Interesting article on the guide to all things Europe today, Euractiv, about the Payment Services Directive.

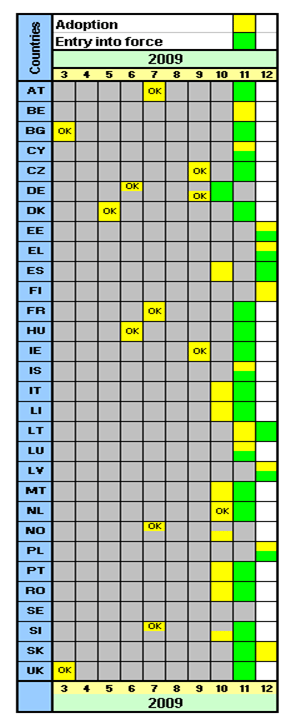

The Directive “has been transposed in all but 11 of the 31 EU/EEA countries”.

Hmmm ... that would be Cyprus, Estonia, Italy and Latvia (Jan); Norway (Feb); Belgium, Greece, Spain, Finland, Malta and Poland (Mar); whilst Sweden is last (Apr).

Note: the above are the official charts of the European Commission. Is someone pulling the wool?

“Observers agree that it favours banks and card companies over the merchants, retailers and consumers who will be using the scheme.”

Hmmm ... would the banks agree? The banks that have spent eight years pulling SEPA together? The banks that have spent billions on change and lost billions of margin? The banks that have been arguing that there is no benefit to merchants, retailers and consumers being communicated by the Commission or public authorities?

“The directive may lead to more fragmentation.”

That’s the point isn’t it?

By introducing new payments institutions, it creates more competition which leads to lower prices which leads to better markets, is the contention of the legislators. This was the same view with the other Directive, the Markets in Financial Instruments Directive, that led to market fragmentation for investing with the rise of Chi-X, BATS and many dark pool investment vehicles, where things are traded outside the line of sight of the public market.

Markets do fragment thanks to these Directives. Over time, they then consolidate. That is why Chi-X stands out as a clear leader in the post-MiFID trading world and, over time, the same will happen in the post-PSD payments world.

So fragmentation isn’t necessarily a long-term issue, but a short-term concern.

“The PSD's weaknesses lie in its opt-outs”.

Absolutely. Checkout our research if you want to know what they mean as derogations and opt-outs have created a truly uneven playing field for payments.

“Card companies argue that the EU's new rules do not address the issue of catching fraudulent transactions.”

In the words of an old Tina Turner song: “what’s fraud got to do with it?”

The card companies are right by the way. The PSD is purely concerned about moving towards a level playing field for payments in terms of the legal structures of cross-border transactions. The focus was primarily around direct debit and credit transfer operations, as this is where SEPA had focused and needed support. Cards were not centre of the radar for the legislation, nor was fraud. Watch out for the PSD II in 2012 however, when these things do move to centre stage.

Postnote:

At the end of the article is the line: “SEPA is being treated as a low-priority project in Sweden and Finland because their respective ministries of finance have limited resources to roll out the scheme, according to Elemar Tertak from the European Commission.”

I think the person who wrote this mistook PSD for SEPA.

If they want to know more about SEPA then come along to our meeting tomorrow night at the Club:

"Is SEPA happening and does it matter?" a panel discussion with:

- Gilbert Lichter, CEO, EBA

- Fred Bär, Managing Director Euro Services, VocaLink

- Paul Smee, CEO, the Payments Administration

- Simon Bailey, Director, Logica

Chaired by Bob Lyddon, Managing Director, IBOS Association.

Started in 2002, in response to the Lisbon Agenda and Regulations on fees for cross-border cash withdrawals, the Single Euro Payment Area (SEPA) has been in the planning for a long time. In fact, it has been discussed for so long by so many that, for a lot of people, it’s become as dull as dishwater.

This view may be wrong though as, after seven years of gestation, SEPA Direct Debits (SDDs) were finally born in November 2009 and the Payment Services Directive (PSD), which legally supports SDDs, was transposed and implemented in most European countries.

So all is good is it not?

Or maybe it is not as, according to the survey the Financial Services Club performed during the Autumn, most nations and most banks are not supportive or implementing SEPA and the PSD correctly.

What is the truth? Is SEPA here? Even if it is, does it actually matter?

If you would like to attend, click here.

The Financial Services Club is sponsored by

For details of sponsorship email us.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...