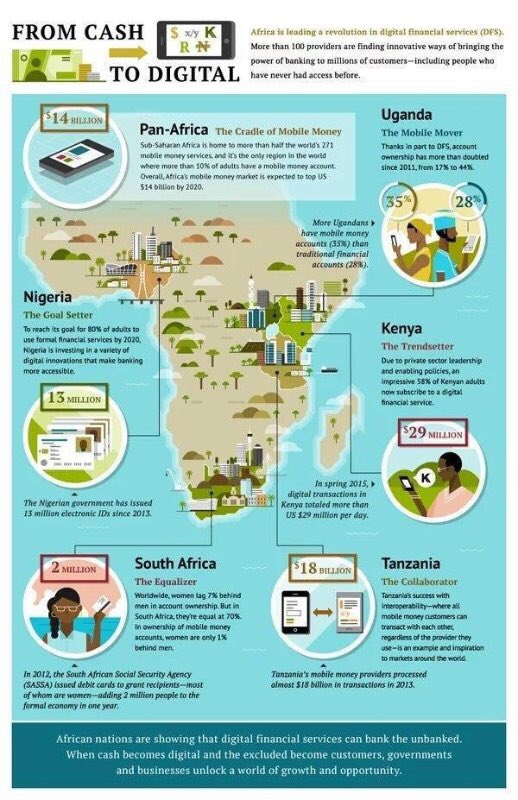

Last week I chaired the inaugural Dot Finance Live conference in Nairobi, Kenya. It is Africa’s premier FinTech event, drawing people from all over the countries of sub-Sahara Africa. What struck me as I listened to lots of keynotes about mobile innovation and mobile financial inclusion, is that Africa is actually leading the world in financial innovation. This is because Africa is a continent where the majority of people were previously excluded from financial service.

For example, according to data from the World Bank in 2015, only 17.9% of people in Sub-Saharan Africa had debit cards dropping to just 6.6% of the lower income population.

That’s a problem as the poorer you are, the more you have to pay for transacting and transmitting. For example, the average remittance cost of sending money from Kenya to Uganda is over 10% if performed through a bank and 8% through Western Union. In fact, The cost of sending money back home to Africa is higher than anywhere else in the world. The World Bank’s Migration and Remittances Factbook for 2016 shows the global average cost of sending Sh2,000 ($200) home was about 7.4%, down by 0.6 percentage points from the end of 2014 but still way to high as Sub-Saharan Africa’s average remittance cost is 9.5%,the highest in the world and over 25% more expensive than other developing countries.

Part of this is the archaic financial system, which fails in most correspondent banking structures due to international sanctions and fear of exposure to money laundering and terrorist funding due to a lack of digital identities and Know Your Client (KYC) documentation. How can you perform KYC on someone who lives off the land or in a village with no digital inclusion?

That’s the challenge that many were addressing in their presentations this week, and it is the reason why Sub-Saharan Africa is the cradle of mobile money.

For this reason, I am going to spend much of this week focused upon talking about African innovations in mobile. It’s not just about mobile financial inclusion however, but about mobile financial innovation generally. For example, Standard Bank rolled out SnapCash a couple of years ago. SnapCash is a method of paying via the mobile camera and a QR code.

It’s a great app, and is described well by this article from Time Magazine:

A free app available for any smartphone, SnapScan works almost like a pocket ATM linked to the user’s debit or credit card account. Instead of handing over a card, customers scan a unique SnapScan logo posted at the cash register with their camera-enabled phone. They enter the amount, type in a pin code (or use touch ID) and a few seconds later the vendor’s phone chimes with a confirmation sent by SMS. It’s quick, painless, and entirely safe … as a result, SnapScan has been adopted by about 12,000 small and medium businesses in more than 17,000 outlets across South Africa. (Apple Pay, by contrast, so far only deals with less than 100 major retailers in the US, but can be used in their multiple branches across the country) SnapScan has 150,000 registered users, and processes hundreds of thousands of dollars in payments every day for everything from airline tickets to handcrafted wicker baskets at roadside curio stalls.

SnapCash isn’t the only African app doing well. For example, Ghanaian FinTech start-up Zeepay is offering an NFC based app for paying by phone. Think of it as Apple Pay without the Apple and you get the idea.

Anyways, as mentioned, this week will focus upon these and other innovations in African finance, starting with the plans for mobile financial inclusion from Kosta Peric, Deputy Director of the Bill & Melinda Gates Foundation, tomorrow.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...