Last Thursday was one of those days where you wake up knowing it’s going to be a good one and you go to bed realising that it was … for some that is, but not for everyone.

In my case, I was up with the birds to get into the City and chair a conference all about trading technologies, from smart order routing through low latency equities exchanges and beyond.

On the way into the conference I discovered that for my good friends Peter Randall might not be having his best day as the headlines held the news that he had left Chi-X. This shocked me as Peter was joining our Financial Services Club’s panel on low latency that very evening.

I rang Peter and obviously gave him my best wishes and that I totally understood that he would not be able to join us that evening and wished him well. Then, in the spirit of the City, I immediately grabbed Hirander Misra, COO for Chi-X, and asked if he would take Peter’s place that evening which he did.

Joining Hirander were Todd Golub, COO of NASDAQ OMX and Yann L’Hullier, CIO of Turquoise.**

Terry Quigley of Colt Telecom and Chris Pickles of BT both joined us as well. Terry and Chris are key advocates and deliverers of low latency networking.

The results were also fascinating and, to an extent, staggering so I'm going to provide here a collection of clips and slides from the evening. The video clips are variable in quality due to the various converters used, and Slideshare isn't accessible for everyone, but here's a complete multimedia view of the evening.

To start with, the slides:

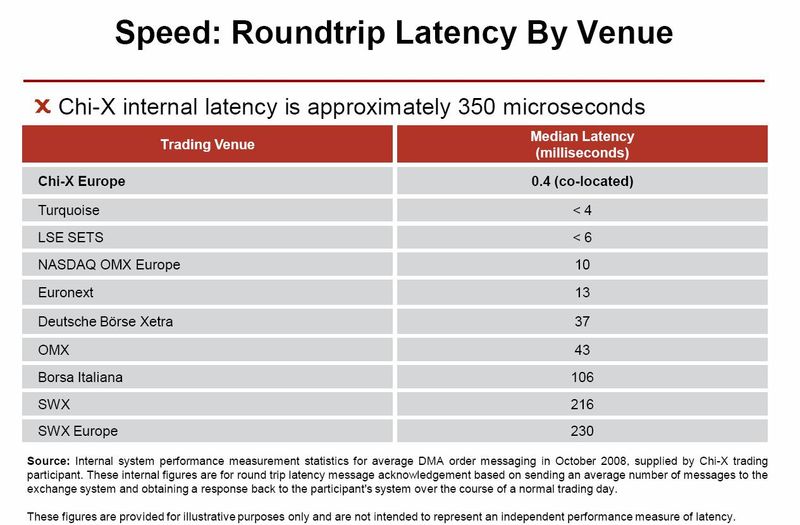

As you can see from Slide 6, which I'm reproducing here in case Slideshare is not available (doubleclick to see this slide in full screen):

This is a high stakes battle where speed is key.

Here’s Hirander Misra explaining how it works:

Now Chi-X was purposefully stoking up the argument by saying that they could provide a roundtrip order execution in less than 400 microseconds. There are 1,000 microseconds in every millisecond, and a 1,000 milliseconds in every second so that’s fast.

To put it in context, it takes around 400 milliseconds to blink, so Chi-X can process 1,000 back-to-back orders for every time you blink!

1,000 orders every time you blink!

I had to write that twice, as it’s quite astounding to imagine.

That speed may be contingent upon proximity and FIX connections, but even so … 1,000 orders every time you blink!

That means that if it takes you around seven seconds to read this sentence, Chi-X will have processed around 20,000 back-to-back orders, and yet they can process 150,000 messages per second so that's more like 3 million messages processed in those seven seconds.

Wow!

So Hirander claimed that Chi-X has the fastest trading system in Europe and scalability to 150,000 messages per second, implying the others did not.

The others responded, with Todd saying they could match that volume processing:

and Yann making it clear that it’s not just about messages but capability:

We then explored more around latency in depth, and how latency is critical if you are smart order routing through the network to these exchanges.

The importance of low latency cannot be stressed enough in the trading room, as illustrated by Slide 17 which states that: “a 1-millisecond

advantage in trading applications can be worth $100 million a year to a

major brokerage firm.”

$100 million a year?

This is because if you place an order and it misses being filled, it misses being filled.

Even if it misses being filled by 1,000,000th of a second, it misses being filled. In other words, you are dead meat.

That’s the power of latency.

Now, I had a dinner last year with a bunch of folks talking about latency from buy and sell side firms, and a few said that latency didn’t matter because their internal systems were so messed up that they took minutes to process rather than microseconds.

That’s not true though.

If your internal systems are messed up, then sure you’re not going to be as effective as an algo trading, smart order routing, co-located broker-dealer with a snazzy execution management system … but once your orders leave your systems, then they can travel at the same speeds and you should focus on being as fast as the best or, at least, the rest.

This is why some folks are moving their data centres around the globe to maximise latency. I even heard of one bank that found it took sixty milliseconds longer to route orders via New York from London to Tokyo than via Moscow, so they moved their router network hubs to Moscow as a result.

Terry Quigley elaborated:

And Chris Pickles also made it clear that proximity services – where traders place their order management systems together to reduce speed of processing – alongside co-location services – where traders place their servers into the exchange to minimise latency – impacted where organisations focused their operations:

We then had a lot of dialogue about the differences and differentiation points between Chi-X, Turquoise and NASDAQ OMX, with a few digs here and there. For example, several folks have questioned whether Turquoise can be truly competitive if they are using off-the-shelf systems such as Cinnober’s Tradexpress, which has also been selected by the Nordic MTF Burgundy, although they will be on a later release.

Yann L’Hullier retorted that they have changed Cinnober to reflect the London markets operations of Turquoise and processing in the top European stocks so it’s not ‘vanilla’ software.

Equally, there were discussions about measuring and comparing apples with apples, as usual, with leased line, networked or co-located and proximity services all offering different capabilities for processing, as well as differences in FIX FAST and FIX 4.2 and other FIX connections. So it’s not all simplicity itself.

The rest of the meeting covered long dialogues about Baikal (who were in the audience) and Dark Pools, market data and the outage of the LSE last year, and more.

Anyways, as you can see, we’ve started recording Club meetings in hi-definition. The embedded clips in this blog entry are a little taster, although the quality is less than the original. Must be my lack of knolwedge of how to edit and use YouTube etc.

Suffice to say that the full meeting recording is available for Club members and online subscribers only and, if you would like to see the full recording of the meeting which runs to over an hour, then let me know.

Equally, if you’re not a member or subscriber but would like details, then email me.

** Interestingly, Hirander, Todd and Yann were also on a panel discussion that morning which I chaired by coincidence, joined by Paul O’Donnell, COO of BATS Trading Europe, and Edwin Marcial, SVP & CTO for The Intercontinental Exchange (ICE). This made the day a really good one from a knowledge gathering around MTFs.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...