I've kept away from commenting too much about Sir Fred Goodwin's pension furore that has been the major media story in the UK for the past week because:

(a) it's old news;

(b) it's just a distraction from the real news;

(c) if it was my pension, I'd keep it;

(d) Fred's got the pension, legally, and he's keeping it; and

(e) there's nothing the government can do about it.

End of day, if the government wants to change the law because they messed up over his pension promises, then they will find the same thing happens upon their retirement:

"Although the Right Honourable Gordon Brown may be entitled to a pension on the state of £225,000 index-linked, we are only going to give him £5:50 a month on the basis that he screwed up the economy."

There's the rub: you ain't gonna change a darned thing that might end up cutting yer nose off to spite yer face, are ye?

Anyways, I am mentioning it here because there were those two letters exchanged between Sir Fred and Lord Paul Myners, the City Minister, last week.

On 26th February, Sir Fred wrote:

Dear Lord Myners

You telephoned me yesterday and asked to consider voluntarily taking a material reduction in pension entitlement as a ‘gesture’ to acknowledge the level of Government support being made available to RBS. You highlighted that the absence of such a gesture would give rise to significant adverse media comment.

I outlined to you my view of the matter, but as I had not been expecting your call, and as you expressly requested me to do so, I undertook to reflect on the matter again. You emphasised that I would need to provide you with an answer ahead of the publication of the Group’s annual report and financial statements sometime next week.

It came therefore as something of a surprise to find that both details of forthcoming 2008 financial statement disclosures relating to my pension and the substance of our telephone conversation had been placed in the public domain a few hours after we spoke.

In the circumstances, I feel that an earlier response to your request is necessary, and the purpose of this letter is to provide that.

Whilst my pension is the current focus on attention, there were a number of other aspects of my departure from RBS which need to be considered at the same time, particularly in the context of ‘gestures’ and appropriate behaviour.

My contract of employment provided for a 12-month notice period, which I voluntarily waived in October of last year. This amount of a loss of one year’s salary and I discussed this with you at the time, when you indicated it was both an appropriate and sufficient recognition of the circumstances.

Subsequent to this, you approached the Chairman of the Group remuneration committee to suggest that I should waive certain share related awards which would otherwise have vested upon my leaving the Group. Whilst difficult to value with precision, these had a value equivalent to about three months’ salary at that time. During these discussions, I am told that the topic of my pension was specifically raised with you by both the Chairman of the Group remuneration committee, and the Group Chairman, and you indicated that you were aware of entitlement and that no further ‘gestures’ would be required. On this basis, I agreed to waive my entitlement to the share related awards, and proceeded to subscribe for my full allocation of shares in the ensuring share issue.

Like you, I believed that these gestures were appropriate in the circumstances, and sufficient, and revisiting the position today, I believe that they remain so. I accept responsibility for that which I was responsible for, and recognise that my actions must be consistent with this. I believe that they have been, and to voluntarily accept a reduction in pension entitlement which has been built up over many years and in other employments in addition to RBS, is not warranted. It is important to recognise that my pension arrangements have not fundamentally altered since I joined the Group in 1998. Whilst the quantum of the ‘pension pot’ figure has increased, this is principally as a result of the assumption used last year about retiring at age 60 no longer being appropriate. The amount which I am due to receive as a pension continues to be calculated in a manner consistent with prior years.

Whilst I suspect that you will not now agree with it, I hope that you can understand my rationale for declining your request to voluntarily reduce my pension entitlement.

In conclusion, since our private conversation yesterday is now in the public domain, I have no objection to the complete content of this letter being made public.

Yours Sincerely

Sir Fred Goodwin

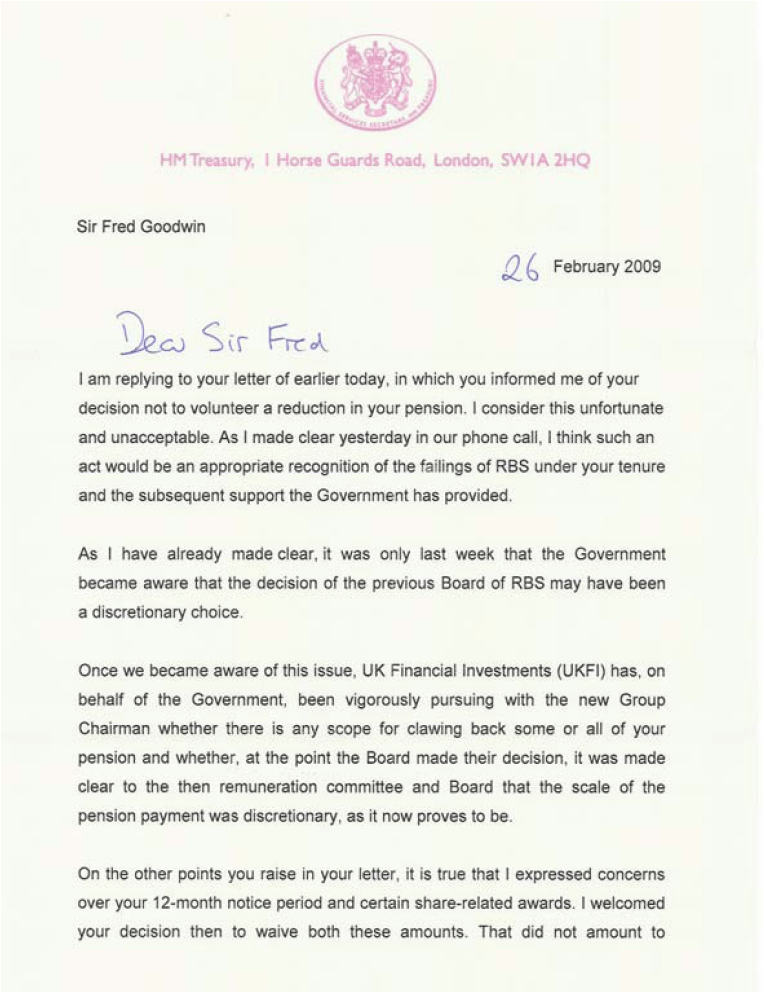

Lord Myners replied (doubleclick to see in large screen):

All I can say is good luck to the both of them, and I hope Fred enjoys his winter holiday in the sun for the new few months.

And thanks to PJ for tipping the nod to Lord Myners' letter.

More info:

City split over damage done to Lord Myners by Sir Fred Goodwin's pension (Times)

Grudge between Lord Myners and Sir Fred Goodwin born at board table (Times)

Paul Myners the man who agreed Sir Fred Goodwin's pension (Telegraph)

Sir Fred Goodwin: the RBS chief who bet the bank and lost (Telegraph)

Fred Goodwin: from Hero to Zero (Chris Skinner on Bankstocks)

And a few spikes:

Fred Goodwin: Forbes Global Businesman of the Year, 2002 (Forbes)

Fred Goodwin Knighted, 2004 (The Scotsman)

Sir Fred Goodwin voted Business Leader of the Year, 2004 (Financial News)

Sir Fred Goodwin: Most Powerful Person in Scotland, 2006 (The Scotsman)

Sir Fred Goodwin: Orange Business Leader of the Year finalist, 2006 (National Business Awards)

Sir Fred Goodwin: Business Communicator of the Year finalist, 2007 (Public Relations Consultants Association)

Sir Fred Goodwin: Awarded Honorary Fellowship of the London Business School, July 2008 (Press Release)

... blah, blah, blah ...

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...