My good friend Jim Marous who recently joined The Financial Brand, asked me to make a comment about this new report from Bain.

It’s not a bad report and is a slight improvement on this one from McKinsey on The Rise of the Digital Bank, but it’s not as strong as what you will hear from leading digital innovators.

So Jim kindly asked Brett King and I to provide input on the report, and here's the result. Interesting.

Financial Institutions Unprepared For Digital Future

July 21, 2014

There is no question that banking is quickly becoming a digital business, supported by enhanced online and mobile offerings from traditional financial institutions as well as new market entrants. But how ready is the banking and credit union community for this transformation?

By Jim Marous, Editor, Retail Banking Strategies

According to a Bain & Company report entitled, “Building the Retail Bank of the Future,” more than half of the 78 global financial institutions benchmarked lag substantially in the ability to create the “bank of the future” experience that customers already expect – integrated, on demand, real-time banking services via a combination of digital and physical assets.

Bain found that while many banks have focused their digital investments on digitizing transactions that reduce brick and mortar cost, less has been done to make consumers’ banking experience more convenient, easy and engaging through a seamless integration of channels. While consumers have definitely appreciated digital innovations such as remote deposit capture, remote bill pay and other simplified transactions delivered through a mobile app, winning the digital consumer in the future will require more.

“The biggest threat the digital pure plays present to incumbents is that they don’t have hang ups about cannibalizing branch networks and how the requisite shift in revenue delivery will compromise the business case for branches,” stated author, speaker andMoven CEO/Founder Brett King in an interview with The Financial Brand. “In fact, while lower acquisition costs and lower distribution costs are key metrics for neo-banks and P2P lenders, their ability to generate business purely through digital is the biggest single threat to the existing model of retail financial services.”

The impact of not being able to provide the digital capabilities customers desire is difficulty in defending against more nimble, low-cost, digital-only entrants that are increasingly grabbing market share. The cost of losing these digital natives can be high.

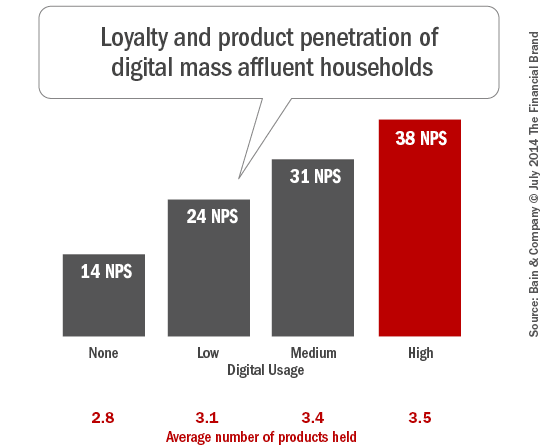

In fact, in a survey of 77,000 banking consumers, Bain found that consumers who conduct the most digital transactions also have the greatest satisfaction with their banks (as measured by Net Promoter Score) and do more business with them as well. As shown below, customer loyalty scores were nearly three times higher for digitally-active customers than for less digital counterparts. There was also a correlation between digital channel use and affluence.

Integrating Digital With Physical

While digital channel use will increase in the future, they will not fully replace physical channels, according to Bain. The number of branches will continue to decrease and the role and structure of branches will continue to evolve. Branch networks may be organized around a ‘hub and spoke’ configuration, with far fewer full service flagship branches being surrounded by smaller branches with limited functionality. These branches could be supplemented by video call center technology that links customers with more complex needs to remote experts.

Chris Skinner, Chairman of the Financial Services Club and author of the book, Digital Bank told The Financial Brand, “A digital bank has to be built with a digital base. Interacting with the bank is then through various form factors – human, machine, device and chip. It is not about adding a new channel – mobile, tablet, social, app – to the old ones … that’s the wrong thinking. Digital infrastructure (the web) must be at the core.”

In what Bain refers to as DigicalSM (digital+physical) transformation, some leading banks are transforming their core business – including products, channels, back office technology and organization – funded by the reduction in legacy costs and systems. Some banks have gone farther to reinvent the customer experience and provide new ways to engage and add value to customers, sometimes partnering with technology start-ups to accelerate innovation and create new propositions.

Skinner agrees that organizations should fund their reinvention of core infrastructure to be web-based through freezing legacy upgrades. According to Skinner, “The savings per annum in upgrades and maintenance should then be used to fund moving the data to the cloud and creating APIs and apps that leverage that cloud-based data.”

