The final day in Hong Kong focused upon innovations and several speakers provided a rich overview of innovation across the region, mainly n Japan and China.

I’ll blog about some of these for the rest of the week, as I was particularly impressed with a few areas of leading-edge technology being deployed in a consumer and business friendly manner.

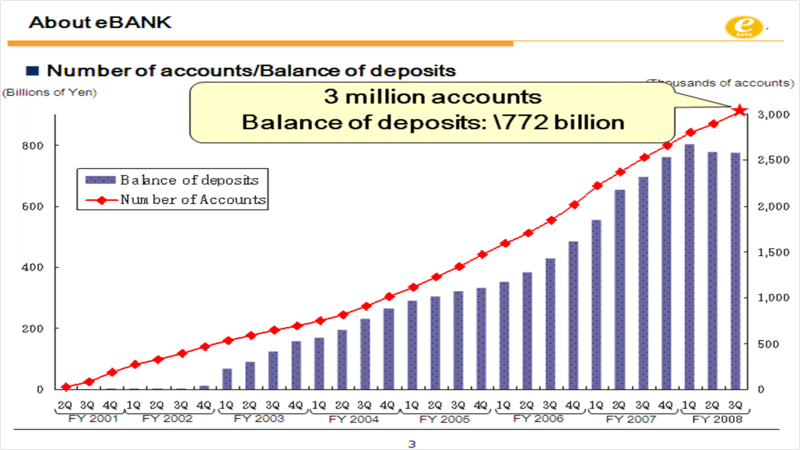

For example Kazuhiko Saiki who leads marketing and operations for eBank in Japan, discussed the latest developments in eBank in-depth. Now I’ve blogged about eBank before and use them regularly as an example of how to do things differently because they have over 3 million customers with a total bank staff of under 200 people. That’s 15,000 customers per employee. Amazing.

And it’s growing too, as shown by the slide below:

¥772 billion in deposits is almost US$8 billion ... not bad for an internet only bank that has just passed eight years old.

I also notice that the number of accounts almost doubled from the end of 2006, as the bank moved access to both mobile and internet channels rather than just internet services.

How eBank manages the on-boarding process and structure is fascinating, as I haven’t seen this in other countries yet, and it’s also a major part of their success as it means no human hand is involved with the account opening process.

Saiki-san discusses this process in the video below**.

There are three slides he refers to here. First, a slide showing how a typical bank receives a client application form:

Then, the way that eBank receives client application forms using mobile with a photograph of the driving licence:

And then they use the driving licence as identification papers and run this through an OCR (Optical Character Recognition) to automatically fill in name and address and verify the licence number is valid with credit checking systems and government databases:

If all information is verified, then the client account is opened and confirmation documents sent in the post (yes, there is paper!).

This is fascinating stuff and, as a result of such innovations, eBank have become the most popular inter-based Japanese bank with almost 1 in 2 online accounts, a 48% market share.

This success attracted an acquirer to step in and, in January 2009, eBank become a fully owned subsidiary of ... an etailer!

Rakuten Group purchased eBank to become the one of most popular internet sites in Japan behind Google, Amazon, eBay and Yahoo!

Considering our concerns about Wal-Mart and others entering the retail banking space, it is interesting to consider that we now have several internet brands running the largest financial operations in the world. For example, Rakuten in Japan, eBay in America with PayPal and Alibaba in China with Alipay.

This is a space to watch.

Meanwhile, eBank aren’t alone with their success, and are now threatened by a new bank.

A mobile telephone only bank.

A bank with no branches or internet site as such, but everything focused upon self-service through the mobile.

A bank launched only a few months ago.

A bank launched by a major Japanese bank.

More about that tomorrow.

** All presentations and videos are available for Club members

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...