I was pleased to hear about the progress of MoBank, the UK’s first mobile-only bank, which launches in May.

It’s not a fully fledged bank yet, like Jibun Bank, as it’s starting out as a convenient way to buy things through an iPhone and designed for young adults.

So it doesn't have all the transactional capabilities of a normal banking service but it will, as MoBank plans to offer a savings account, P2P payments, account aggregation, bill payments and a virtual prepaid card over time.

Long term?

Britain's first mobile only bank.

Steve Townend, MoBank’s CEO and co-founder, presented the firm’s plans at a conference with me last week.

Steve and fellow co-founder of MoBank Dominic Keen, both worked together at Egg. Strangely enough, many of the founders of Zopa also worked at Egg, which may be indicative of where to look for these entrepreneurs of new models of finance. Steve was also head of lending at First Direct, so he knows a bit about telephone banking, internet banking and disruptive banking innovation.

Now, I’ve heard Steve talk about MoBank’s plans before but it is now ready to launch, having secured a further $1 million in funds in January, so here’s the low-down.

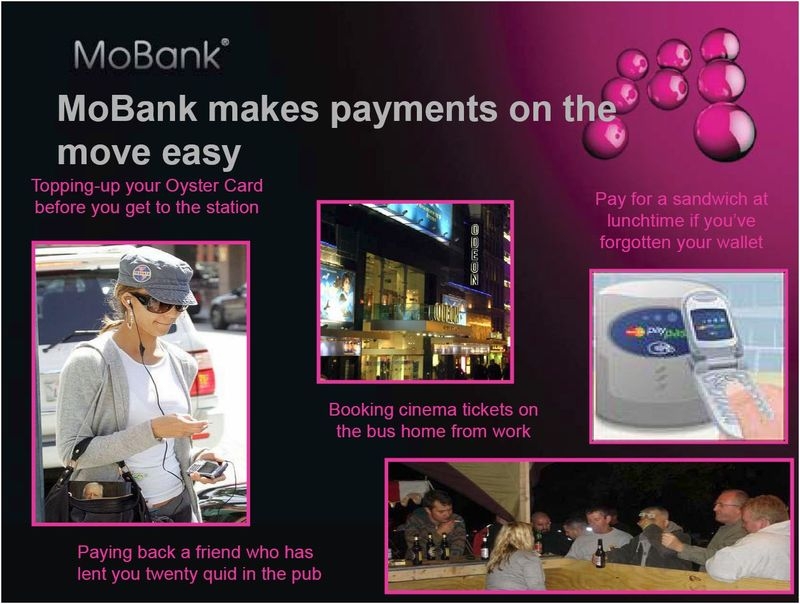

MoBank is a new mobile service that allows customers to buy and pay for goods wherever and whenever they want. By working with the customers’ existing account it is a convenient and secure way to make day-to-day transactions and administer personal finances from a mobile phone or any Internet connected device.

MoBank works on the iPhone and iPhone touch and is primarily targeted for students and young adults, with 100,000 of them expected to sign up in the first year.

I particularly like the MoBank interface which is a very easy-to-use and attractive iPhone applet that makes buying convenience plays - such as cinema tickets, flowers, mobile top-ups and similar goods and services - a breeze.

From launch, MoBank will offer cinema tickets, clothes, music, books, train tickets, flowers, gifts and takeaways on the service. A typical example of the services concepts is that people will use MoBank when they are on their way out, for example, and they realise they have forgotten their Mum’s birthday or whatever.

In this case, they can send her flowers just by ordering, buying and paying for them via MoBank on their mobile phone. To do this, the user simply downloads the MoBank application, register their credit or debit card which gives them a secure MoBank PIN. The PIN can then pay for any services through the MoBank service.

This is a core focal point for MoBank who work with affiliate partners and earn a percentage of each sale as their revenue model. For example, the flower firm Interflora give MoBank 8% of any sale as a fee for distribution through their channel.

This fee payment from affiliates may be a far better route to follow than interchange fees, and is representative once again of another disruptive model of finance.

Shortly after launch, the service will also add further money management applications to pay bills and IOU’s, and transfer money between accounts, as well as features such as a birthday and special dates reminder alert, and a budget tracker to help keep track of spending.

What particularly intrigued me is that MoBank has had hardly any coverage to date, but the 35 articles that have featured the firm generated over ten million visitors to their message, many of them American.

Obviously there’s a lot of interest in mobile banking out there!

A few other details about MoBank from their press pack includes the details of their technical setup.

Agencymobile is MoBank’s application development partner; NTT Europe Online hosts the IT infrastructure; the current banking services are provided by Yodlee; and transaction fee services are provided by TxtTrans.

Finally, MoBank has already won a Red Herring 100 award for the best startups in the world in 2008, and won the Oxford University Saïd Business School Venture Fund Competition 2008.

Worth watching this space me'thinks.

Steve Townend will speak about MoBank at the FSClub’s Technology panel on 28th May, alongside:

- Richard Johnson, Chief Strategy Officer, Monitise;

- Perrine Fiorina, Research Associate, Celent; and

- Samee Zafar, Director, Edgar Dunn & Co.

If you want to attend, please register.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...