It made me laugh today. I was chairing a panel where Romana Kumar, Head of Global Transaction Banking for the National Bank of Abu Dhabi (NBAD), was discussing their trial of Ripple. The background to this was announced in a press release on 1st February 2017:

Ripple’s Distributed Financial Technology fits within NBAD’s existing infrastructure and offers a secure end-to-end payment flow providing transaction immutability and payment integrity. Integrated to the NBAD’s innovative payments infrastructure, the Ripple solution offers customers end-to-end visibility of transactions and allow for the instant transfer of funds to a beneficiary in a cost-effective manner.

There was quite an interesting discussion about how this worked, as Ripple has been added to existing infrastructure? According to Ripple’s website:

REAL-TIME PAYMENTS WITH NO SETTLEMENT RISK: using Ripple’s solution, banks can coordinate funds movement across multiple ledgers to remove all settlement risk and minimize delays in the payment process. Having global reach through many nostro accounts is no longer necessary.

FLEXIBLE LIQUIDITY PROVISIONING: expand reach to new corridors with Ripple through more efficient liquidity sourcing. Either leverage existing nostro accounts for high-volume corridors that have competitive FX rates or utilize a marketplace of third-party liquidity providers.

LOWER OPERATIONAL COSTS: with Ripple’s bidirectional messaging, banks can validate transactions before funds are transferred and confirm delivery of funds, ensuring high Straight-Through Processing rates, low returns and negligible tracking and reconciliation effort.

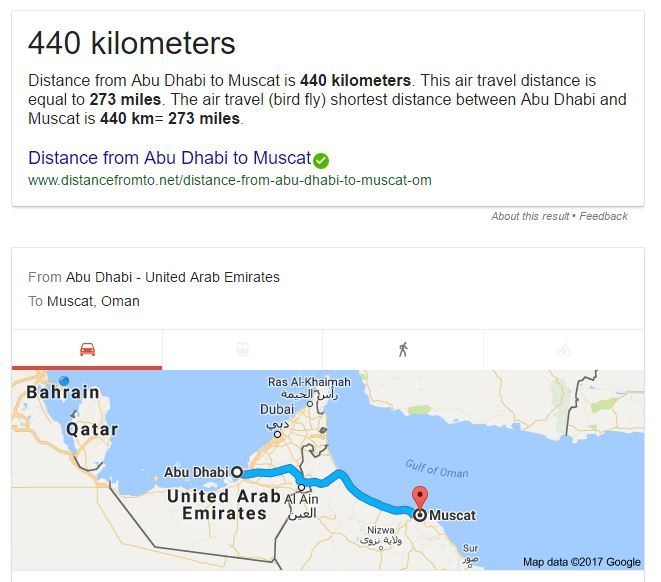

Lovely advertising. However, Romana articulated it well by illustrating the issue. They make regular payments from Abu Dhabi to Muscat, Oman. That’s 273 miles or a five-hour drive. Simple.

Except that it takes a minimum 24 hours and usually 48 hours for payments to wind their way through the counterparty network. If it’s a Friday, then you’re lucky to get it delivered by Tuesday. Imagine ordering from Amazon and waiting five days for delivery. Amazon works on speed. The payments system works on sludge.

That’s what got them motivated to implement Ripple.

"We can move money across borders in 4secs today & we believe we can get that to milliseconds" @marcus_treacher told @Chris_Skinner #emGCC pic.twitter.com/HEXLVhjHos

— Ripple (@Ripple) February 28, 2017

With the new upgrade, they can send payments from Abu Dhabi to Muscat in three seconds. Forget hours or days.

Then they went to their corporate customers and said: “we’ve upgraded our payments systems and you’ll find it works faster and cheaper”. However, instead of getting a hug and a thank you, most corporate clients rolled their eyes and said: oh no, I now have to call my ERP supplier and get a change made. I wonder how many millions this one will cost. Oh dear, poor cynical world-weary corporate treasurer.

The sell however, was to say how would you like to take the banks’ float off us. Instead of us spending one, two or more days sitting on your cash, you get it straight away in three seconds.

That worked and, if you want to know more on Ripple, I can recommend the white paper they released with Accenture last year.

There's also an interesting development related to this announced in Japan today, where 47 Japanese banks got together to roll out a consortium use case of Ripple.

SBI Ripple Asia announced today that a consortium of 47 banks have successfully completed a pilot implementation of Ripple in Japan using a cloud-based payments platform. This platform, RC Cloud, is powered by Ripple’s solution and is the first in the world to enable real-time money transfers both domestically and internationally. As a result, the consortium has confirmed that it will move into commercial phase.

