I was talking about lots of things yesterday but one conversation sticks in my mind more than any other: who will Lloyds sell their branches to?

This is all wrapped up in a debate with the European Commission dating back to 2008, when the UK government flouted competition rules to approve the emergency merger of Lloyds TSB and HBOS. This was viewed as anti-competitive by the European Commission, but was approved under the caveat that a restructuring plan was put into play.

The restructuring plan, agreed in November 2009, “contains a divestment package in Lloyds Banking Group's core business of UK retail banking as a measure to limit the impact of the aid on competition. The divested entity will have a 4.6% market share in the personal current account market gained through a network of at least 600 branches.”

The aim of this sell off divestment, called Project Verde by the bank, is aimed at creating a new competitor or to support the growth of a smaller existing competitor in the UK retail banking market.

The Commission argues that this will “remove the distortions of competition created by the aid”.

In other words, it’s a bit like the RBS sell-off of branches to Santander or the ING Direct USA sale to Capital One. Something that Lloyds, RBS and ING didn’t want to do, but was forced upon them in exchange for their bailouts (slightly different to the American approach to TARP mesays).

Anyways, back to Lloyds.

Eighteen months after the plan was approved by the Commission, the divestment is in play and 632 branches are being organised for sale, equivalent to 22% of the bank’s UK branch network. Bids will be received by the end of July and will then move into the Phase 2 due diligence process for the shortlisted few.

The details were announced at the end of May with a press release from the bank:

“The Verde business will have around five per cent of the UK personal current account market, over 600 branches and will become the seventh largest bank in the UK. It will bring together the Cheltenham & Gloucester business, Lloyds TSB Scotland and over 250 branches from the Lloyds TSB network in England and Wales.”

Paul Pester is the new Chief Executive Officer of the Verde business. In the press release:

“I am delighted to be in the position of shaping and growing a new business which will serve over 5 million customers and service over 8 million accounts. The new bank will be an exciting addition to the UK market and will be focussed on promoting competition and delivering great products and services to its customers.”

Paul’s senior team, most of whom will transition across to the acquisitive firm, will be:

- Darren Pope, Transitional Finance Director

- Helen Rose, Chief Operating Officer

- Neeta Atkar, Risk Director

- Peter Navin, Network Director

Peter is currently the Network Director for the Bank of Scotland and Lloyds TSB Scotland branch networks. He is also the CEO of Lloyds TSB Scotland plc.

The divestment will complete before November 2013, when all the customers and branches will move across to whoever the buyer is.

And there’s the rub: who will buy them?

We have the normal suspects: Virgin and Tesco.

Virgin may have a challenge if they want to buy the Verde business due to the history between Paul Pester and Richard Branson.

Before joining Lloyds in 2005, Paul was CEO of Virgin Money for five years. He left in a bit of a dispute with Virgin Chief Branson, when the bearded one pulled a leaving package that had been agreed, and left Paul with something that was half of what it would have been. Something that still grates with Paul, although I’m sure he’s big enough to get over it. However, it does mean that the deal will be negotiated really hard and, having seen the performance with Northern Rock back in 2008, Virgin never pay over the odds for a business so I think they’ll back off.

Tesco?

Tesco doesn’t need these branches as they have stores in most of the strategic locations they need, so forget them.

National Australia Group, who own Clydesdale and Yorkshire, or a similar smaller existing competitor … not really. I cannot see any small bank wanting to take on board 632 new branches from a large competitor.

After all, even though the sale is going to make them a big player, how do you check these branches are decent? Sure, the European Commission ruling stipulates that they must provide full coverage representing the demographics and operations of the bank, and are in decent geographic locations, but that isn’t easy.

The integration of the branches, the staff, the processes, the products, the systems and everything that goes with it won’t be easy.

