I’m just starting a project on real-time, immediate, faster payments or whatever you call it. It’s basically making a payment that is either settled within seconds or the data is moved and settlement takes place at a later time, but it look immediate.

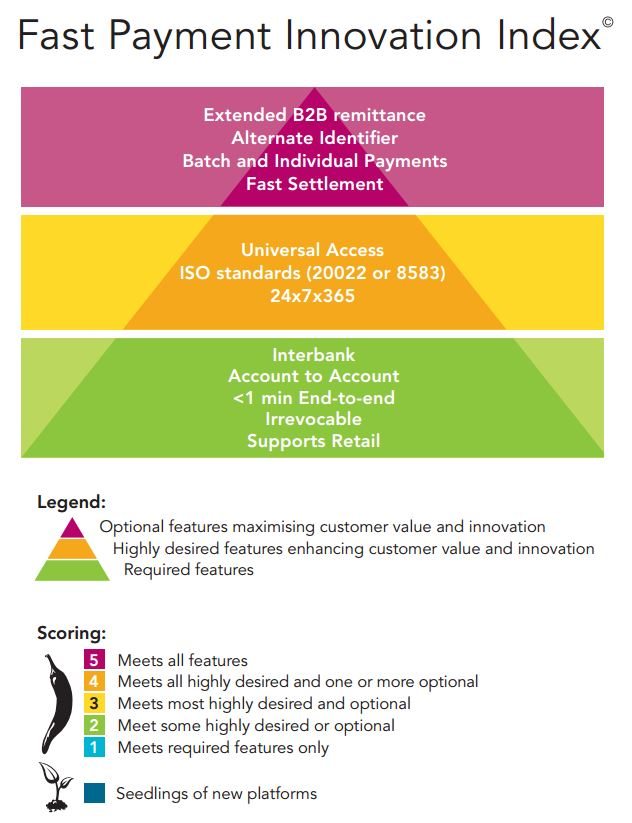

There’s lots of reports out there about immediate payments, with my favourite being from Clear2Pay, now FIS, because it’s produced by my good friend Conny Dorrestijn. A few years ago, she started a faster payment innovation index which ranks different country’s schemes based upon the functionality.

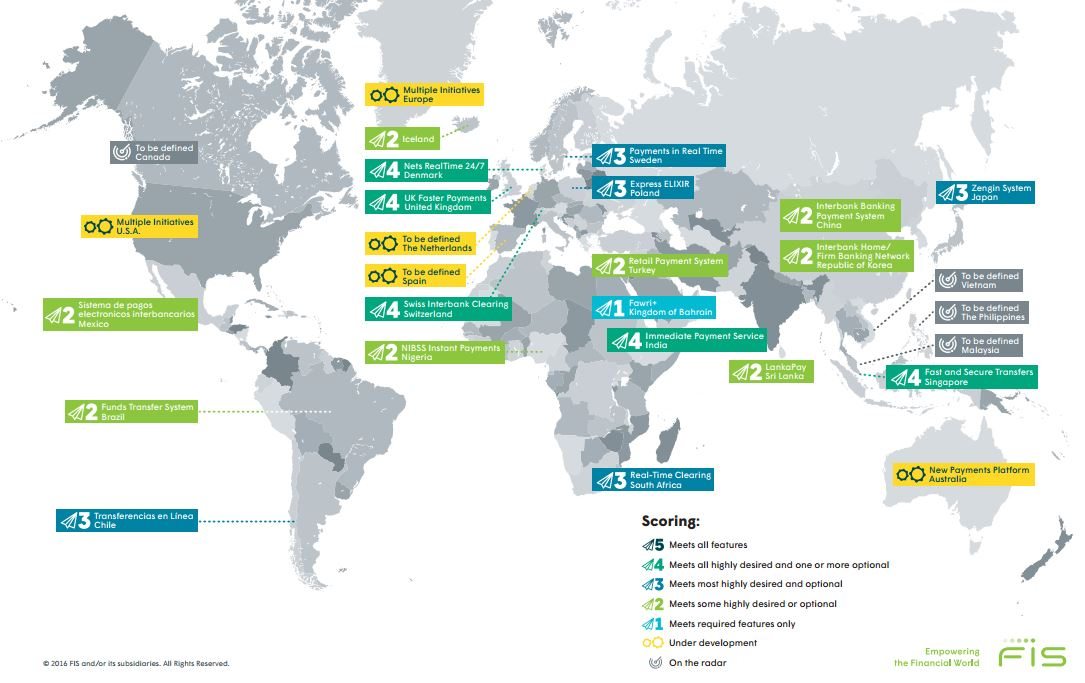

In 2016, most countries would struggle to score more than 3 but the UK, Denmark, Switzerland, Singapore and India manage to get a ranking of 4 (doubleclick map for a bigger image).

Nevertheless, I couldn’t find a clear statement of the pros and cons in their report, so I started looking at the big consulting houses to see what they had to sya.

