I just

received a report from the Economist Intelligence Unit (EIU) on new bank models

based upon different styles of banking in emerging markets.

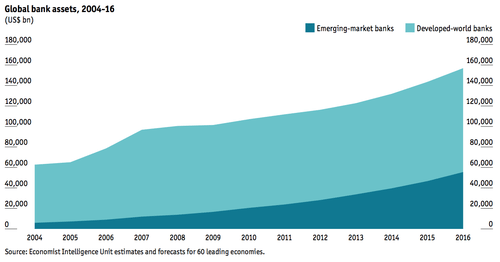

According

to the report, the BRIC economies and their brethren will account for 35% of

global assets by 2016, up from 24% today and just 10% in 2004.

Emerging

market banks are growing to fill a domestic vacuum. This is not surprising when you think that

these economies are spawning millions of middle-class, middle-income consumers

over the past decade.

This is

why there is enormous room for growth. In

China 64% of adults have a bank account.

In Brazil, the figure is 56%. In

Russia (48%) and India (35%), less than one in two adults uses banking services.

Similarly,

there are growth stories, such as M-PESA’s growth in Kenya. With 17 million subscribers, that’s every

adult in Kenya using the service, but more notable is that the number of banked

consumers in Kenya has risen from 2.4 million to over 9 million since the

launch of M-PESA in 2007.

In other

words, new business models are creating new styles of banking, as illustrated

by the reports’ introduction:

“New

technologies, innovative low-cost business models and supportive policy changes

will permit lenders to engage ever greater numbers of consumers in sustainable

and profitable ways. Many of these individuals will become users of formal

financial services for the first time in their lives …

A decade ago, few took notice of this

trend. After all, rich-country banking systems accounted for over 90% of

worldwide industry assets as recently as 2004, according to Economist

Intelligence Unit data. Emerging-market banks began to cut into their rivals’

dominance only slightly before the financial crisis of 2008-09, which marked

the beginning of a global shift in the industry. Developing-country lenders now

account for about 24% of global banking assets, and this share will increase to

over 35% by 2016, according to our forecasts.

Moreover, most growth in the banking sector

worldwide in terms of customers, deposits and lending now takes place in the

developing world. About half the world’s adult population lacks an account

at a

formal financial institution—that is, at a bank, a savings and loan association

(building society)

or a credit union—according to a recent series of household

surveys by the World Bank and Gallup. Although they differ among themselves,

many developing countries have only low levels of bank

usage and thus offer the

greatest potential to reach new customers and deepen financial sectors. For

example, in China some 64% of adults have or share an account, with lower

levels in Brazil (56%), Russia (48%) and India (35%).

By contrast, in developed markets most

adults have accounts, and any growth in customer numbers depends on population

growth and immigration (which are themselves often stagnant). For example, in

the United States 88% of adults hold accounts, with even higher rates of bank

usage in Japan (96%), the United Kingdom (97%) and Germany (98%). The industry

has recently been shrinking in many rich countries as banks trim loan books,

sell off assets and realign their capital ratios to meet regulatory

requirements.

In short, financial firms can no longer

ignore developing countries if they want to expand in growing markets. Those

lenders that insist on carrying on as usual are likely to be reduced to the low

profit margins that come from fighting over market share in stagnating or

declining markets.”

You can find a full copy of the report over

here.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...