There are loads of discussions about mobile financial services right now, not least at the Financial Services Club.

For example, I recently received this presentation from Len Pienaar, CEO for First National Bank’s (FNB) mobile solutions in South Africa:

Add this to the many other mobile financial stories and case studies reported already:

- ABSA (Mobile Payments)

- BBVA (Social Finance/Web 2.0 and Mobile Finance)

- Jibun Bank (Mobile Finance)

- M-PESA (Mobile Payments)

- MoBank (Mobile Finance)

- UMPay (Mobile Payments)

and you can soon see that this space is hot.

Now I can add a bunch more because we recently held three meetings at the FSClub: the first in Austria in April; then in London in May; and finally in Dublin in June; and all about mobile financial services.

The common theme amongst all three meetings is that mobile banking and financial services is BIG news, with speakers including Volksbank, Royal Bank of Scotland, Monitise, MoBank, Cap Gemini, S1, IND and Edgar Dunn.

So here’s a rapid summary of what folks said.

First, Martin-Hannes Giesswein, Head of Retail for Nokia Alps & Southeast Europe, made these statements about key mobile trends:

The core of Nokia’s view: kids are being introduced to mobile young and, with most of the world now able to access mobiles, you would be silly to ignore this space.

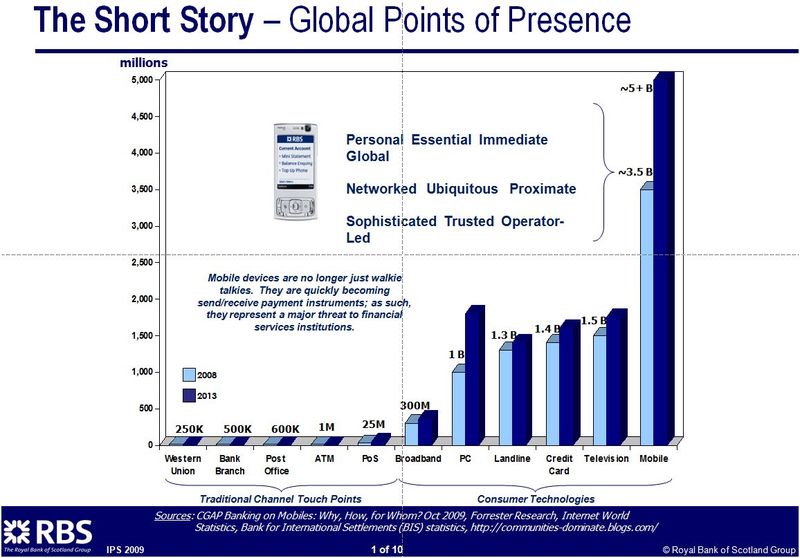

This is corroborated by Roy Vella who heads up mobile for Royal Bank of Scotland who presented this slide (it’s one of his favourites and worth a doubleclick to see the full slide):

What this shows is that half the planet has access to mobiles. A point that is stressed by Samee Zafar, Director with Edgar Dunn & Co:

There are more mobiles being bought per second than babies being born!

József Nyíri, Chief Technology Officer with IND Group, makes the point that mobile is this major channel because it is easier than using a PC:

Whilst Richard Johnson, Chief Strategy Officer with Monitise, stresses that it is a critical channel for getting rid of nuisance calls, such as those that are just balance checking:

All of these firms, banks, infrastructure and solutions providers believe the same thing: if you’re not into mobile yet, you’re going to be dead meat.

This was truly illustrated by Steve Townend, Chief Executive Officer with MoBank, who discussed what happened when they started a pre-release programme for their banking service on the iPhone:

Steve's point is that the MoBank iPhone app was launched in Beta mode and, as a result of being listed as a half-decent financial app on the Apple App download listings, it shot up from no downloads to 3,000 in a day.

How do you scale to handle that sudden viral impact of being noticed?

Cloud computing I guess, as this was similar to the issues Animoto experienced last year.

Animoto was a little known service that makes it really easy for people to create videos with their own photos or their own music. Last year, they became a classic case study in cloud computing because they suddenly went from zero to hero over one weekend.

The Amazon Web Services Blog summarised what happened well:

“Animoto co-founder and CEO Brad Jefferson stopped by Amazon HQ for a quick visit on Thursday. Earlier in the week we had seen their EC2 (Amazon’s server farm for cloud computing ) usage grow substantially and I was interested in learning more. Brad explained that they had introduced the Animoto Videos Facebook application about a month earlier and that it had done pretty well, with about 25,000 users signing up over the course of the month, with steady, linear growth.

“The reaction from the Facebook community was positive, so the folks at Animoto decided to step it up a notch. They noticed that a significant portion of users who installed the app never made their first Animoto video — yet the application (as they themselves admit) relies heavily on the 'wow' factor of seeing your first Animoto video and wanting to share it with your friends.

“On Monday the team made a subtle but important change to their application: they auto-created a user's first Animoto video.

“That did the trick!

“They had 25,000 members on Monday, 50,000 on Tuesday, and 250,000 on Thursday. Their EC2 (server) usage grew as well. For the last month or so they had been using between 50 and 100 instances (this is the equivalent of the need to access the power of 50 to 100 servers). On Tuesday their usage peaked at around 400, Wednesday it was 900, and then 3400 instances as of Friday morning.

“Here's a chart:

“We are really happy to see Animoto succeed and to be able to help them to scale up their user base and their application so quickly. I'm fairly certain that it would be difficult for them to get their hands on nearly 3500 compute nodes so quickly in any other way.”

As Jeff Bezos, CEO of Amazon puts it: “You can see they’ve gone from 50 instances of EC2 usage up to 3,500 instances of EC2 usage. It’s completely impractical in your own data center over the course of three days to scale from 50 servers to 3,500 servers. Don’t try this at home.”

In summary, I know this blog entry combines a lot of different points, but they are all related:

- mobile technologies are transforming banking services globally;

- from simple text payments to full banking services, there are many examples of this transformation;

- the challenge is how to keep up with the speed of innovation and the speed of viral change; and

- when a mention on iPhone apps shifts MoBank from 50 downloads a day to 3,000, how do you keep up?

- similarly, viral networking through other social media can result in a similar upclick in hours (think of Susan Boyle going from nothing to 200 million video views in only a month!); and so

- cloud computing and the Animoto – Amazon story maybe shows the way, where you can upscale by buying server space on demand.

Our world is one where mobile social networking enables viral financial apps to transform an unknown bank into a dominant player in hours.

The world is changing … are you keeping up?

Full sound and, in some cases, video recordings of the Club meetings are available to Club members, including remote members.

The Finanser is sponsored by Vocalink

For details of sponsorship email us.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...