In May 2015, McKinsey‘s payments report had an insight into faster payments:

Faster payments: Building a business, not just an infrastructure

To date, most discussions about building a “faster payments” system have focused primarily on speed and “plumbing.” Even more important, however, are the innovative products and services that an enhanced infrastructure will allow financial institutions to bring to market. These new products and services—in both consumer and corporate payments—can create new revenue streams and help banks and other players realize a return on their investment in a modernized payments system.

They note the UK being forced to upgrade their payments infrastructures when the regulator clamped down on three day processing and demanded same day. What’s interesting is that McKinsey estimate the cost of the UK Faster Payments Scheme as “between £150 million and £200 million to build and operate for the initial contract period of seven years (2008-2015), plus up to £50 million for banks to connect to the central infrastructure”.

McKinsey note that faster payments allows payment product innovations from peer-to-peer payments, mobile payments, einvoicing and more. Great. But where’s the ROI? Maybe it’s in growing volumes of new services? For example, Forrester forecasts that P2P payments will reach up to $17 billion by the end of 2019 from $5 billion in 2014, largely driven by accessibility and an attractive user experience that focuses on speed and convenience for both domestic transfers and cross-border remittances. Maybe so, but McKinsey propose that it’s not revenue generation and new product revenue streams that’s the focus, but cost savings and modernisation.

While some existing revenue streams (such as paper-based services) will no doubt be

impacted by a modernized system, the digitization of information, the rise of mobile commerce, and end-users’ rapidly changing expectations all create the opportunity for banks to boost customer engagement, gain a greater share of wallet, and acquire new customers.

New revenue streams will be the primary source of return on investment in a modernized payments infrastructure, but it is worth noting that additional cost savings could be significant if banks seize this opportunity to integrate their payments architecture … McKinsey estimates that banks can reduce their payments-related IT spending by 20 to 30 percent when they integrate their payments architecture.

OK, I can buy that. In fact, the real driver may not be the ROI but just keeping up with customer and regulatory needs. For example, the Deloitte Faster Payments report has a nice little graphic that explains the world of change.

They explain this graphic as follows:

What is driving the growth of real-time payments?

We have witnessed tremendous technological and business model changes over the past decade. From new payment platforms and solutions, to updated regulations addressing payment effectiveness and security, to — maybe most significantly — higher expectations from merchants and consumers.

Technology innovation: Smartphone adoption has reached 70% in developed countries, while in various developing economies feature phones are often replacing wallets and cash. New domestic person-to-person (P2P) payment providers are popping up on a regular basis, due to catalysts like social platforms, digital currencies and near-field communication (NFC) based payments. Rapid technological change is driving rapid change in the industry.

New players and business models: While the traditional financial industry once controlled the world of payments, new start-ups, spin-offs, and partnerships are introducing new options for the payments sector. In the last few years numerous new FinTech startups have launched with a focus on mobile payments. The focus tends to be on new services, for instance, security with fraud detection and authentication, improved customer experience or making funds available quickly to small businesses when their line of credit is approved. The next step for these organizations may be determining whether real-time payments becomes a core business element and ways to design an operating model to help optimize that service delivery.

Merchants’ expectations: In addition to payment assurance and lower fees for transactions, many small businesses and large retailers alike are looking at real-time payment to enhance their cash flow management, reduce fraud activity and provide incremental value to their customers.

Consumers’ expectations: Due to rapid technological change, many consumers now expect almost everything to be available in real-time — but payments often seemed stuck in the past. The age of instant gratification is here to stay. Paying bills or friends should not be more than a few clicks or touches away, and the same expectations tend to apply to accessing funds as soon as they are available.

Regulatory pressure: Regulators across the globe are leading efforts to accelerate payments. The Federal Reserve Bank and the National Automated Clearing House Association (NACHA) are working on a roadmap and incentives to accelerate real-time payments in the US. Regulations in some developed countries are supporting real-time payments. This can benefit consumers and the government, which can efficiently trace activity and help increase the fluidity of the overall economy.

Globalization: Generally, consumers and corporations expect the same simple payment and transfer experience regardless of where they are in the world. More efficient payment solutions have already been effectively implemented in various countries and for a large variety of use cases. As the roster of countries adopting real-time payments grows, the pressure on other countries to lay the groundwork and support speedy payments is likely to increase.

Very good, and I’m a lot clearer now that immediate payments is all about creaking old infrastructure that cannot keep up with consumer, merchant and market needs, so has to be renovated voluntarily or by regulatory force. The outcome is increased volumes at lower margins, so not a profitable uplift but a cost overhead reduction.

There are other reports of note out there on this subject, such as Cap Gemini’s paper on US immediate payments developments and Deutsche Bank’s research paper, but back to what I’m up to. In the next month, I’m launching a research program into the benefits and issues of real-time payments. If you’re interested in participating, please leave your email address as a comment under this blog entry. Your email will remain private – only I will see it – and I’ll make sure to ping you the survey when we launch it in the next few weeks.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...