Derek Wylde, Group Head of Fraud at HSBC,

presented at the Financial Services Club last week.

He talked about many aspects of fraud and risk,

and presented quite a few numbers

related to the issue.

One of the charts raised questions in my

mind. It related to the total cost of payment card fraud. According to Derek, payment card fraud costs

an average of six to eight basis points on sales. For those who don’t use the terminology of basis points, a basis point

is 1/100th of a point, or 0.01 if you prefer. So fraud costs between 0.06% to 0.08% of the

total sales in payment cards.

Doesn’t sound like much does it.

Just eight basis points.

To put that in context however, a basis point of

card sales is worth billions, so eight basis points is a pretty large amount.

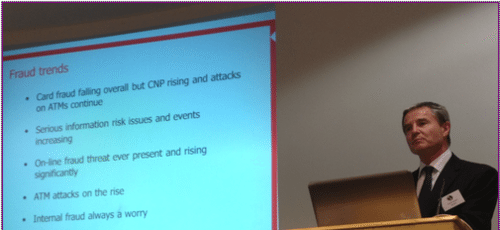

You can now see why fraud is an issue, and Derek went on to discuss the main trends in the industry, which include:

- card fraud falling generally,

although cardholder not present (CNP) attacks are rising; - ATM attacks are on the rise;

- serious information risk

issues and events are increasing; - online fraud threats are ever

present and are rising significantly; and - internal fraud is always a

worry.

Derek expanded on these points in depth, marking

the success of Chip & PIN as a key component of the success in minimising

fraud. He confidently expects the US to

follow the example of the rest of the world therefore in eventually adopting

Chip & PIN (although my sources say different).

With regard to ATM attacks, I was quite surprised

that these are on the rise, with an increase in ATM fraud in Europe of 63% over

the last year. My surprise is due to the

fact that much of the card fraud related to ATM attacks I had heard about years

ago, with crooks sticking webcams and wireless emitting devices into the

frontage of ATMs to get card data and PIN shots of customers using these

machines.

Apparently, such issues are still rife with card

skimming, reversal fraud card and cash trapping increasing and, more recently,

incidents of malware injection into ATMs to capture magnetic stripe data.

Derek went on to cover the whole gamut of mobile

and internet fraud issues, with phishers and the rest still creating a sea of

issues for the bank.

His summation is that the industry needs far more

support from the technology community to minimise fraud in the future, and

demanded real-time monitoring and analysis to enable the bank to capture the

crooks. Real-time is key as you only get

one chance to catch the criminals, never a second chance.

A sobering message and one that I also take to

heart.

At the end, Derek put up a cartoon that I found particularly

amusing for two reasons. One is that

it’s very funny and the second is that it’s an Alex cartoon, and reminded me

that we recently had Alex’s creators Charles Peattie and Russell Taylor

speaking at the Financial Services Club.

Therefore, for all of you who enjoy a good laugh, enjoy (doubleclick image to enlarge) …

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...