I talk to a lot of wealth managers and private banks. They want to lead in digital as their clients are the coolest, richest people on the planet. It used to be that everything for a high net worth (HNW) client was face-to-face; now it’s skype-to-skype; tomorrow it’s machine-to-machine.

The large wealth managers, private banks and investment advisers have therefore all embraced digital. It wasn’t the case a few years ago. Interestingly, I just spoke at the ObjectWay conference in Amsterdam, where they released their 2016 research into digital trends in wealth management, in partnership with EFMA (you can read last year’s report here). The research surveyed institutions in 27 countries who look after HNW and affluent clients, with 1 in 5 participating institutions holding over $50 billion in assets under management (AUM), although most (46%) held less than $20 billion AUM.

The standout answer for me was the answer to this question: What is your organisational strategy in relation to digital engagement and collaboration? 46% of those answering said it was a board level commitment. 90% of institutions were working on digital – only 2% said they have no strategy – and digital engagement, according to the report, is a strategic topic with boardroom commitment.

I would challenge that statement. After all, as I blogged the other day, banks need to reboot their boardrooms and private banks and wealth managers are no exception. I’ve been into Switzerland’s boardrooms many times and haven’t seen any technology guys in the C-suite so, if digital is a strategic topic with boardroom commitment, where’s the technologists in the boardroom?

It struck me that this is what I hear so, so often: digital is a strategic program and we are committed. No, you’re not. You’re just saying that. Committed is when half the leadership team are technologists and half are bankers. Then you are tech and fin. If you’ve got 10 people in the C-suite and only one of them is a technologist, and more often none, then you’re not committed. After all, how can you embrace digital if you’ve got no one in the C-suite who understands a blockchain?

Anyway, a survey is a survey and so the next question intrigued me: Who asks for digital engagement? 28% of HNW clients and 47% of the mass affluent are asking. So there is a customer need for such engagement, although its higher amongst the wealthy rather than the uberwealthy. What intrigued me is that almost on the same page is the question: Rank the channels you use to interact with clients, and Branch-Based Advisor was #1. Really? When you’re saying digital is serious and half your customers want it as their mainstream connection, you really think coming along to the branch for a chat with an advisor is still the way to go.

I’m not having a go at this research – it’s interesting – but I am having a go at the wealth managers. Admittedly, they did put Mobile Advisor as their second choice. Then I had to think: does that mean an advisor on a mobile app or an advisor who goes around visiting clients which means they’re mobile?

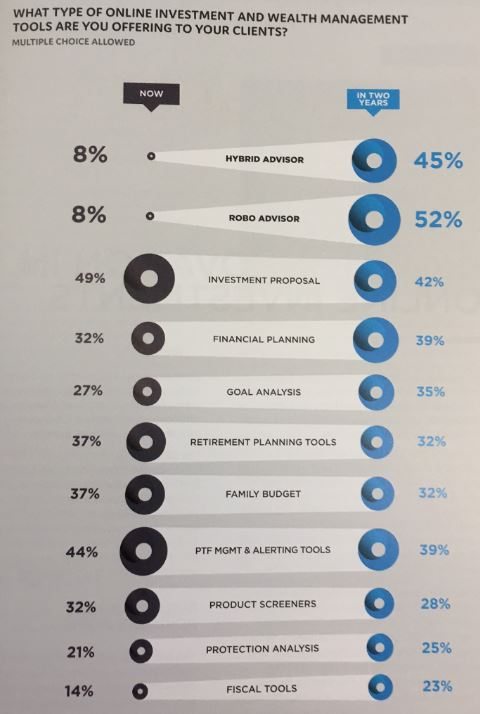

There’s then a section on the type of investment and wealth management tools offered to clients. Intriguingly, they all think they’ll be offering a hybrid of human and robo advisory services over the next couple of years …

I must admit that the rise of robo advice may have caught out the industry, but the industry has adapted and adopted such technology pretty quickly. In fact, the roboadvisors start-ups are struggling now, as the heavy hitting teams of Charles Schwab and co take over.

https://intelligent.schwab.com/

Interestingly Charles Schwab also held a recent conference of their investment advisors and released research that confirms the hybrid robo-human advisor is here. Schwab surveyed 500 financial advisors in all sectors of the market from independent advisors to insurance and wirehouse producers. The results of the survey included:

- About 60% of advisors believe that they can reach additional markets and expand their businesses through the use of automated investment platforms.

- More than 80% of advisors plan to provide their customers with pricing that is based on assets and 64% of these advisors said that their automated model would be cheaper than their standard model.

- A low percentage of advisors plan on going completely digital. Most advisors plan on coupling their automated investment services with regular client interactions in order to provide a more holistic experience.

For me, it’s a sobering experience as way, way back in the annals of time a certain pseudo-intellectual called Chris Skinner predicted that human advisors would disappear. This was a prediction made when call centres were appearing and consumers could get direct service. Why would a consumer go to an intermediary for advice, when they could self-serve direct?

Oh how wrong I was. Therefore, my prediction is that all the technology developments we deploy will be there to supplement and augment the human touch. That’s what robo advice is doing in wealth management, and it’s pretty much what FinTech is doing in P2P lending, payments APIs, social trading and investing and more. It’s all about making it easier to talk, trade and transact with other humans.

Now, when machines start trading with machines …

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...