I spent a bit of time today thinking about trust in banking, a subject I’ve blogged about lots before.

One thing we know is that times have changed. How have they changed?

Well, have a look at this advert from 1991 for NatWest:

She’s a mortgage adviser for NatWest in 1991: “it’s my job to make sure they get the right mortgage, which means one they can afford” ... not a five-times salary self-cert then?

The advert finishes with the line that NatWest has mortgage advisors in every high street branch.

Now, move on fifteen years, and here is a more recent NatWest advert:

This is taking the mickey out of naff sales folks from another bank, and saying how good NatWest’s mortgage offer is. The focus moving away from finding the right mortgage and buying a house, to getting people to move mortgages and switch providers.

Now we get to NatWest’s UK adverts today:

The focus is to say: "we’re being really helpful because every penny counts".

It’s all about being open and honest and is part of NatWest’s Money Sense programme.

NatWest stress that this a programme designed for customers, with 1,000 advisors in branches who are there to give good advice, not to sell.

Sounds like a bit of a return to 1991, the last time Britain went through a crisis of finance and housing, with many people facing negative equity.

In fact, the message is the same: “we have advisors in every branch who can give you good, honest advice”.

It sounds great in principle but, in practice, something has fundamentally changed.

The confidence has gone. The trust is blemished. The bank’s brand is not the same.

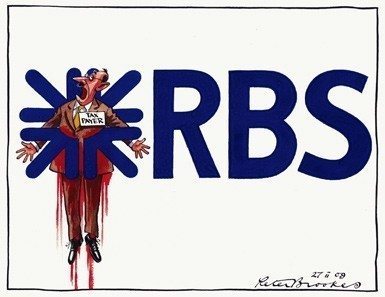

Wrapped up in the folds of the Royal Bank of Scotland and Sir Fred Goodwin daily headlines, the idea of giving good money sense advice is a bit laughable, especially when national newspapers such as the Times have cartoon half-pages such as this:

Source: Peter Brookes, The Times

This is not to say that NatWest shouldn't advertise but, as I will discuss later, they should stop spending on advertising in traditional media only and start leveraging new media.

Similary, HBOS should do the same.

HBOS has changed from its old ads declaring the wondrous world of cash machines:

To the frivolous Howard:

To the idea that you now have to reward customers to stay with you:

Does all this work?

Not really, as customers are more aware of their finances than ever and do not trust institutions that have bad headlines, bad rates or bad vibes.

That’s why folks are churning their money around, looking as far as they can for a flight to safety.

For example, I’ve already said a few times that some of the less flashy banks are doing quite well, and here’s what you see these days in the windows of mutual institutions such as the Nationwide Building Society:

For those overseas, Nationwide is not some itsy-bitsy credit union but the world’s largest building society, with 15 million members and assets of around £200 billion ($290 billion).

Nationwide do advertise, but their focus is much more around being lovable, nice and working in the customer's interests because you are a member of the Nationwide, not a customer.

And all of this is focused around branch-based banking debates.

In branches, the idea of money sense and rewards programs for staying with the bank probably seem great in the marketing corridors of head offices but, in the high road, far more convincing is the human experience of staff you trust and like, and brands you see as being trusted and liked.

Result?

Nationwide’ s new account openings have risen massively in the last year. For example, last December the Society released this press release: "Savers put their trust in Nationwide", with this quote from Nationwide’s savings director, Matthew Carter:

“Following the collapse of the Icelandic banks, Bradford and Bingley and Northern Rock and the proposed takeover of HBOS by Lloyds TSB, we have seen consumers move their savings to Nationwide as they look for a safe home for their savings. In the first half of this financial year we took £2.6 billion in net receipts giving us a 34% market share. Indeed, the entire building society sector has seen an increase in deposits being made as consumers reacquaint themselves with the benefits of being with a mutual.”

Banks with branches fighting for trust and confidence could learn something from the consumer championing, member-based interest approaches of the Building Society sector as a whole, not just the Nationwide.

Meanwhile, the Building Society sector festers as they are paying the price of the banks’ frivolous lending policies through the Financial Services Compensation Scheme (FSCS). But that's an aside.

The real point is that those who want to be able to touch their financier’s bricks and mortar may well find that the prudent and quiet thrifts gain a ‘trusted’ position over those who feature in the headlines every day as being the creators of this crisis.

So what should the banks with damaged brands do?

Stop advertising in mainstream media.

Funnily enough, Nielsen came out with some analysis of this area this week, and the headline was: "Banks should advertise more to regain consumer confidence".

The Financial Brand picks through the meat of this news though and, like me, conclude that banks should stop advertising on TV if their brand is damaged.

So what should they do?

Focus upon leveraging remote relationships through new media.

The fact is that UK banks are mainly fighting a branch-based battle and yet totally ignoring online and remote channels. UK banks' ideas of marketing online are, to be honest, pathetic.

Oh, a banner ad here, a link placement there.

Great.

Doesn't work though.

You look at the NatWest Money Sense website and the focus is advisory, but its still very customer meeting advisor in branch oriented. Or that's how it looks to me.

Where are NatWest’s online or viral campaigns? Where's their blog?

Where's HBOS, Lloyds, Barclays or Nationwide blogs for that matter?

They don't exist or, if they do, then they're very well hidden as I can't find them and I'm looking.

Google these company names and the word "blog", and nothing official comes back.

The fact is that the only UK banks I’ve noticed doing anything with Facebook, MySpace, Twitter or new media is the Co-operative Bank, who created a few nice green pages on MySpace two years ago (note this attempt to network has now been deleted); Barclaycard, whose advert for contactless gained great viral viewing; and Lloyds TSB, whose irritating theme tune made the charts.

Mind you, rather than their annoying advert tune, you are far more likely to find a YouTube customer-generated advert such as “I fought the Lloyds and the Lloyds lost” instead of a bank generated ad, when looking for some form of online presence.

So here’s the rub.

Banks today are stuck in branches fighting for customer confidence through traditional marketing media where they position themselves as trusted.

Meanwhile, customers are searching online for advice and support through social networks and communities of friends, where the banks don’t even exist.

UK banks are doing nothing to reach out to customers online and gain their confidence and trust and yet, as I've said so often, this is the best place to build it.

After all, you can't hide anything anymore (this link is worth reading as it puts context to this post, and makes clear how online transparency changes the dynamics of our industry).

In the UK, there must be something wrong here … and there is.

The fact is that banks should be creating transparency and communicating with customers through mobile and online channels in an honest and open exchange. This is a huge opportunity, not a threat.

I’ve blogged about this so much before, and would cite this series on the subject rather than writing it all again:

Banks ignore social media at their peril

Social networks don't need banks, they need friends

Social finance is right here, right now

Social money – what’s all that about?

Mobile social money, the final frontier?

Plus the discussion, as mentioned, that you can't hide anything anymore.

The fact is that the UK banks have lost the plot when it comes to marketing and customer relationships.

Please get it back and start to focus upon how to reach out to customers through social media and social networking, as well as other remote channels, to rebuild customer confidence.

Meanwhile, if you want to know how to spot a leading bank in the new world of remote finance, look at the ones who get onto Twitter first:

Wachovia

First Twitter post, August 18th 2008.

2,403 followers

272 updates

Bank of America

25 million internet banking customers, 2 million mobile banking customers

First Twitter post, January 7th 2009.

1,578 followers

635 updates

ING Direct

First Twitter post, February 6th 2009.

670 followers

79 updates

Wells Fargo

First Twitter post, yesterday.

193 followers

43 updates

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...