One of the big topics in capital markets is intra-day liquidity and post-trade transparency.

Such discussions are far more noticeable now because the whole reason for this crisis, according to some, was the loss of trust between counterparties. That loss of trust was based upon counterparties not having enough liquidity to cover their positions. After all, if Lehmans could collapse with billions of dollars of debt – and they were AAA rated – then anyone could collapse.

We then had this dialogue around the right levels of counterparty cover and collateral required in the markets at start of day, end of day and intraday to enable effective trading.

There were discussions of whether it should be like the Russian markets, where collateral has to be pre-posted every morning to cover the day’s trading.

Or whether there was a way to just put circuit breakers on the markets, like the Eurex Clearing model discussed last week, although that liquidity control is based upon self-management.

There have been other discussions about regulatory controls of liquidity risk, such as those provided by the UK’s FSA that requested real-time reporting of liquidity positions, at an estimated cost of £2 billion in new technology spending.

Meantime, Europe announced the de Larosière reforms a year ago, and these reforms are now coming into play as the three new regulatory authorities- the European Banking Authority, the European Insurance Authority and the European Securities Authority - come into play.

And, of course, America is trying their darndest to sort out the mess of OTC Derivatives and fragmeneted trade reporting.

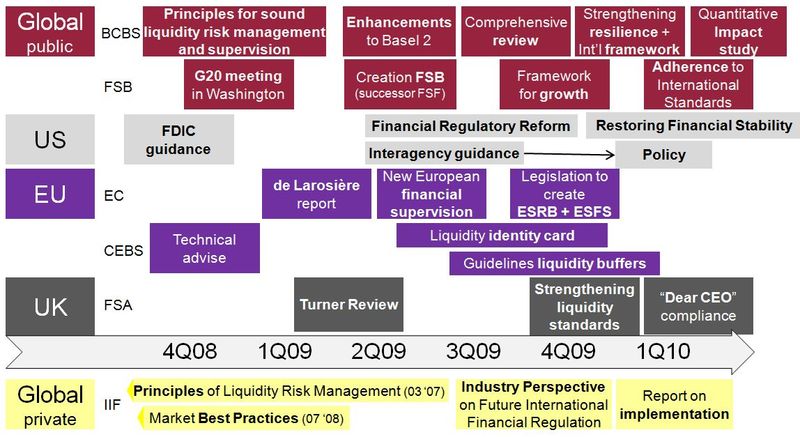

So, in summary, we have global, regional and national regulations working together and apart to try and lock down this space, as illustrated by this slide (doubleclick image to enlarge):

Stolen from Harald Keller’s (Senior Manager, Payments Markets, SWIFT) presentation – for more click here

Overall, the focus of all these regulatory changes is around liquidity risk, which brings in several other key elements including collateral management, clearing and settlement and post-trade reporting.

For example, at last week’s meeting in Germany, Robert Barnes of UBS kept using the line: “post-trade reporting is the next pre-trade”.

What he meant by this is that if you have real-time trade reporting, then that helps the markets with transparency of investment strategies and where the next trades will come from. Therefore, if you can immediately see who traded those two million Apple shares on the dark pool, then you can immediately alter your algo strategies to suit.

Bring in the algo news feeds et al and he’s right.

The trouble with this is that post-trade reporting is good if people do it, but a lot of trading operations ignore trade reporting. In fact, the only post-trade reporting market that seems efficient is London thanks to Boat. In some other markets, T+3 is the order of the day ... or even worse.

So one thing that MiFID II is likely to do is to bring in some mandatory trade reporting requirements that strengthen the moves where the first version of MiFID failed.

Another facet to MiFID II will be some form of mandatory real-time reporting of trades, and a clearing and settlement directive incorporated as part of this.

Now that’s a leap of imagination –real-time trade reporting, real-time liquidity positioning and real-time clearing and settlement.

I’ve blogged about real-time opportunities before, and do NOT think that the European Securities Authority, the European Commission or the ECB would be silly enough to mandate real-time everything, but I do think they will want to see true interoperability across all clearing systems.

The LinkUp Alliance and Code of Conduct has gone some way down this route, but the situation is still pretty fragmented as can be seen from this chart, courtesy of Robert Barnes at UBS:

Sure, this is slightly out-of-date, but things haven’t changed that much and so transparency of trades, simple and straight through clearing and real-time liquidity management are definitely order of the day for the regulatory agenda.

This is Part Four in a Series of Posts on the Regulatory Agenda for Capital Markets:

- Part One: SEC to crackdown on HFT?

- Part Two: What was the cause of the 'flash crash'

- Part Three: Exactly what is and how big are 'dark pools'?

- Part Four: MiFID II - the post-trade agenda

- Part Five: Best Execution and Global Trading

These items also build upon a series of posts about the Deutsche Börse:

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...