In America and Europe, stress tests are regularly applied to see whether the banks are becoming more resilient to another crisis.

The latest results of the American stress tests shows that all but one (Zions Bancorp) of the top 30 US banks are ok.

Europe is different.

Having said that Europe has fudged their previous tests, this time they’re serious.

The reason is that the stress tests are meant to completely analyse and gain transparency of Europe’s banks, prior to the move towards a Single Supervisory Mechanism (SSM) under the European Central Bank (ECB) in November.

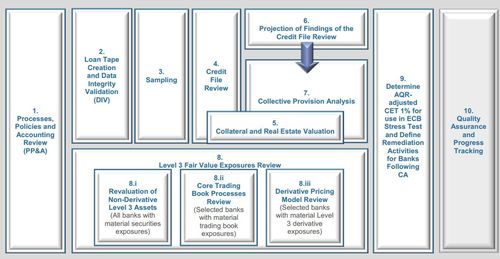

As a result, 128 of Europe’s banks are seeing auditors and regulators crawling all over their data and seeing what their quality of loans and assets look like.

It’s a real headache for all those involved in Asset and Liability Management (ALM), and for the bank in general.

For example, one bank told me that they have to report their exact position for mortgage exposures based upon the exact remaining term of every mortgage on their loan book. That sort of information has not even been reported at the aggregate level in the bank in the past, so they have to create new systems and calculations to cope.

Another smaller bank has told me that the cost of having the auditors working on their books with other creditable people is around €10 million to produce the data required for the Asset Quality Review (AQR). That figure excludes the circa 50 full time staff dedicated to the project internally.

In other words, the AQR will cost at least €2 billion this year, and that is at a conservative level of calculation.

Good news for the audit firms, but bad news for the banks.

Even worse, once all this is done, that is not the end of it.

This is because the aim of the AQR is that the ECB clears out all exposures in Europe’s banks before taking over their regulation. The results of the AQR are therefore meant to be top secret until released in October.

That creates two issues.

First, the banks are quaking in their boots as they have no idea what will be announced until it is announced. This means that a bank might find it’s failed the stress test but only find out on the day.

Second, if they find out beforehand, what does that mean? Will the information be leaked? Will the information be leaked anyway?

After all, as Reuters reports:

“The problem is that the health checks will be done in different stages. Right now, more than 1,000 auditors and independent specialist appraisers are trawling through trillions of euros of assets, checking whether banks have set aside enough capital to cover potential losses.

“A stress test will follow in May and June to check how banks hold up under potentially damaging scenarios.

The auditors have been asked to keep test-related information to themselves, but banks might be able to draw conclusions from the data and additional information the auditors are requesting.”

For those who want to know more, checkout the ECB’s AQR manual.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...