I’m called by a number of people about the BNP Paribas fine today.

The fine looks like a done deal of $8.9 billion, and includes the bank admitting criminal charges as well as being banned from US dollar clearing.

Why so bad?

Because BNP failed to co-operate in the SEC and Federal Reserve’s investigations which, once concluded, discovered that the bank had processed $100 billion of transactions from banned countries including the Sudan, Cuba and Iran between 2002 and 2009.

This is terrible news for BNP Paribas, one of the largest transaction banks out there, and will be a serious problem for their business. Sure, they can find a counterparty to process dollar payments for a year (or six months if the ban is lessened), but it’s not a good thing and will result in higher costs for their customers.

Equally, this ban and fine build on other heavy hitting actions from the US authorities including a $2.6 billion fine with a criminal charge against Credit Suisse six weeks ago and the $1.9 billion fine against HSBC in 2012. Add on Benjamin Lawsky, the US attorney, fining Standard Chartered for money laundering, and you have a real list of named and shamed banks:

$2.6 billion: Credit Suisse

In May 2014 the bank pleaded guilty to helping rich Americans lie to avoid paying taxes.

$1.9 billion: HSBC

The British bank agreed to pay up in December 2012 to avoid prosecution for complicity in money laundering.

$1.5 billion: UBS

In December 2012 the Swiss bank paid out to put an end to legal proceedings linked to the alleged fixing of the inter-bank Libor interest rate.

$1.0 billion: Rabobank

The Dutch bank paid just over $1.0 billion in October 2013 also for proceedings over the alleged Libor rate rigging.

I’ve already blogged about the hypocritical approach of the US authorities but, as was pointed out by Evan Davis on The Today program …

Today Program, Radio 4, 30 June 2014 on BNP Paribas fine

… they have also been fining their own:

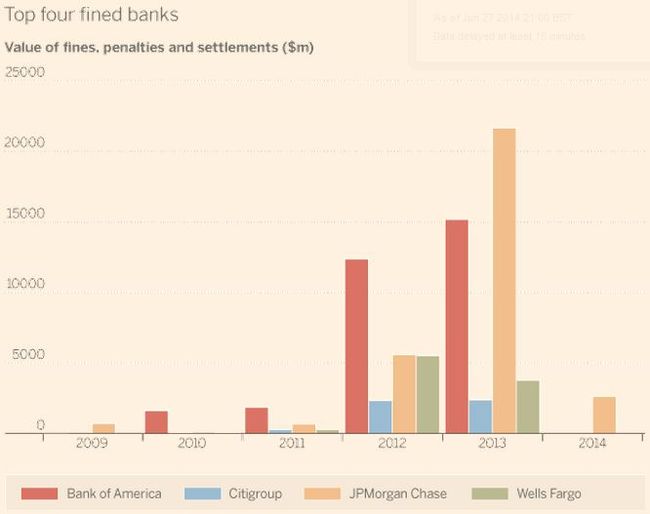

$25 billion: Wells Fargo, JPMorgan Chase, Citigroup, Bank of America, Ally Financial

In February 2012, the banks collectively agreed to pay this amount - $20 billion in various forms of relief for home-loan borrowers and $5 billion in penalties and contributions to a cash fund for unfairly foreclosed homes -- to avoid prosecution over abuses.

$13 billion: JPMorgan Chase

The bank, Wall Street's former poster child, paid in November 2013 to resolve a series of US and state lawsuits over the sale of toxic mortgage-backed securities.

$11.6 billion: Bank of America

One of the rare big US banks whose headquarters is not in New York, the North Carolina-based Bank of America also paid the biggest penalty for the subprime mortgage crisis. In January 2013, BofA paid this fine to settle claims that it sold US government-controlled mortgage finance giant Fannie Mae hundreds of billions of dollars' worth of dud home loans.

$9.5 billion: Bank of America

On March 26 this year, the bank, America's second-largest lender in assets, agreed to pay $9.5 billion to settle litigation by the Federal Housing Finance Agency over mortgage securities sold to Fannie Mae and fellow agency Freddie Mac.

$8.5 billion: Bank of America

In June 2011 the bank agreed to compensate a group of investors who said they lost money on mortgage-backed securities bought before the financial crisis.

$1.7 billion: JPMorgan Chase

In January the bank agreed to cough up to resolve charges its lax oversight enabled Bernard Madoff to build up the massive Ponzi scheme that bilked investors of billions.

The difference in the fines, as can be seen from above, is not the scale but the rule.

American authorities are punishing overseas banks for breaching US rules on trading whilst fining their own banks for screwing their customers and the government.

Of course, we all have domestic issues and focus – just look at the $30 billion costs for PPI mis-selling – but we do wonder when the issues will end.

We begin with mortgage fraud, PPI and swaps mis-selling, losing billions of taxpayers’ money, creating risks through casino capitalism and calling customers muppets then, just as you think it cannot get any worse, it does.

Insider trading; supporting dictators, drug runners and terrorists; creating tax dodges that are criminally fraudulent; rigging markets through fixing LIBOR and FX rates; and, in the latest twist, screwing customers through flash trading in dark pools.

The feeling in this constituency is: when will it all be over?

The feeling in the regulatory circles is: will it ever be over?

The fact is that yes, it will be over one day. The challenge is that as the skeletons in the banking closets are found and buried, another one pops out.

There are many, many issues of banks behaving badly over the past decade, and the regulators will not sort this one out until they open all the cupboard doors. For example, other cases under way could smash these records. Bank of America is facing a possibly $12-$17 billion penalty, while Citigroup could be facing as much as $10 billion for more bad business practices in mortgages which were the origin of the global financial crisis.

So how far have we got?

About 75% of the way.

That means there’s probably another five or six big issues to come.

What are thy?

More mortgage issues in the USA (there’s about another $20 billion of fines to come over that); more making profit at the customers’ expense cases (there’s a whole raft of questions still to be answered over business foreclosures that could outscale the fines for mortgage foreclosures); more individuals behaving badly (we’ve had a Whale and an Adoboli, but insider trading is still a rich seam to be tapped); and more general selling of products inappropriately.

The bottom-line is that clearing up the mess of the banking system is going to take a long-time and it’s not just regulating to get banks to behave in a socially useful fashion, but it’s punishing to show banks that past behaviours are unacceptable.

A fine balance between dealing with past issues and creating a resilient system for future ones where the real challenge is not to throw out the baby with the bathwater.

American Authorities

Bank fines to date for US banks over mortgage issues (from the Financial Times):

Bank fines to date for overseas banks in the USA (from the Wall Street Journal):

European Authorities

Bank fines to date from the European Commission (from the Financial Times):

UK Authorities

Bank fines to date from the Financial Conduct Authority / Financial Services Authority (from the BBC):

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...