I hosted a dinner this week, where a group of senior bank executives

involved in cleaning up the PPI mess gathered to debate and discuss what had

been learnt from the experience.

For those overseas readers who are unfamiliar with the

situation, the UK banking industry has been caught out with a massive consumer

mis-selling exercise.

The exercise began with a simple product that was and is worthwhile:

Payment Protection Insurance (PPI). The

idea of the product is that if you borrow money – a loan or mortgage – then this

insurance can be taken out to ensure that your loan can be paid back if you

lose your job or are too ill to work.

That makes sense.

The problem came about when customers were sold these

products incorrectly, due to staff incentives and remuneration. The bonuses paid to employees for achieving

sales targets for PPI meant that some branch members became a little too enthusiastic. In some cases,

they even ticked the box for agreeing to PPI insurance when the customer had

left the branch, without the customer even knowing they were getting this

product or having to pay for it.

It was an interesting meeting, bearing in mind the cost of

this debacle which was originally estimated to be around £4.5 billion (BBC

News, April 2011) and now amounts to £9.6 billion (Mortgage Finance Gazette, June 2013).

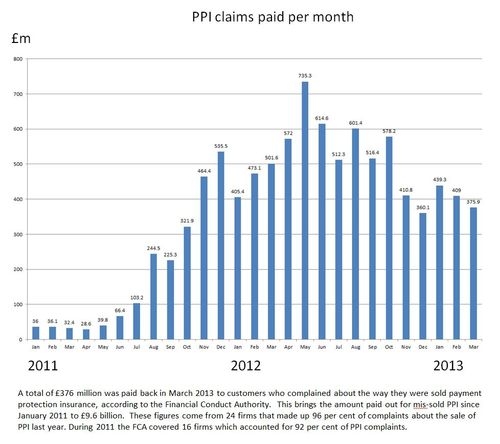

Interestingly, the first comment last night is that the claims

mountain has reached its zenith and is now tapering away, which is supported by

this chart that shows the monthly volume of processing claims (doubleclick image for larger version).

Nevertheless, there is a large scale Claims Management Industry

that has formed around this mess, and they are pushing hard for more claims to

be made.

Importantly, in this context, only one in ten policyholders have claimed so far, so there is still a way to go and, as a result, the end figure is going to way more than the current £9.6 billion, particularly if you add in the

cost of processing claims.

For example, Lloyds Banking Group’s annual results for 2012

showed losses of £570 million largely due to PPI costs. In their annual report statement, the bank

said that:

“The losses for the

2012 year were largely a result of provisions for mis-selling PPI, with the

bank setting aside a further £1.5 billion in the last quarter to take the total

provision to £3.6 billion for the 2012 year.

The bank said its total costs for PPI alone last year were £4.34

billion, which included £700 million in ‘administrative costs’. In total, Lloyds has now set aside £6.77

billion to cover PPI mis-selling claims.”

In fact, putting all the facts

and figures in context makes for stark reading:

About 34 million policies are

thought to have been sold since 2001, alongside personal loans, credit cards

and other borrowing. So far, almost £14 billion has been set aside by the big

sellers of the policies.

Lloyds Banking Group

- Lloyds Banking Group has made

the biggest provision for PPI mis-selling of any bank, putting aside £6.7

billion so far to compensate customers of Lloyds TSB, Black Horse Finance,

Halifax and Bank of Scotland. - By the end of 2012 it had

spent £4.3 billion on settling claims, of which about £700 million went on

administration - In the last quarter of 2012

it spent £200 million a month on settling complaints. - It has more than 6,000

employees processing PPI claims. - In February it was fined

£4.3 million for delaying compensation payments to 140,000 customers. - In June, the bank was further caught

out by a sting, where it was found to be purposefully delaying the

payment of claims and trying to persuade customers not to claim

HSBC

- HSBC has added £199 million to

its provision, increasing the total to £1.5 billion. - So far £757 million has been

claimed by consumers. - It employs 700 staff in the

UK to deal with the issue.

Santander

- Santander has put aside £538 million

to cover claims from customers who were with Abbey and Alliance &

Leicester. It hasn't increased its provision since July 2011. - It says it had just 6% of

the PPI market.

Nationwide building society

- Nationwide has put aside £173 million

to date and paid out £42 million of that. - This accounted for just 1.6%

of the total industry provision on 30 September 2012. - Of the claims the society

receives, 42% have never been sold a PPI policy – the majority of these (72%)

are through claims management companies.

Royal Bank of Scotland

- RBS has put aside £2.2 billion

to cover compensation to customers of RBS, NatWest, Lombard, Mint, Churchill

and Direct Line. - Customers have so far

claimed £1.3 billion. - About 1,800 staff members

are dealing with complaints. - In the second half of 2012,

51% of complaints by NatWest customers were successful, as were 45% of

complaints by RBS customers. - The bank started writing to

customers in September 2012 and will continue to do so throughout 2013.

Barclays

- Barclays has so far made a

provision of £2.6 billion across all of its brands, which include Barclaycard. - It has so far spent £1.6

billion settling claims, of which about 10%-15% has covered administration

costs. - About half of the claims it

gets from claims management companies are invalid. - About 2,500 members of staff

are working on PPI cases.

Overall, therefore, this mess is currently a £14 billion headache, and will be more than double this amount by the time it finishes.

So it’s pretty

serious although, as one attendee pointed out, it is also a failure of the

regulator as the first claims were made as far back as 1994 and so there was a

long period – 1994 to 2011 – where the regulator failed in their duty of

coverage of consumers.

Another pointed out that there

were similar scandals in other industries however, where people had taken out

insurances without due consideration.

This is illustrated in the consumer electronics markets where stores

sell insurance for repairs to white goods and electrical items, and many consumers

buy these products happily.

The result is that the stores

make their profits from the insurances and sell the goods at cost, and the consumer

has peace of mind.

That’s what PPI was all about,

so why are banks targeted as an issue here when the electrical stores are not?

In fact, it’s a good point that

I’ve raised before which is that it is not just an industry that mis-sells but, more often than

not, a case of customers also0 being guilty of mis-buying.

We ended up concluding that it’s

a sad indictment of the industry but, for consumers, it’s even worse as it probably

means:

1. an end to free banking, as

banks now need to make money via other means,

2. an end to gaining advice from

the bank as this debacle combined with RDR (the Retail Distribution Review), leaves banks

no longer operating a sales channel for financial products that require advice

3. an end to bancassurance, as

the cross-selling of insurance with banking has now become toxic.

All in all, a sobering lesson

about something that started with all the right intentions and eneded with all

the wrong outcomes.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...