** out of a possible *****

And so the long awaited Independent Commission on Banking (ICB) produced it’s report yesterday, and we all went … hmmmm.

Some went hurray:

Shares in Barclays and Royal Bank of Scotland topped the FTSE 100 yesterday, as the interim report of the Independent Commission on Banking stopped short of recommending the break up of high street banks.

And some went boo:

Lloyds Banking Group lashes out at plans by the Independent Commission on Banking to make it divest more than the 600 branches.

Some think it’s good for the economy:

Chancellor says Independent Commission on Banking findings have justified coalition decision to set it up

And some think it’s bad:

In effect, the banks got off scot-free. The British economy and the nation’s taxpayers will be the big losers.

And some think it was just mush:

When it comes to justifying the decision to stop short of recommending a full separation of investment and retail banking the ICB descends into intellectual mush.

Me?

I think it’s a political compromise that assuages the banks whilst showing the governments trying to force a strong hand, when it doesn’t have one.

In essence, after a nine-month long gestation period, the report is like a pregnant pause. A moment of held breath that, when you release it, shows there was just a silent moment with little changed.

The report does have some good things in it, like the idea that banks should be fire-walled to allow the bit that can fail to do just that, but the overall view has to be that it’s just BAU (Banking As Usual).

Barclays share price bounced strongly upwards having dropped heavily last week. This was due to the expectation that prop trading, the Volcker Rule and even a return to Glass-Steagall would be incorporated in the ICB’s report, leading to a breakup of the bank.

That hasn’t happened.

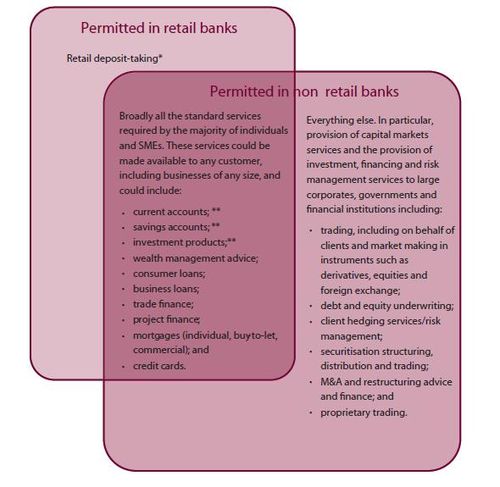

What happened instead is that the banks have been told that they must ring-fence the risky bits of banking – trading and investing – from the bits that need to be safe – retail and commercial.

This is so that if the risky bits fail in the future, they can be allowed to without impacting the safe bits.

I see it as like separating the jungle from the farm.

The jungle is the investment bank; the farm is the retail bank.

The jungle is full of dangerous animals that can kill you; the farm is full of nice things, like chickens and cows, which you control.

The jungle is full of risk and excitement and, if you come out the other end intact, you can reap big rewards; the farm is open and easy, with everything under control and reliable results the expectation.

What we had before is a single landscape within a bank – a Universal Bank – where the jungle and the farm existed on the same plateau. Hence, when the jungle went out of control, the wild animals ate all the ones we were trying to nurture for sustenance, and the whole bank failed.

Under the ICB’s report, the two must now be kept distinctly different. Therefore, two separate plateaus and a big chasm – or firewall – in between.

It sounds ok in theory.

It doesn’t go as far as Glass-Steagall, but it does go to the extent of making clear that if the jungle catches fire, then the farm is easy to save.

But that’s got nothing to do with long-term bank stability.

HBOS was a farm.

Northern Rock was a farm.

They both burnt down due to using the jungle for support and leverage.

Under the ICB view of the world, these farms would be safer because they would not leverage or use the jungle in quite the same way; and they would have far more capital in reserve, should the occasion arise, to survive a meltdown.

That cost of capital reserving will add about £5 billion to the bill for banking according to the FT, or even more than double that according to Oliver Wyman, which is why costs to customers will increase.

Meanwhile, the idea that the ICB has stimulated competition by making accounts easier to switch and telling Lloyds Banking Group to shrink further is also contestable.

Customers don’t switch accounts today. Is that because it’s hard, or because there’s no reason to bother?

Does the report make it easier for new banks, like Metro Bank, to launch?

