In this world of choice that emerges from the integration of new technology models and old financial models, we see hybrid systems emerging that bring together the best-of-the-best. A great example was announced today, as Metro Bank and Zopa join forces. The deal allows deposits from Metro Bank retail customers to use P2P lending as an asset class for their deposits, with the expectation that this will provide higher returns on their savings. It’s an innovative deal in that P2P lending surely cannibalises that other asset class: credit. But it’s all about choice and if customers know that they can place money in Zopa, then why not allow them to do so through the intermediation of the bank to assure its viability?

This is where it gets interesting as I’ve seen innovative deals like this before. Fidor Bank (Germany) has been offering Smava’s P2P lending for some time through its operations whilst Caja Navarro (Spain), a non-profitable foundation, offered its own version of P2P some years ago. They called this Civic Banking and gave every customer the right to know the profit they made from each transaction and account. Through Civic Banking you could also invest in friends and family businesses and loan requests, with the bank ensuring the loan was repaid.

This is the point I am making when talking about aggregating the customer experience. If a customer has so much choice these days, do they really want to be opening accounts here there and everywhere with eToro, Circle, PayPal, Zopa, Friendsurance etc, or do they want to have an aggregator on top? I think the new emergent form of retail bank will be that aggregator. Like a Trip Advisor for travel, we will see front-end services that integrate many back end providers for finance. Some may say that this is just what the comparison websites do, but the comparison websites are not integrating and aggregating. They are just providing a rate choice and then you have to jump out to the provider’s own website to complete the transaction.

What I mean by the new component-based bank is that they will find the best providers of alternative finance and offer these services through their own portfolio of access. A one-time sign-on to get access to choice all in one window. That’s what Fidor are offering and, through the deal between Metro and Zopa, it’s another step in the right direction.

Meanwhile, a rock to throw.

I was pretty surprised to read these two headlines side-by-side the other day:

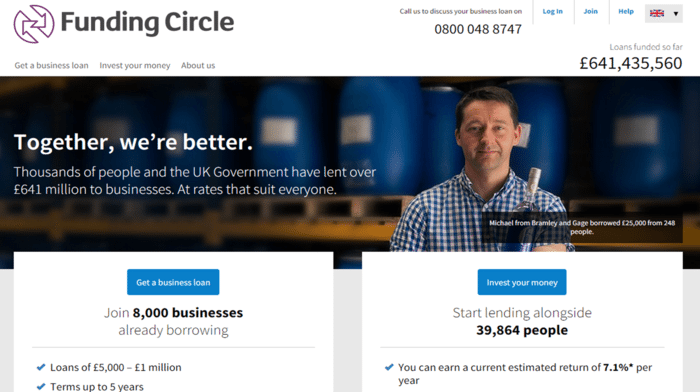

The reason I was surprised is that SMEs (Small to Medium Enterprises) are being commonly rejected for credit by banks, because they don’t meet their risk criteria. They are too small, too young, too untested, too unproven, too risky to lend to. So banks are recommending they go to Funding Circle and similar alternative finance houses. These alternative finance houses (AFH’s) opened a lifeline for businesses in the UK in the last year. For example, here’s Funding Circle’s homepage today:

And 13 months ago (yes, this was 20 April 2014):

Note the statistics: £225 million of lending enabled by Funding Circle a year ago climbing to £625 million today. A tripling in enabled funding in just over a year.

Meanwhile, the number of businesses borrowing through Funding Circle has almost doubled in that time, as has the awareness of this alternative financing marketplace. A lot of the funding of Lending Club comes from the UK Government, and it’s interesting to note that almost 98% of P2P Lending funds in the USA come from institutional investors.

So you have two key things happening here. First, the large banks are turning small businesses away to AFHs whilst de-risking their own portfolios by funding the AFHs. So the AFH becomes the risk manager.

That’s all well and good, but then take the other headline: SMEs stung by £425 million in hidden fees. This is where the Christensen disruptive innovation does start to hit as the AFH market looks like nothing today but, when I attended an Alternative Financing conference the other day, they didn’t call it alternative finance (which was a bit strange, as that was the name of the conference). They called it narrow banking. Narrow banking takes a part of the bank – a component – and squeezes that component to make it as efficient as can be for the process of its usage.

Here, in lending, it is a narrow bank focus on SME and consumer credit. A Funding Circle or Zopa squeeze the process of getting funds to those who need them to the max. And their customers love it. 77% of Funding Circle users say that after their first loan, they would return to Funding Circle first next time, rather than a bank.

So, on the one hand, banks are de-risking their credit portfolios by both funding narrow banks and encouraging their higher risk customers to use them. On the other, they are stinging their higher risk customers – small business customers – with higher hidden fees. And, on the third hand (yes, doing well here with my artificial limbs business), their customers now love their narrow bank and would not return to their old bank in the future.

That’s a broken model if you ask me. Broke for the bank that is, unless it really does not want any SME or consumer credit market operations in the future.

What banks should be doing is the Metro, Fidor and Caja Navarra approach of integrating the narrow bank offers into their customer aggregated experience. Instead, what RBS and Santander who partner with Funding Circle appear to be doing is saying that we would rather offload you to the narrow bank, than keep you with our bank.

That may be just my misperception, but it’s one that sits uncomfortably if true.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...