As those who follow this blog know, I write regularly about services such as Facebook and PayPal.

This is because they are disruptive and fresh, as well as being incredibly successful.

For example, Facebook is now the world’s #1 website, bigger than Google.

Not bad for a five year old.

Meantime, PayPal is still growing fast, making over $95 a second in revenues based upon $3 billion in revenues this year. This makes them the interweb’s sixth most successful website by earnings.

Not bad for a ten year old.

But these sites are not the be-all and end-all. You have to bear in mind that they are purely popular in their language of origin: English.

As a result, there are several other search engines, social networks and P2P payment services that are succeeding out there, from China’s QQ to Russia’s Yandex.

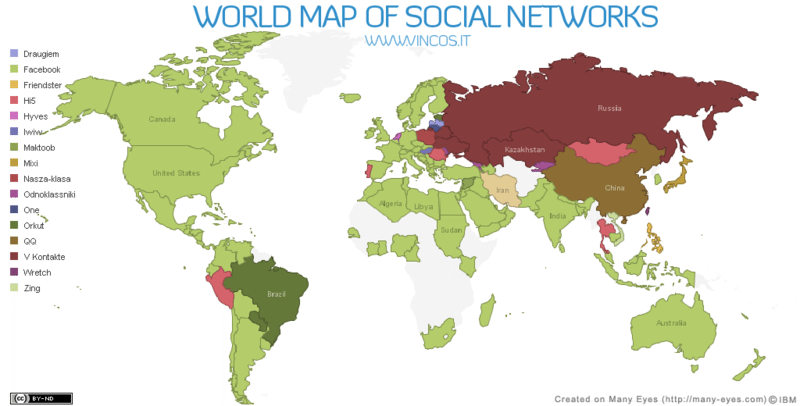

Here's a world map of social networks, taken from the blog of Vincos, Italy (doubleclick to enlarge picture):

Although Facebook is a big hit worldwide with 400 million users, it’s tiny in some countries like the Czech Republic (Lidé is the #1 social network), Hungary (iWiW), India (Google’s Orkut), Japan (Mixi), Netherlands (Hyves), Philippines (Friendster), Poland (Nasza-Klasa), Russia (vkontakte), South Korea (Cyworld), Taiwan (Wretch) ...

Similarly, PayPal is hardly recognised in some countries.

In the Netherlands, for example, the banks launched iDEAL, a set of standards to facilitate online payments.

iDEAL was created in 2005 by a range of participating banks with ABN AMRO, ASN Bank, Fortis, Friesland Bank, ING, Rabobank, SNS Bank, SNS Regio Bank and Triodos Bank on board today.

Some of the major features of iDEAL include the fact that it offers both real-time payment initiation and authorisation by both the issuing and acquiring bank, followed by irrevocable credit transfers to the merchant at the time of online purchase.

The participation of the banks along with real-time processing, has created a strong perception of iDEAL being SAFE. As a result, iDEAL has gained over 15,000 participating merchants and 5.8 million users, resulting in a total of 45 million transactions in 2009 worth over €3.4 billion (up 60% over 2008).

* maandtotalen = monthly total

In other words, iDEAL has a 40% market share of all e-payment transactions in the Netherlands, with an acceptance rate at almost 9 out of 10 online merchants (88% of all Dutch merchants) compared with only 1 in 4 for PayPal (although that’s up on 1 in 5 a year ago, thanks to the decline of AMEX in the Netherlands).

So the banks do have a PayPal service equivalent ... but, right now, only in the Netherlands, although iDEAL aims to expand across more of Europe by gearing up for SEPA Credit Transfers (SCT) and the Unify XML standards.

Meanwhile, in Russia, their version of Google Checkout has taken a place ahead of the market.

Google Checkout is actually called Yandex.Money run by Yandex, Russia’s largest search engine.

According to Liveinternet.ru, Yandex increased its share of search traffic from 56% in January 2009 to 59% in December to 62% in February 2010.

Yandex.Money claims to be the leading online payment system in Russia as a wholly owned subsidiary of Yandex. Founded in 2002, Yandex.Money has seen payment volumes grow 135% CAGR, processing 21.5 million transactions per year worth $350 million.

This may sound small, but the appeal of Yandex.Money is for the vast numbers of unbanked and underbanked Russians who want to deal online.

Yandex.Money provides over a million prepaid cards per year through 100 distributors, to be used in over 50,000 participating outlets all over Russia. They have over 200,000 participating terminals to load cash on the cards in 80 of Russia’s largest cities, and 1 in 5 customers use them as top-up wallets. Meanwhile, 61% of users pay directly from the Yandex.Money interface online.

So Russia’s online payments market has developed a slightly different way.

Meanwhile, China has an incredible story of the success of Alipay, a division of Alibaba the B2B ecommerce portal.

Alipay is China's primary payment platform thanks to being the preferred payment system for sister firms Taobao and Alibaba.com, along with over 460,000 external merchants. The result is that Alipay has a 49% market share today for all online payments in China:

Q1 2010 market share figures from iResearch

Equally, it has a larger userbase than even PayPal with over 300 million registered users as of March 2010, with five million transactions per day worth an average RMB 1.2 billion (US$176 million).

Why should this be of interest to our global banking community, and PayPal specifically?

News Headline, April 11th 2010: “Alipay, China’s largest online payment network, has announced that Alibaba Group will invest a total of RMB5 billion (US$732 million) over the next five years to upgrade the payment solution for e-commerce in China and around the world.”

Serious stuff!

Meanwhile, in a non-exhaustive list, there are many other online payment services worth a look including 2CO, AlertPay, Bill Me Later, C-gold, CashU, Dotpay, E-Gold, LiqPay, Mobile Wallet, Nochex, PayPay and Z-Payment.

So in future, when I talk about PayPal, don’t forget that we’re also talking about their national equivalents such as iDEAL, Yandex.Money and Alipay. Similarly with Facebook, don’t forget that there’s also Mixi, Hyves, Orkut and Friendster.

The implications of these services on core banking is exactly the same which is that we are seeing the creation of many disruptive, fresh and incredibly successful web services for social and P2P finance ... leading, in future, to social B2B finance.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...