Barclays Bank wrote an article with the core message that tokenisation is moving finance from a world of messaging and reconciliation to a world of programmable, instantly settled value, which will be the most significant change to money since the arrival of electronic banking.

They argue that tokenisation is the next major stage in the evolution of money, following the progression from physical cash to electronic payments and now to digital assets that can move, settle and interact on blockchain-based networks.

The key point is that tokenisation is not really about cryptocurrencies. It is about representing money, deposits and real-world assets as digital tokens that can be transferred instantly, programmed with conditions, and settled without many of the frictions that exist in today’s financial system.

Funnily enough, that’s the focus of my other new book Diary of a Ponzi Scheme, which is all about a fund based upon tokens. Find out more here.

The vision is a financial system where money, securities, collateral and contracts all exist on the same digital infrastructure.

Barclays sees several advantages. Transactions could settle in seconds rather than days. Counterparty and settlement risk could be reduced because payment and asset transfer happen simultaneously. Smart contracts could automate processes that today require multiple intermediaries, reconciliations and manual checks. This would lower costs and improve efficiency across capital markets.

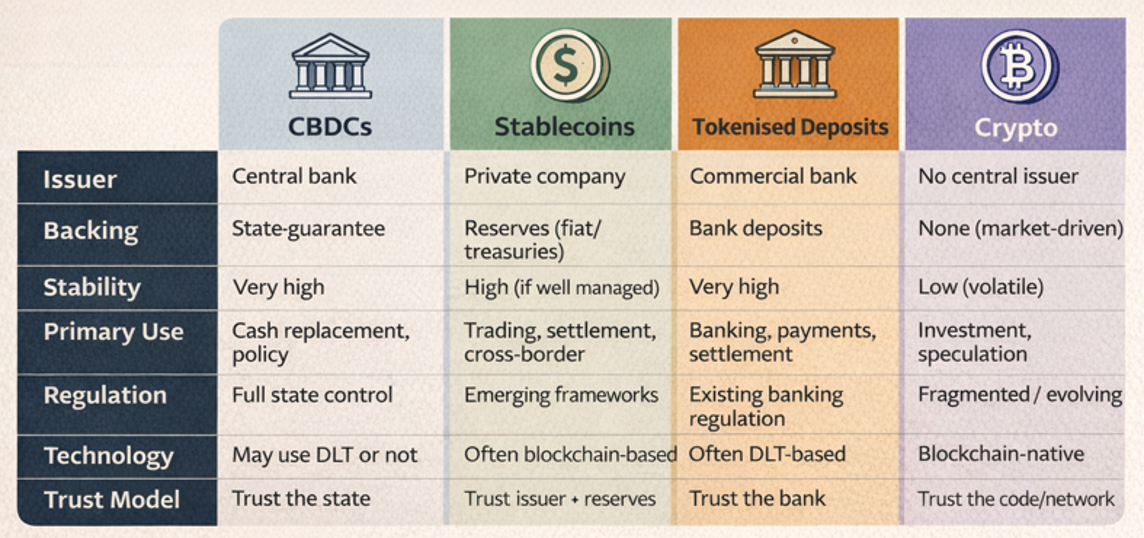

The article also highlights that the future is unlikely to be dominated by one form of digital money. Instead, it will probably be a layered ecosystem combining stablecoins, tokenised bank deposits and central bank digital money. Each serves a different purpose: stablecoins for fast movement of value, tokenised deposits for commercial banking activities, and central bank money for final settlement.

I have a slide about that …

… it’s all about who you trust, imho.

Importantly, Barclays believes tokenisation could unlock entirely new markets. Assets that are traditionally difficult to trade, such as private equity, real estate, infrastructure and other illiquid investments, could be divided into smaller digital units and traded more easily. This could increase liquidity and broaden investor access.

The conclusion is that tokenisation is not a niche blockchain experiment. It represents a fundamental redesign of financial market infrastructure. Just as electronic banking transformed finance over the last few decades, tokenised money and assets could reshape payments, capital markets and banking over the next decade. The challenge is not the technology itself, but achieving the regulatory clarity, interoperability and industry-wide standards needed for adoption at scale.

Hasn't that always been the case though?

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...