After the earlier discussions of flash crashes and HFT, on to dark pools.

It was interesting that a colleague made the statement this week that all orders could be seen on US exchanges before they are filled as that may be true for some markets, but dark pools exist to ensure that orders cannot be seen before they are filled, which is why they’re so popular.

Take an investor in a particular stock, let’s say they want to buy two million shares in Apple.

Two million Apple shares is a lot, especially as the shares trade at $268 per share. The result is that you’ll move the share price if anyone sees your trade in so large a block of shares.

So you a few choices: split the block order into multiple sub orders, all of which gradually trade as little trade executions and the wider market has little knowledge of such a large order flow until the sub orders are filled; or place the order onto a dark pool where it sits until a message comes across it that can match the order’s requirements, and then it’s filled.

Either way, it creates a better market by allowing order flows of significant volumes without the markets reacting positively or negatively to your investment until it has been executed.

Now here’s the problem.

Regulators don’t like it.

They don’t like it because it’s scary. It’s dark.

They think that dark pools create bad markets because they allow dark trading with zero transparency.

Equally, it’s not fair for the traditional stock exchanges where order visibility is clear and transparent. These dark pools, because they are dark, keep things too secret.

Now, there are a number of mistakes in that logic.

First, dark pools are good for markets as they increase liquidity. They are purely executing block orders that would have been sub-divided into multiple order flows previously.

Second, they are good because they get best price execution for those trading, and allow market investors to make large order trades without punitive anti-trades occurring.

Third, they are transparent in post-trade. Post-trade reporting means that you can see dark pool trading transparently after the fact, as it should be, rather than before where the intentions are made but the action has not been taken.

However, as MiFID II is under discussion, some are resisting the march of dark pools, particularly the traditional exchanges. For example, earlier this year, the Federation of European Stock Exchanges (FESE) said that dark pools accounted for 40 percent of total EU equities trading. This was clarified afterwards as being a misquote, with the point being more that OTC trading accounts for 40 percent of European trading. Even so, the rotten tomato throw stuck to the blotting book of dark pools, with others coming out and saying that FESE’s figures are just wrong.

CESR finally stated that it was more like 2% of European trading in dark pools, a figure that seems more realistic, whilst the FSA estimated 1.25%.

Who’s right and who’s wrong?

The FSA.

In June 2010, Thomson Reuters Equity Market Share Reporter (EMSR) showed that dark pool trading accounted for 1.36% of all on and off exchange trading in Europe across 50 trade venues.

The value was €21.9 billion of trading, against a total value of €1.62 trillion across all exchanges. That compares with just 0.85% of trading on dark pools in January 2010 (€10bn against €1.18tn) and just 0.23% in January 2009 (€2.4bn against €1.062tn).

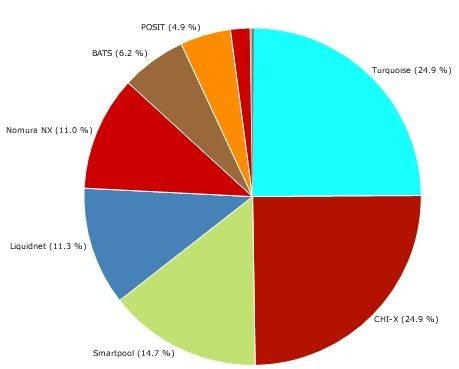

In terms of venues here are the June market share figures by Value:

Volume:

And Trade Count:

Compare the value traded on Turquoise, Chi-X and Smartpool in June with January 2010:

And January 2009:

And you can see how dynamically this market is changing.

(taken from our monthly MiFID monitor using Thomson Reuters EMSR)

This is Part Three in a Series of Posts on the Regulatory Agenda for Capital Markets:

- Part One: SEC to crackdown on HFT?

- Part Two: What was the cause of the 'flash crash'

- Part Three: Exactly what is and how big are 'dark pools'?

- Part Four: MiFID II - the post-trade agenda

- Part Five: Best Execution and Global Trading

These items also build upon a series of posts about the Deutsche Börse:

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...