We had an excellent presentation from Giles Andrews, CEO of Zopa, at the Financial Services Club this week.

Giles follows on the tradition of Zopa presenting to the Club, started by their late founder Richard Duvall in 2005 and former CEO James Alexander in 2008. What intrigues me about Zopa is how their business is developing over time.

First, for those unfamiliar with the company, they are the original P2P lending provider. What this means is that they do not provide loans themselves, but they enable people who want to lend to connect with people who want to borrow in a managed risk environment. The risk is managed by using traditional credit vetting services of banks, such as Equifax and Experian, and is the reason why the service has a minimal default ratio averaging 0.7%. The ratio lowers to 0.1% for the lowest risk lending operations, which is actually a better risk model than traditional banks achieve.

Their lenders range from 20 to 88 years old – the cybergrans as Giles refers to them – and the average age is 40. Their lending ranges from £10 to £100,000, which does raise the question of how Zopa achieves full KYC and AML requirements. Giles deflected this somewhat by stating that the money coming into Zopa and going out has to come through a bank account, so the AML is through the bank rather than through Zopa.

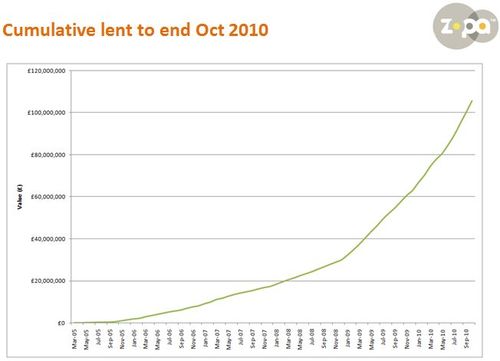

Meanwhile, through the credit crisis, Zopa has seen this phenomenal hockey stick u-curve of people flocking to their platforms, such that they just broke through the £100 million (US$160 million) barrier of loans flowing through the platform, a figure that shows a doubling year-on-year and now reflects 1% of the overall lending market in the UK.

Note: the increase in business occurred in September 2008, just as HBOS and Lloyds merged and RBS had to be bailed out.

This year alone, they expect to process £70 million ($100 million) in enabled lending – about £6 million per month ($10 million) – and hope to increase this to £140 million next year.

This success has been replicated elsewhere, with firms such as the Lending Club in the USA taking over $10 million a month through their platform.

It is also the reason why others want to get in on the act, with four new P2P lenders entering the UK market in the last three months of which one is specifically targeting the small to medium business market for loans, a market that is discussed almost daily in the media as being underserved today.

No wonder Giles confidently believes that they can garner 10% of the UK lending market by 2014 and half long-term.

Nevertheless, Giles then went on to discuss the worldwide movement of social lending and P2P loan platforms and gave a few caveats here. For example, Zopa's overseas ventures had not worked out for various reasons, most of them regulatory; Prosper had also failed, as the SEC shut them down when they were generating around $10 million a month and they’ve struggled to average more than $2 million a month ever since; there are no such systems in Africa; and the only other European success has been Smava in Germany, but they needed a banking licence from BaFIN before they could ramp up their business.

In other words, the financial protection rules of most countries has made it incredibly difficult to repeat Zopa’s UK success, even though the service they offer is not a financial one themselves. Note: Zopa does no lending themselves, they just enable those who want to lend to connect with those who want to borrow at better than high street banking rates.

Another point Giles rammed home is that they do no marketing, but that they are trusted. This trust is generated by their community, not by Zopa themselves. For example, they have an open platform for discussions that are regulated by their customers. If one customer comes out and moans about bad services, there will normally be ten others who will shoot them down if they are wrong. Amazingly, he believes that some customers spend up to eight hours per day responding to community posts. They are Zopa’s biggest advocates and, as such, are unpaid marketing champions for the cause. As a result, Zopa’s interventions in these dialogues are normally purely for technical or legal reasons or if it’s just plainly a mistake.

Having your customers as your community moderators not only means less staff dedicated to monitoring the conversation but also faster response times and more trust in the answers.

All in all, this is why Zopa use social media for customer servicing extensively, and state that twitter is one of the best service tools they’ve ever seen. Why? Because complaints are short – under 140 characters – and therefore easy to deal with. Not just that, but their staff think it’s cool to be using the latest technologies to deal with customers, not some boring old call centre operation for Zopa’s people. Furthermore, it’s in the public domain and that sends a powerful signal that they’re not trying to hide anything.

The social tools have built a trust that when the crisis hit has enabled them to compete effectively against traditional banks. As Giles pointed out, traditional banks weren’t particularly liked before the crisis, but they were trusted because they were old, big, safe, secure and reliable. Now, that’s not the case. Their image has been tarnished and Zopa have worked really hard on both the hard and soft things to ensure they can compete. For example, they have a completely transparent business model aligned with their social community platform. They position themselves as being ‘available to talk’ and pride themselves on being responsive and attentive.

He believes some others got this wrong, which is why it has hindered their performance. For example, you cannot be transparent and open some of the time. You are either open all of the time or none, there is no middle ground.

Giles emphasised this by saying that, because it’s in public, you cannot follow that line and then ask the customer to take something offline. He then posed a question to the more traditional financial firms: are you ready for transparency? Can you deal with it? And, more importantly, do your customers want to be social with you anyway?

What does this mean for the future?

Well, it means that banks will be componentised, a point I’ve now made so many times I’m fed up of making it.

The deconstruction of banks into component pieces is already happening and is being generated faster and faster, quicker and quicker, every day through apps and mobile internet.

Giles illustrates the theme well by likening it to the car servicing industry.

In the 1970s, all cars were serviced by their manufacturer, who made fat margins from replacement parts and labour. The customer was forced to drive their car to the manufacturer, at the time of the manufacturer’s choosing and would be forced to work to the manufacturer’s agenda.

Then a firm called Kwik-fit came into the UK markets, with the view that certain car parts – tyres and exhausts – were pretty much bulk standard and could be fitted without any really specialist knowledge or expertise. Result: cars could get these parts replaced at a fraction of the cost of the manufacturer, and whilst the customer waited.

The illustration shows how the industry was re-engineered from the supplier in control to the customer in control and this is what Zopa and their cohorts are trying to achieve – to take the parts of banking where margins are high for low value-add, and make them accessible to all at low margins through high value-add based upon direct connections enabled by today’s technologies.

I totally agree with this view, as I’m sure y’all would expect, and believe it will drive into all aspects of banking from payments to loans, cards to deposit accounts, and treasury to derivatives.

So the net:net is that the banking industry is being componentised and commoditised through apps and new business models and structures, such as Zopa's.

Question: has any bank noticed?

Giles's full presentation is available to members of the FSClub.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...