In this guest blog entry Brett King, blogger at Banking4Tomorrow and author of the new book Bank 2.0, looks at what it means to live in an age where the internet is THE bank ...

In a quick straw poll recently conducted via Linked In we had a set of responses that confirms pretty much all the other data we are seeing in relation to channel adoption and utilization. The key issue is that despite the obvious data and conclusions, Internet is still seen as either the poor cousin of Branch banking, a necessary ‘burden’ or normally as a transaction channel for cost reduction – rather than what it is today…a customer channel.

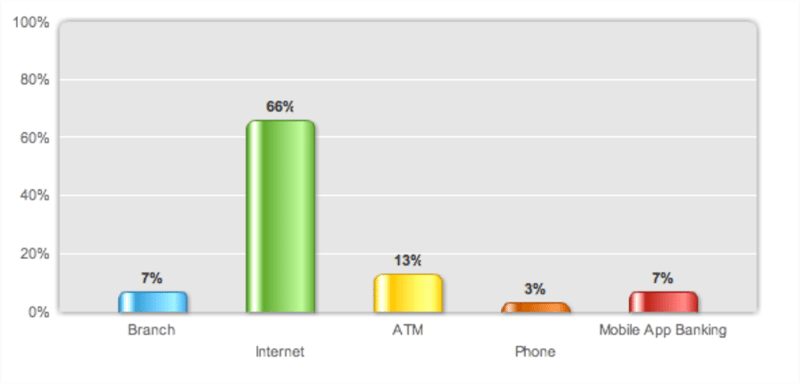

The question we asked in the LinkedIn poll was very simple. Which Channel is the most important for your day-to-day banking needs? The answer was clearly Internet banking.

Poll Results - Which channel is the most important for your day-to-day banking?

Now, the conservative bankers amongst us might think that asking for people to participate in an Internet survey guarantees results skewed towards the ‘internet’ and to be honest this is not a rigorous piece of multi-variate research. However, even if you factor in that in most developed economies Internet Penetration is at 65-75%, that Internet Banking is hovering around 40-50% of the populatio and that the highest demographic of users of social media online are the coveted 35-44 year old age bracket, why would you bother arguing that Internet is not a significant channel for retail banking today?

Let us use some very simple logic. Even in the US where Internet Penetration looks as if it has started to flatten out in the last few years around the 75% mark, is it reasonable to think that Internet Banking is likely to decline in usage in the near future, or is it likely that as more people shift to internet banking via mobile phone that it will continue to increase?

Patrick Chew, Head of Delivery from OCBC in Singapore, was reported in the Straits Times this week saying

“Mobile banking customers are no longer only professionals, the technologically savvy or those who are better educated…these customers now come from all walks of life.”

Patrick Chew, Head of Delivery, OCBC Bank Singapore

In Singapore already OCBC has the majority of it’s customers on Internet Banking and expect within 2 years that approximately half of their customers will have migrated to mobile banking. Daniel Li, Director of E-Business at Citibank in Singapore, indicated similar plans, saying that one in 10 of their customers will be on Mobile Banking by the end of the year. Bank of America has had phenomenal growth in Internet banking with their user base now approaching 4 million users. A recent survey by mBlox showed that already mobile internet banking has surpassed both branch banking and traditional telephone banking in terms of usage. Internet Banking surpassed branch in respect to transaction volumes back in 2003, so that battle is long over.

But do banks really know what they are doing online? Do they understand the value proposition given that Internet is now the primary channel for the majority of customers? It appears not.

Look at the table below. It illustrates number of page updates made to the primary domain of major retail bank websites in 2005 compared with 2008. In every case, mysteriously, the major retail banks have scaled back on their commitment to Internet since 2005 reducing the number of updates they have made by about 50-75%. This is a worrying trend – it most likely signifies three things. Firstly, banks are over the initial ‘buzz’ around internet, further reinforcing the perception that it is actually mainstream. Secondly, that they don’t know what else to do, all the initial experimentation, etc has been done – what new tools do we have in the toolbox to deploy? Lastly, there has been consolidation of a lot of content that just wasn’t useful online. But, this does closely correlate with budgets online – they aren’t increasing. If anything they are decreasing.

What happened? Reduction in web banking spend has been universal...

Branch expansion is once again slowing too in the US, UK and many other markets (see FDIC:Quarterly). This is argued to be a function of cost reduction and the effects of the recession, but we can’t discount behavioral shift as a key element of this development. Yet, traffic of each of these sites has increased significantly in the same period with Internet Banking usage doubling globally in the period 2004-2009.

One global bank I met with in the last few weeks told me in confidence that they have budgeted US$800m for branch related costs this year, but less than US$8m for web, internet banking, social media, web marketing and mobile banking. What was the business case for spending 100 times more on digital versus branches – it is a function of existing infrastructure. The same bank realizes that today the Internet contributes as much revenue as the branch, and does 300-600% more transaction volume. But can’t conceptualize that Internet and mobile is underfunded.

So let’s get this straight. The web is now the dominant channel for customers. Internet and Mobile banking are growing at significantly higher rates than branch banking, branch growth is leveling off and yet we are not leveraging non-branch channels for revenue. In fact, Bans are reducing spend on non-branch because of the financial crisis.

There is something seriously wrong with this picture. First of all, banks need to realize that 80-90% of the daily traffic that comes to their site goes straight for the login button and that a great deal of time and effort needs to be spent on understanding how to sell behind the login to existing customers. I would argue as much time and money needs to be spent on cross-sell and up-sell within Internet Banking as we currently do training staff for the very same within branches – at least as much, if not more. Secondly, Banks need to better understand what customers actually want to do through internet banking and mobile internet banking. Let’s not assume it’s just checking account balances, paying bills and doing transfers. Let’s think about which products suit these channels and would make the lives of our customers easier.

Remember the two key drivers for Internet usage are convenience and price. The key driver for mobile internet banking is still convenience, but increasingly mobility itself.

Banks are getting this wrong because they are measuring the wrong things internally. They are busy measuring how much revenue increased channel by channel, product by product, and t

hey aren’t looking at the big picture nearly anywhere near as effectively as they should. They are still thinking like the bank of the 1990s when branches continued to be the primary channel because customers had no choice.

Today we have a choice!

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...