banks need to carefully consider the damage each individual branch closure will inflict on communities as they weigh up the pros and cons of doing so. While our banking landscape is increasingly shaped by the digital era we find ourselves in, it’s important we remember that not all groups are able to take advantage of technology and innovation. For those without internet access or the know-how, the continuing branch closures, which are disproportionately higher in deprived areas, can spell serious trouble.

“And, with our report finding that opening more local branches to be one of the top ways consumers believe banks can improve customer service, this could be just the ammunition needed for banks to reconsider their position on proposed further closures.”

So the poor pay the most in charges and get the worst deal. Sounds about right.

* Quick recap:

We all know that there is a digital divide to day where the poorer, less educated are less included in our world than those with money and education. The prediction of Professor Yuval Noah Harari is that, in near-term future, those with money will design their children to be more intelligent and achieve more than those without. Those without money will become irrelevant as human beings essentially.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...