Digital Pure Play Competition

The need for traditional financial institutions to provide better digital banking is no longer an option as low-cost digital-only entrants are taking market share. Anthemis Group, an investment and advisory firm for digital financial services companies, tracks 3,000 such companies worldwide. The impact in financial services is similar to what happened in industries like music, retailing, and travel. Bain clustered the digital pure play competition into three groups:

- Aggregators redefine the interface between traditional banks and consumers, providing added value while squeezing profit margins. Moneysupermarket, Mint and CHECK24 bring transparency to pricing and product features, and could become a primary interface.

- Innovators use existing technology platforms, but leverage innovative sales and service platforms. Square, Paypal, Starbucks and many of the players in payments take what was once considered ‘marginal’ business away from banks, potentially reducing banks’ function to simply processing transactions.

- Disruptors such as Simple, Moven, Serve and several players overseas provide alternative products and services, leveraging mobile to provide a better overall experience. Starting with a mobile-first perspective, they threaten banks’ economics in market niches that prefer a digital platform (see correlation between sales, loyalty and affluence above.

Making the infiltration of traditional banking strongholds easier for digital pure play competitors is the reality that shopping for financial services now begins begins online, that the power of bricks and mortar is crumbling, that the trust in traditional banks has been reduced and that traditional banks have been slow to respond to the needs of the digital consumer.

Imperatives for Building a Stronger Bank

Bain’s research provided five imperatives that are essential for building a strong ‘bank of the future.’

1. Combine digital and physical capabilities for a differentiated customer experience

Instead of deploying technology to replicate previous processes in an online or digital world (usually to reduce costs), customer-centric digital banks combine the best digital and physical assets to make consumers’ banking lives easier, more convenient and more engaging. In Chris Skinner’s words, “The bank does not become digital through technology. People are what will make the digital bank.”

For instance, in South Korea, Hana Bank has innovated around a core of “moving money.” The Hana N mobile platform serves as a full-service bank in a smartphone, working seamlessly with Hana’s branches. Customers can withdraw cash from ATMs via their smartphones, parents can send money to their children via their mobiles, and N money includes near-field payments technology that can be used to pay at many stores. There is even a platform that offers integrated money management, location-based offers and coupons, as well as the ability to borrow for larger purchases while in the store.

2. Rebuild the branch network … smaller, leaner, seamless

With teller-assisted transactions declining at an annual rate of 10% to 15% for many institutions, optimizing the branch footprint is an imperative, with some organizations needing to shrink their branch network by as much as 30% over time. Unfortunately, for a US bank with 1,000 leased branches, the cost of closing 30% of a network might cost up to $120 million.

Many organizations are either implementing or considering a hub-and-spoke configuration that includes centralized full-service advisory offices, smaller retail branches with limited functionality and self-service kiosks. Each of the new formats incorporate digital technologies to enhance the customer experience and provide self-service capabilities that customers increasingly expect. Some spoke formats have removed bank tellers altogether. According to Bain, 40% to 60% are adding in-branch tablets, video teller machines, smart ATMs, etc.

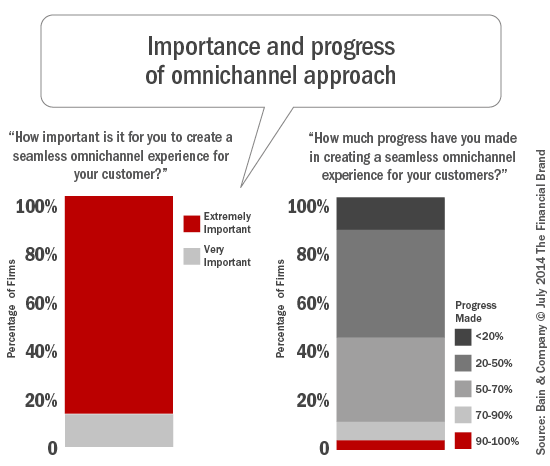

The term ‘omnichannel’ is both misused and misunderstood as it relates to becoming a bank of the future. Chris Skinner has been outspoken in his distaste for the term, calling it ‘last century’ and hoping it will simply go away. “What banks need to do is put the consumer at the center of the engagement process and ensure that the experience is seamless with digital (web) at the core,” says Skinner.

The challenge grows more complex as banks introduce more solution specific mobile apps, or digital form factors based around communities of humans. With more diverse needs come more coordination across channels. But from the consumer’s perspective, seamless channel connection is nonnegotiable.

3. Overhaul the technology platform to simplify consumers’ lives

It’s impossible to build a strong solution on a weak foundation. Unfortunately, this is the case at most financial institutions that are trying to deliver a ‘bank of the future’ solution with a core processing system that is decades old. Bottom line, to deliver a differentiated, seamless experience to customers, most banks will need to make substantial improvements to their IT infrastructure to eliminate data silos, duplicative and/or incomplete customer data files and incompatible systems.