Good stuff.

Meanwhile, to balance things out, there was another person on the panel I hosted: Lisa Nestor, Director of Partnerships with Stellar. Stellar is a Ripple competitor and you may ask: What’s the difference? More like what’s the similarity as both Ripple and Stellar were co-founded by the same guy, Jed McCaleb, and are both head quartered in San Francisco. From Wikipedia:

Stellar was based on the Ripple protocol. After systemic problems with the existing consensus algorithm were discovered, Stellar created an updated version of the protocol with a new consensus algorithm, based on entirely new code. The code and whitepaper for this new algorithm were released in April 2015, and the upgraded network went live in November 2015.

Hmmm … this Jed McCaleb is an interesting guy, having also formerly co-founded eDonkey, a decentralized, mostly server-based, peer-to-peer file sharing network created in 2000, and the failed bitcoin exchange Mt.Gox.

Now there’s plenty of bad blood between Ripple and Stellar in the past, as reported in The New York Observer. A particularly notable piece in their 15,000-word article of two years ago, is:

Until the beginning of 2014, Wells Fargo had a whole task force at its highest level comprising 20 of its top executives and advisors, including Susan Athey, a Stanford economics professor who sits on Ripple Labs’ board. They were marching forward to be the first U.S. bank to dive into crypto. All of a sudden, in March, just after the February collapse of Mt. Gox, they did a complete 180, shutting down the entire program that had been exploring crypto.

The Mt. Gox disaster was compounded by the legal entanglements of Silk Road, the bitcoin based exchange that was used to run a massive, anonymous narcotics bazaar. Just yesterday here in Manhattan, Silk Road founder Ross Ulbricht was convicted of all seven charges against him, including those usually reserved for guys named Gotti and Escobar—hardly the sort of names with which a Wells Fargo prefers to associate. Even more striking as far as Mr. McCaleb is concerned, Mr. Ulbricht’s trial revealed that the Department of Homeland Security long suspected that Jed’s friend Mark Karpeles, to whom he sold Mt. Gox, had actually been the mastermind behind Silk Road.

Predictably, Wells got cold feet. At the bank, the crypto blackout was so severe that it extended not only to shutting the accounts that cleared funds for crypto companies, but even those companies’ operating accounts—the money they kept around to put organic granola in the pantry and pay their electric bills—were shut down.

Mr. Larsen had used Wells Fargo for his previous companies, E-Loan and Prosper. After a 20-plus-year relationship, he was stunned to get a call telling him Ripple Labs had three months to find a new bank. According to Mr. Larsen, Ripple Labs’ banker at Wells Fargo told him, “The problem is your connection to Mr. McCaleb. The guy founded Mt. Gox. You’ve got to get that guy out of there or we won’t bank you.” Even though Mr. McCaleb hadn’t been involved with Ripple Labs since losing the “him or me” showdown in summer 2013, his continued involvement as a board member and major holder of XRPs was enough to make Wells Fargo skittish about Ripple Labs.

Yep, there’s bad blood in the past, but that is what it is. The past. Today, Stellar is doing pretty well too. A good example is Jed’s latest blog about using Stellar for Remittances, in partnership with Coins.ph, ICICI, Flutterwave and Tempo.

Today, you can send money to anyone in the Philippines over the Stellar network–for free ... you can create a payment to [any phone number in the Philippines] with the amount of Filipino pesos you want to send that person ... [and] they will receive the funds in 3-5 seconds. The recipient can cash out at any of Coins.ph‘s 22,000 locations.

Stellar is also backed by Stripe’s Patrick Collison, and that is notable in itself considering the success of Stripe (gossip: in the NY Observer story Wells threatened Stripe that they would unbank them if they didn’t disassociate from Jed).

So you have two major companies changing the payments world: one in the banking community (Ripple) and the other for financial inclusion (Stellar), at this stage, and both co-created by the same guy.

Rather than being forced to disassociate from him, I’m personally surprised that Wells Fargo didn’t hire him!

The New York Observer: Universally regarded as a ‘genius’ even by his detractors, Jed McCaleb helped create two landmark crypto companies that are now battling for supremacy—first Ripple Labs and now Stellar. He is precisely the sort of ‘surfer-dude man-child’ coders regard as a demigod. But with a long string of failed companies, broken hearts, and legal problems in his wake, time will tell if legit outfits like Stripe and Wells Fargo will bet on the man who created companies like Mt.Gox, which turned out to be the biggest fraud in crypto history. (Flickr Creative Commons)

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...