This is my fifth posting about why banking will be free (Parts One, Two,Three and Four).

I keep talking about this as it's clarifying my own thinking, and I'm intrigued to see if anyone wants to come up with an alternative.

This posting comes around because I was thinking about Banking on the Network and whether banks really will give away banking for free. So here’s how the pricing and economics of Banking as a Service (BaaS - SaaS for banks) works.

The bank recognises that most activities outside direct servicing of the customer is commoditised. A commodity is worth nothing, and so all processing and technology is priced at near zero because they become freely available networked widgets (as discussed last time).

Commodity processing being made freely available is a radical departure from bank histories which is why this will be a culture shock for many bankers … and yet, the pricing and economics is relatively obvious.

Let’s start with the cost of building BaaS.

The cost can be however much you want it to be. In HSBC’s case, the cost of building their global internet service is around $250 million … but that’s cheap enough considering that they were building a global bespoke service.

For HSBC that means they can launch a completely customised internet

banking service in any country, by just ticking the boxes you want in

that service and it's up and running. No additional development or

cost.

But for most, it's not $250 million developments, it's a few thousand dollars to deploy a piece of functionality.

Y’see the key point is that, whatever the cost is, once it’s built - it’s built.

That’s it.

You have sunk the cost and built the widget.

Now, the critical point is not to protect the widget but to get everyone to use it.

What’s the point of investing in a developments today if you can’t get volume?

And that’s the point of BaaS: once you’ve built your widget, crank up the volume and volume increases fast these days.

That’s how Chi-X, the pan-European equities trading facility, could take more than 10% of many traditional European exchanges equities trading ... within a year.

And, having built the system, it is why Chi-x, Turquoise and NASDAQ OMX and co are after volume.

It is why Zopa, SmartyPig and PayPal are leveraging volume.

And that's what any bank building components of applications should be thinking about today.

Volume.

Because additional volume adds zero cost and purely feeds return on investment.

Think of it like making movies. Once the movie is made, you’ve spent all the budget. Now, the point is to get bums on seats and market the hell out of it.

And that’s how banking widgets in BaaS should be considered.

Market the hell out of your widget, crank up the volume and focus upon the service delivery – the human interfaces – as your critical value-add differentiation. Your value-add is how you package the widgets and present them, not the widgets themselves.

That’s why Citigroup have been marketing the hell out of their FX and other services for the last two years. They want volume on their widget, and Citi are one of the few banks who have been white labelling their systems to other banks. They get some of the BaaS components.

The idea is really illustrated by telecoms folks who get networks. For example, I once worked for NCR when they were owned by AT&T. I always remember the AT&T guys talking about “minutes on the network, it’s all about minutes on the network”, and that’s the key.

Once you’ve built the infrastructure, it’s all about getting volume because it costs you no more to process a billion calls than it does to process one.

Which brings us back to the economics of banking in the future, under the BaaS model and the culture shock this creates.

I was recently with a head of payments at one bank for example, who said: "our technology guys asked me the other day why we charge more for a $50 million payment than we do for a $5 payment, when the infrastructure costs to process are the same? Are they mad?"

No sir. They are asking an obvious question at the heart of the change that needs to be made to banking cultures as they realise the change that technology now delivers.

This payments guy was from that old school of banking that are the ones now waking up to the new world realities.

Thirty years ago, when many senior bankers were starting out in their banks, they were told that technology was expensive, inflexible and must be used forever, or at least until the systems peg it anyway.

That’s why every project was massive, time consuming and demanded huge cost.