There’s another wrinkle in the process of the sale here as well, as highlighted by Robert Peston of the BBC:

What makes a disposal close to impossible is that Lloyds has been instructed by the European Commission to sell £68bn of assets, largely mortgages, and customer deposits of nearer £35bn. So there is what bankers call a funding gap of more than £30bn. The point is that any buyer would have to pay Lloyds £68bn for the assets, but some £35bn of this would be covered by the £35bn of deposits that are being transferred to the successful bidder. The remaining £33bn has to be raised from investors in the form of regulatory capital and new debt. Or to put it another way, any successful bidder would have to borrow at least £30bn.

This is why Lloyds went out and got some further £15 billion of funding back in March I guess, but it’s not enough to cover the funding gap Peston highlights.

So a small UK competitor swallowing such a massive divestment won’t be something any of them would want to take on board that easily.

This rules out Metro, Newbank and others too. After all, imagine taking on 632 branches. Not only do you need the massive capital funding to cover the deposit base, but you also probably need a further 25% or more of the price to invest in a branch refit and rebranding.

So then you start to look overseas for buyers.

Santander would have been a contender a few years ago, but they won’t buy the sell-off … they’ve already become a mainstream UK branch-based bank through acquisitions from Abbey, Alliance & Leicester, Bradford & Bingley and RBS, so an additional 632 branches won’t help.

Maybe another EU bank?

BBVA? Probably not, as they’re not here now and strategically look to Latin America.

Deutsche? Too busy bailing out Greece.

BNP Paribas? Un banque francais dans Grande Bretagne? Sur mon corps mort.

Overall, I would say that Europe has enough domestic issues to warrant zero interest in buying a new UK bank divestment in a zero growth market.

So then we look to further shores.

The USA?

Citi, JPMorgan or Bank of America?

It would be interesting.

A US bank with the American culture of innovation, marketing and service, would be good for the UK. That’s what Metro Bank are bringing over here. But Citi, JPMorgan and Bank of America are still grapping with domestic issues too and, as mentioned, buying a new UK bank divestment in a zero growth market is not attractive.

So to Asia.

Asian companies are buying Western firms … but only those that offer strong brands or manufacturing capabilities to sell back into Asia where the growth is.

So buying a Cirrus or Volvo makes sense, but buying a UK bank in a UK market with UK customers and UK growth rates?

No.

So there’s no obvious buyer out there.

Add onto this that the Vickers Independent Commission on Banking (ICB) reforms state that even more branches should be sold than those required under the European Commission ruling – possibly up to 1,000 branches rather than 632 – and you can see a real muddle of challenge here.

If the bank resists this requirement then an antitrust probe could ensue, which would block government plans to begin selling its holdings in the bank next year.

The ICB recommendations are yet to be finalised, but this could be an extra spanner in the works for the Verde divestment plans.

The deadline for the sale of the branches is November 2013.

I won’t be holding my breath and neither are Lloyds, as they’re already talking about having to float this off as a separate business:

“The sale has always been part of what we call a ’dual-track’ process. We are obviously looking for buyers but we can do an initial public offering if we need to. Clearly, people are showing a great deal of interest in the branch network but we need to ensure that we achieve the maximum value for our customers and our shareholders.”

Nothing simple here then.

Final, final point.

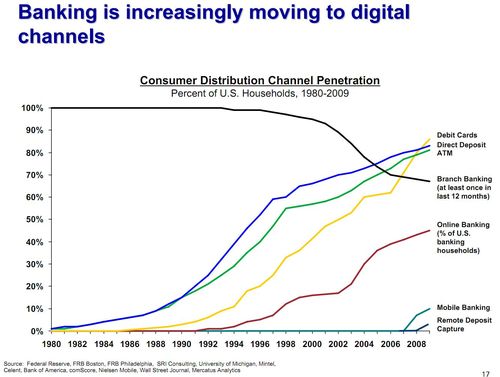

What have branches got to do with competitiveness anyway?

ING Direct USA became one of the largest banks in America without a large branch network. That's why they're called 'Direct'.

Equally, some would claim branch is past competitiveness whilst direct is future ...

Source: Capital One's presentation on the acquisition of ING Direct USA

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...