I don't write a lot about investment banking and capital markets because the readers of this blog are primarily in commercial, transaction and retail banking, but I am going to write about it today as it seems a real shame how we've killed investment banking.

From Barclays slimming down BarCap so fast that it looks like it's wrapped itself around a gastric band to Goldmans' top traders having a seriously bad bonus year, is it time to call the banker-bashing of casino capitalism over? Possibly, as all trends are moving to a vision I blogged about six years ago, where all the trading has moved out of the banks and into the markets.

In fact, it strikes me as scarily accurate looking back to what I said back in 2008, as one of the key thrusts of the article is that investment banks had died a death as regulation forced all trading into private hands and they just became technology links for trading private bets.

Today we see JPMorgan, Citigroup, Barclays and more shelving their prop trading - as Volcker means it doesn’t make sense - and leveraged models - as Basel III says it doesn't make sense - to move back to plain old boring commercial and retail banking - as Vickers says they have to be separated anyway.

The regulators and politicians believe they have achieved what they want - to derisk the markets - whereas I say they've thrown the baby out with the bathwater.

Y'see we now don't have a decent investment bank left in Europe.

The ones that were leaders have been hit by too many scandals - LIBOR, FX, rouge traders, money laundering - and the fines have hurt too much for any of them to want to stay in that game.

Add on a final overhead of trade reporting and systematic internalisation through Dodd-Frank, EMIR and MiFIDII, and you get a sense of just how much the markets have been transformed through failure, fear and fines.

Again something I blogged about a while ago (a wholesale reconstruction of the markets).

Which brings us around to what has all this achieved? Are banks no longer risky? Have we wiped out too big to fail? Has the global integration of markets changed? A little bit.

I would still claim there is risk and systemically important financial institutions that are too big to fail, but we have built greater resilience into the core banking system.

But at an expense of liquidity and transparency.

The result of all of this change is the private equity, venture capital, hedge funds, asset and wealth mangers, corporate treasury and more still wants to make a buck, but they'll now make a buck elsewhere.

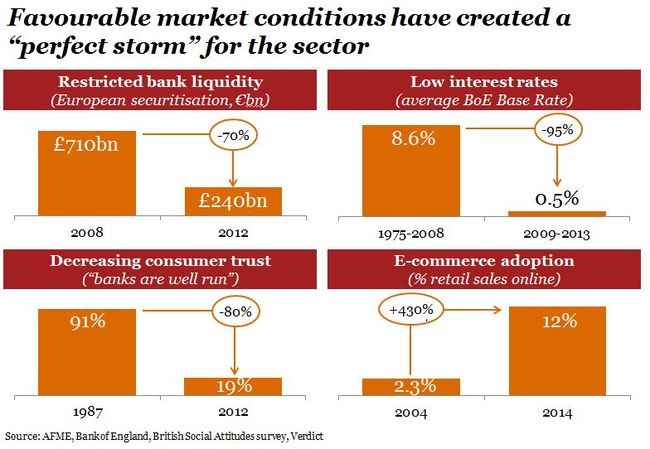

In fact, just as Zopa CEO Giles Andrews' put it, when he spoke at the Financial Services Club in April, the regulators and banks created this perfect storm.

Source: PwC

As markets crashed and credit dried up, individuals had to look outside traditional funding circles to find borrowing to cover their needs.

And so they came to Zopa.

The same is true in capital markets.

As the buy side and their brethren find the sell side offerings drying up, leverage and liquidity disappears and moves elsewhere, I would contend it moves to the shadow banking system.

And shadow banking is just that: a murky pool of invisible trading that avoids the regulatory oversight.

Hence, if traders cannot get away from the regulators in on-exchange trading, then expect them to move to markets that are off-exchange.

And that means that the next wave of regulatory microscope will be applied to the off exchange, shadow banking system.

About time? Yes.

Will it cure the cancer of risk in leveraging to make a buck?

No ... but at least it will ensure eventually that the risks and leverage is not at the expense of the economy or the country.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...