Further to my write-up about Wonga the other day, I have been contacted by author and campaigner Steve Perry, who has been on the wrong side of the payday loans industry.

Now don’t get me wrong.

I am NOT against payday loans firms or their operations (I actually admire Wonga's technology ops).

I AM against the uncapped interest these firms charge on their vulnerable customers.

However, this also needs to be qualified in terms of who are 'vulnerable customers' and who actually charges 'rip-off' rates and how.

For example, Wonga have also contacted me to put their side of the story and made clear that they do not target 'vulnerable' people with 'rip-off' rates.

Read Monday's blog to see what their take on the world is, particularly as my original piece was kicked off by the Wired magazine coverage of Wonga.

In that coverage were two issues.

First, the line in the article that stated: “within a year, Wonga had issued 100,000 loans, worth £20 million, earning about £15 million by charging interest at an eyewatering headline rate.”

I had a fundamental issue with a firm making those sort of rates of profits on loans, but Wonga tell me their margins are nowhere near these levels and, having met with them, I will take that as fact.

Second, the star letter that followed in Wired the following month saying: “When I could no longer repay a Wonga loan, it took 50 days of ringing and emailing to get through – an £800 loan became a £1,700 repayment.” Steve Perry

As mentioned, Steve contacted me following the blog entry and I discovered that he is a person who got into serious trouble using payday loans. Wonga tell me they are not a payday firm, which again I will explain on Monday.

But let's look at Steve's story.

Steve borrowed £15,000 in a year from payday loan firms. This led him to be in serious schtuk, and having to pay back £22,000. In other words, even though he tried hard to manage it, he was being charged extortionate interest rates and, having nowhere else to turn, spiralled into debt by borrowing off one payday firm to pay back another,.

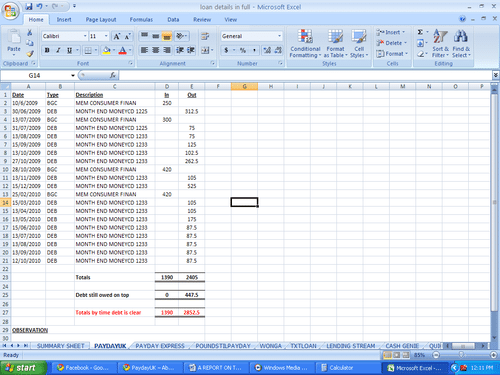

In one instance, he borrowed £1,390.00 from PayDay UK between June 2009 and February 2010; he paid back £2,852.50 over 15 months.

Due to losing his job and trying to manage his commitments to payback PayDay UK, Steve unfortunately then borrowed from another payday firm to pay back the first payday firm.

In July 2009, he borrowed £160 from Payday Express. By the end of his borrowing with them – October 2010 – he had taken a total of £1,225.00 in payday loans and had to pay back £1,975.00. This is over 15 months.

Again, the uncapped interest on payday firm operations is illustrated well as, so far, Steve has borrowed £2,615.00 over 15 months which, with a bank, would incur interest payments of around £650 max but, through payday firms, incurred interest of £2,212.50.

It’s the difference between average APRs of around 19% versus 90%.

One of the points Steve raises is that the payday firms do not take into account your other financial commitments, whereas banks do. If you have borrowed to the hilt, a bank will take this into account and refuse you a loan. Payday loan firms do not ask about your commitments and this means that you can borrow off all of the payday firms to pay back each one. In so doing, you just become more and more of a victim, and that’s what happened to Steve.

He ended up borrowing off other firms to keep up and make the payments to the first.

So then came Lending Stream.

Steve borrowed £200 off Lending Stream in June 2010 and, by November 2010, owed them £1301.10 on borrowings of £640.00.

The interest was more than double the borrowings in just under five months.

He borrowed from several other firms and found each had nuances by which they made more or less money.

Over a period of 21 months, Steve ended up borrowing from 12 payday loan companies, who made and approved 64 individual loans to him with no knowledge or interest in each other’s activities or his other financial commitments. The result was that he had to repay £21,707.49 on loans of £14,886.00.

Now Steve admits he was a mess … but he became a much worse mess due to the unregulated state of the UK’s payday loans markets.

As Steve says: “It has been apparent throughout, a fact in which I have never denied, that I am the chief architect of my own demise. Whilst I felt I had no other avenues to take, the harsh reality is that I chose on each of those occasions to take payday loans and sign agreements stating immediate repayment on the set payment dates. However, responsibility of borrowing of this magnitude, on this scale cannot possibly lie totally at the feet of the desperate borrower. A fact that cannot be ignored is that on 64 separate occasions, over the period of just 21 months, a total of 12 different payday loan companies were more than happy to instantly approve loan payments to me, with no questions asked.”

So what should be done about this?

For me, the #1 issue is uncapped interest rates.

Most countries impose limits on the interest payday loan firms can charge.

- 37 American states allow payday lending, whilst 13 have made it illegal;

- In those American states where it is legal, there are hard interest rate caps;

- In Canada, any rate of interest charged above 60% per annum is considered a criminal act, according to the Criminal Code of Canada; and

- The Australian states of New South Wales and Queensland have a 48% APR maximum loan rate, including fees and brokerage.

In the UK, 1.2 million people took out 4.1 million loans in 2009, four times the level of 2006,with total lending of £1.2 billion. The average loan size is around £300, and two-thirds of borrowers have annual incomes below £25,000.

And there are no restrictions on the interest rates payday loan companies charge.

Steve makes many more recommendations which you can read in his 70-page overview of the UK industry (provided on request).

These include:

- More qualification of the borrower and their other financial exposures, particularly for repeat customers;

- Capping of the amounts that an individual can borrow, not just from a single lender but from across the industry; and

- Better structuring of rollover of interest and transparency so that the vagaries between lenders is clearer.

The net:net is that as Vince Cable talks about the banks' “rip-off culture”, maybe he ought to look here a little too?

Meanwhile, I won't damn the industry completely as Wonga have proof that sets them apart from the payday pack. That proof shows that they are not one of the bad guys, which I'm pleased to hear as I've watched them from their first days of operation and was surprised to hear they were making eye-watering margins.

They're not.

I will explain more about Wonga's operations on Monday.

Nevertheless, the core debate here is whether these markets are working well and whether customers are being protected from potentially damaging practices by some of these firms.

My view is that they are not in the UK.

This means that these markets need regulating and regulating fast.

And that is a fact.

Postnote:

Follow Steve Perry on Twitter and/or join his campaign - Say No To Pay Day Loans.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...