As mentioned yesterday, there’s a big question about what all of this means for financial service. You may not have asked those questions but if life sciences allows people to live for 150 years or more; if babies can be born without defects; if you can design yourself to be whatever you want to be; then that raises all sorts of questions.

How will you live in a world where those who can afford it are beautiful and can live for almost ever, whilst those who cannot are secondary. I blogged about these things just last month, so I’m not going to over labour this entry here. However, it is worth thinking about:

- What pension policy will you need for 150 years of possible life?

- How many jobs will you have during those years and when would retirement be ready?

- What jobs will there be if we can automate almost every form of work?

These are fundamental points primarily for insurance firms who offer critical illness plans, health insurances, pensions and related products. In particular, there will be issues around work - everything can be done by robots - and longer life planning. After all, when Otto Von Bismarck came up with the idea of a pension, most men died in their 40s. That's why retirement age was set at 65. Today the average person is living until 80 and that is why we have a pensions shortfall in most economies. Now the average lifespan is increasing to 100, so what should the new pensionable age be? 80?

These are insurance challenges, but banks will also find challenges and opportunities here.

- How will wealth be built and who will be building it?

- If someone becomes high net worth as they enter their third or fourth career in their seventies – 70 is the new 35 – will you even be considered, bearing in mind that most people choose their bank by the age of 30?

- Can you offer high net worth products to people who have had enough years to suss you out?

- What will trust look like if it’s being played out over centuries, rather than decades?

Obviously, governments will also have huge challenges as, with 150 years of life, how many people will be living on the planet? Earth’s numbers are doubling every thirty years or so, and this would see those numbers explode. Add to this the ending of poverty (Bill & Melinda Gates Foundation) and the end of disease (Mark & Priscilla Zuckerberg) … what will all of these people be doing?

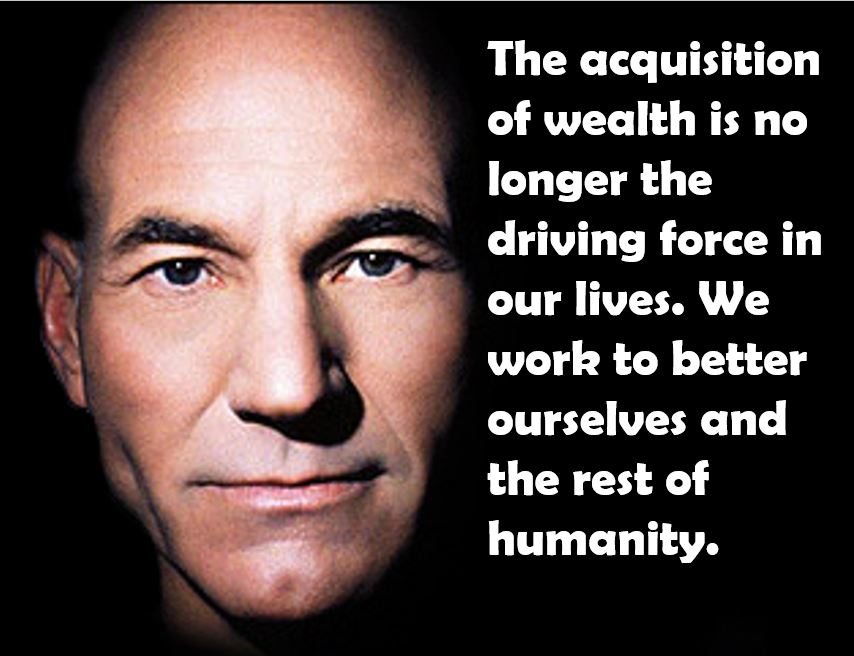

Some believe it will lead to a world without wealth as a focus (Star Trek):

Others believe it will lead to a world of slums for the poor (the 99%) and floating cities in the oceans and stars for the rich (the 1%). Such visions have been around for a long time, dating back to Fritz Lang’s Metropolis in the 1920s, and oft repeated in other movies. Most recently, The Hunger Games , In Time and Elysium explore the same themes of the rich living on the fat of the poor and are all, to an extent, remakes of Metropolis. In fact, most films you look at have some resonance with that landmark movie.

The discussions represent two extremes, but there is often a middle way. The Star Trek way would bid banks, money and governments farewell. The world would act as a global citizen with democratized money, self-regulating structures and no need for statist interventions. I love the idea of that world, but just cannot see it working even with bitcoin. Bitcoin succeeds by being democratized and providing money without government, but how will that self-regulating structure eradicate risks such as terrorist funding, money laundering, drug money and contracts for assassinations or paedophilia? Will a self-regulating market run that world?

At some point controls need to be in play that rise above the democracy for these reasons. At this point, it offers the opportunity for Metropolis to step in. The controllers control the weak. They accumulate wealth and find ways to exploit those they control because they set the rules.

This is all getting a bit too existential for me, but I fundamentally believe that we will have democratised money for value exchange, with digital identities that we control who can access but are issued to us by a statist intervention.

Whether that statist is the United Nations, European Union or UK government, as a UK resident, I have no idea. But the digital identity I control in the future will be on some form of distributed ledger and that’s the real question: who runs that ledger?

Again, I’ve hazarded a few guesses in the past – some say my recent piece on Applying Blockchain to Digital Identity is pretty good – but there will be an identity controller (me) and an identity issuer. We may automate the issuer through blockchains, but there will still be an intervention somehow, some way to get at that control and, as discussed, you then have the ability to build power through that control.

It’s gonna be fascinating to see how that evolves and I’ll return to these themes several times this week as we explore the future world built upon the internet of things tomorrow.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...