Will a smaller Lloyds be any different to a bigger Lloyds?

Does it really make the banking world better?

Probably not.

That’s why I said last week that the Treasury Select Committee (TSC) had laid a bomb for the ICB. In that blog entry, TSC member John Mann called it “a whitewash”, published with conclusions made by “a bunch of elites coming up with something palatable to banks.”

Many would say he’s right, but then what can the ICB and Chancellor do?

Be radical and lose the banks support for the UK completely?

Lose all those tax pounds and pence?

No.

So the result is that Lloyds are a bit miffed as they are the target of being too big to retail, whilst the rest are fed up that Barclays has won the day.

For me, it was just another day in the jungle.

Watch your back.

Summary of the ICB report’s main findings nicked from Cicero Consulting:

Need for reform

- Banks tend to fail together and their liquidity and funding can be affected by a lack of confidence in financial institutions;

- A bank’s solvency can be threatened by a relatively small proportion of its assets going bad;

- Effects of bank failure are especially detrimental when it comes to the bankruptcy of systemically important institutions (SIFIs);

- Banks need to be allowed to fail and the probability and size of macroeconomic shock need to be reduced;

- Competition needs to be increased, especially in the field of SME lending and Personal Current Accounts (PCAs) where the market is most concentrated;

- The currently concentrated retail banking market in the UK can lead to poor outcomes for customers, as a larger bank has a lower incentive to offer good deals;

- No further action from the Commission to be taken on wholesale and investment banking operations, but more transparency is called for.

Current reform initiatives

- The Commission’s work reflects wide changes to capital requirements, such as Basel III;

- The FSA is expected to publish a consultation paper in the latter half of 2011 setting out its recovery and resolution plans;

- The Financial Stability Board requires the authorities of international financial institutions to meet annually in cross-border, firm-specific ‘crisis management groups’;

- The Basel Committee on Banking Supervision has introduced qualitative measures to improve liquidity risk management by requiring banks to establish a liquidity risk tolerance level;

- More regulatory oversight needs to be paid to the shadow banking sector to avoid transferral of riskier activities;

- The regulation of derivatives has been based on standardising OTC derivatives and clearing them through Central Counterparties (CCPs);

- The new tripartite institutional supervisory system in the UK will allow for timely identification of emerging risks to the financial system.

Reform options - financial stability

- Banks differ from other commercial institutions in terms of their vulnerabilities, and ability to leverage risk;

- The Commission is considering whether the Basel capital ratios are appropriate for SIFIs;

- The optimal capital ratios set out by the Commission as between 7 per cent and 20 per cent.

- The Commission is looking at a SIFI surcharge of 3 per cent, bringing the credible minimum SIFI capital ratio to 10 per cent , but accepts the need for international agreement;

- To tackle the issues raised by universal banking, namely the high impact of failure, the increased risk of system failure and increased risk taking, the Commission sets out the concept of a retail ring fence;

- Without safeguards, the Commission concludes, universal banking increases the risk of the failure of the financial system;

- A retail ring fence would strengthen the UK banking system and make the sector better able to absorb shocks;

- Whilst full separation would guarantee seperability during a crisis, the Commission feels that it would also remove all bank diversification and therefore increase risk ;

- Contingent capital (CoCos) has benefits, but the appetite for such capital is questioned;

- The Commission states that implementing the Volcker Rule in the UK would be unlikely to have a significant impact and would fail to address concerns about conflict of interest;

- The Commission sees little evidence to suggest that these changes would have a significant impact on competitiveness, and will be broadly neutral in effect in an international context ;

- Domestically the Commission accepts that there may well be employment and tax loss as a result of some of the proposals, and whilst there is a paucity of evidence the Commission feels that any impact would be small.

Reform options - competition

- Structural and behavioural changes are necessary to deal with the lack of competition in UK retail industry operations;

- Enhancing divestiture is an economically efficient way to promote competition; the Lloyds divestiture in particular could give rise to a new challenger;

- Barriers to entry into the banking market need to be lowered;

- Consumer choice needs to be improved significantly, real and perceived complexities in switching accounts and comparing products need to be rectified; and

- Competition in the banking sector must be subject to active monitoring and improvement by the FCA

Download and read the full ICB report here.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...