The new infrastructure must allow different departments and functions to share a uniform 360 degree view of the customer data. This will also allow all frontline employees to see the entirety of a customer’s history with the organization. Organizations also need to implement technology that supports one-and-done processes and speeds up transactions by processing them in real time rather than in batches.

Unfortunately, only 60% of financial institutions benchmarked by Bain reported having IT upgrade plan with clear budgets and allocated investments.

4. Fund the transformation by halting legacy funding

The change recommended to move forward does not come cheap. Institutions that are moving forward are funding change by simplifying their product lines, processes and organizational structure. They’re also selling real estate (branches), reducing staff, and streamlining operations.

The boldest of financial organizations have gone as far as moving funding that was allocated for projects related to their legacy infrastructure to projects related to improving the new digital interface with customers. Again, the reality hits home as Bain found that only about half of the benchmark organizations fully understand the cost of digital change for their business, with less than 60 percent of the benchmarked banks having a budget.

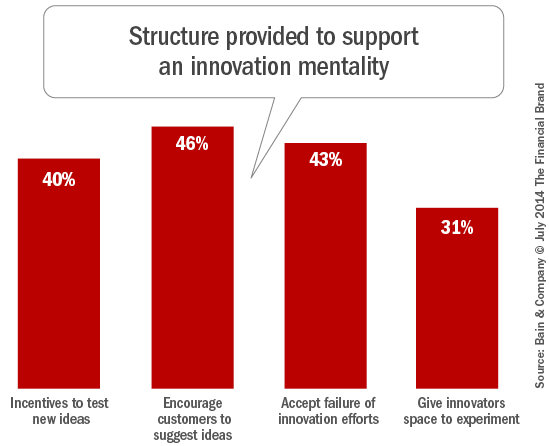

5. Reorganize to encourage innovation and change.

Silos are the enemy of innovation and change. Innovations that are product, department or functionally based will deliver just a fraction of the potential benefits. According to Bain, 70 percent of the benchmarked organization organized “digital” as a standalone department. While this may sound like a way to focus resources, the standalone structure usually hinders the objective of an overarching transformation. Remember, digital is not a channel.

Asked whether they exhibit common innovation requirements, such as incentives to test new ideas, freedom to experiment and tolerance of failure, fewer than half of the benchmarked organizations said they did. Another disconnect is that digital channels are seen as competition to the branch network, with manager sales incentives creating a conflict within the organization. The branch staff also sees digital as a threat to their future.

Some institutions have set up innovation labs that are separate from the core business, with freedom to explore external deals and relationships. BBVA, for instance, acquired Simple and invested resources in a strategic alliance with SmartyPig. BBVA also has invested in start-up accelerators.

Meeting the Needs of the Digital Consumer

The digital consumer no longer sets their expectations based on other financial institutions. Their expectations are being formed by the experiences and delivery of products and services from non-banking organizations like Amazon, Apple, Uber, Zappos and even Disney and Southwest. Physical branch networks are no longer structured for a digital universe. They are costly to run and costly to change.

Time is running out. Digital pure play competitors are gaining recognition and building a base of customers. In effect, the market is moving faster than most banks and credit unions can keep up.

Most industry observers believe traditional banks can leverage their historical strengths and still compete effectively. But, it will require laser focus and the commitment to rebuilding internal and external business models around consumer priorities leveraging digital technologies.

Chris Skinner has a warning however, “Remember that digital just augments the interaction and takes away the friction – or should – and is not the be all and end all. But once you’re committed to digital, make sure you design it for humans.” Brett King is even more direct when he told The Financial Brand, “If bank and credit union executives don’t have a plan to deliver more than 50% of their revenue across digital by 2020 – then it’s time to start packing bags and beefing up resumes!

Brett King is a global bestselling author, futurist, speaker, host of the “BREAKING BANK$” radio show on Voice America and the founder of the start-up Moven. He is widely regarded as one of the world’s foremost experts on retail banking innovation today. King was voted as American Banker’s Innovator of the Year in 2012, and Moven was nominated by Bank Innovation as one of the Top 10 “coolest brands in banking”. His book, BANK 3.0, has been a best seller since its release late in 2012. His latest book, Breaking Banks, has just been released. He can also be found on Twitter.

Chris Skinner is best known as an independent commentator on the financial markets through his blog, the Finanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He is also Chief Executive of Balatro Ltd, a research company, as well as a regular commentator on BBC News, Sky News and Bloomberg about banking issues. He can also be found on Twitter.

Jim Marous is a recognized financial industry strategist and publisher of Retail Banking Strategies for The Financial Brand. Marous publishes the Digital Banking Report and is a consistently highly rated speaker worldwide, presenting on global trends, distribution strategies, customer experience, digital banking, advanced marketing and marketplace disruption. You can follow Jim on Twitter andLinkedIn.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...