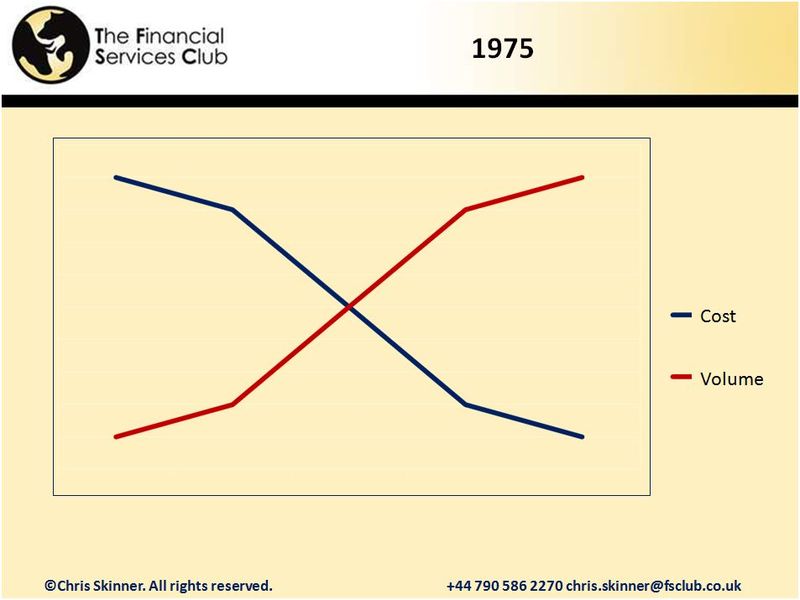

When SWIFT, MasterCard, Visa and the key networks for transaction processing were built, for example, they had to be built by an industry consortium. No individual bank could afford such a huge project or cost. That is why these were cooperative groups back in the 1970’s across all banks, even though MasterCard and Visa are now proprietary firms. Nevertheless, the MasterCard and Visa IPO’s are only recent and recognise the economics of BaaS.

For example, back in 1975, the bank technology economic model looked something like this (double-click the image to make it bigger):

Massive cost that slowly over time could be recouped through usage. Cost was depreciated slowly, and could only be covered by high prices and margins. Hence, banks, SWIFT and the card companies all worked hard to create the infrastructure, and cover the costs of that infrastructure through high transaction processing and interchange fees.

That was back then.

This model had changed a little by 2000.

What was happening in 2000, was that the post-Year 2000 hullaballoo was over. Many systems had been renovated and rationalised. And the costs of building new systems had reduced somewhat thanks to HTML (an internet language) and component/object-based modelling.

Therefore, banks found the time and cost of building new systems had been fundamentally reduced … but the costs for usage and pricing did nto come down as fast.

After all, if you’ve got a good thing, hold on to it! So the pricing and fee rates did not change dramatically, although we did see SWIFT’s model changing.

For example, the then CEO of SWIFT, Leonard Schrank, was interviewed in 2003, and made a few statements about SWIFTNet was well underway using IP-based messaging, costs for a typical SWIFT message had come down 70% in the last decade, whilst volume had increased four-fold to 8 million messages per day.

This shows the new economic model in play:

What we were seeing a decade ago is the cost to build was coming down, and volume was rising faster than before, thanks to ease of communication and connection.

SWIFT gave those savings back to their banking members, because they are bank-owned. However, banks have not yet passed all these cost reductions on to their clients but, thanks to today's competitive forces, they will.

Today competitive forces recognise how the network has changed these pricing models even further:

Today, the cost to build should become virtually irrelevant if you are using the right tools but, once built, the volume can be cranked up really fast, thanks to openness, standards, ease of networking and communicating.

You see, the bottom line is that the economics of banking has fundamentally changed. This is because banking is based upon technology, and the economics of technology has fundamentally changed.

New economics of banking: technology and systems, processing and functionality are virtually free; anything that is commodity activity should be brought in as a service and all pricing is for value-add, not commodities.

Today, it is a no-brainer to build new functionality, or even micro-functionality, and then deploy it openly, transparently and easily across the network.

That’s why banking will be near free.

It will be free because banks can build micro-functionality, widgets, and then make money out of volume.

If I can get a thousand banks to serve a million companies processing a billion transactions through my banking widget of commoditised functionality, then I make money. And that process is far better than one bank working with a hundred firms to transact a thousand times through my very expensive and out-of-date legacy infrastructure.

The latter is the old way.

Banking on the network is the new and better way.

And how do banks make money in this new world?

By being the lowest cost integrator and offerer of the best white labelled banking widgets, and then charging me for advice and superior services to those commodity services offered by others.

This final part if where the culture shock will really hit.

In a world where every bank is offering transactions and processing for nothing, how can you make me feel you’re so worthy as to be worth a fee?

The answer to that one is to focus upon the customer experience.

The customer experience, service, dialogue and advice will become the critical differentiation and profit point.

Whoa … now that’s going to be tough isn’t it?

Yep.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...