We had a very succesfful third meeting of the Financial Services Club Nordic Region in Stockholm the other night (checkout what happened at the first and second meetings if of interest).

The focus was upon innovation and, specifically, innovation in payments with presentations from:

- Lazaro Campos, former CEO, SWIFT;

- Richard Jones, Head of Industry Business Development, VocaLink (UK); and

- Christina Friberg, Marketing Director with Bankgirot.

Lazaro kicked off with a keynote that made clear wholesale, retail and commercial banking is being disrupted by the regulatory regime, changing customer attitudes and the digital revolution.

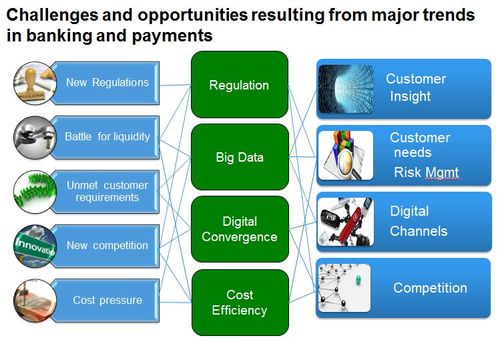

In wholesale banking, there are a number of major challenges to deal with:

- Heightened regulations is the new normal

- Battle for liquidity increases

- Increasing and fragmenting customer requirements driven by technology development

- Entry of new players and emergence of new business models

- Continued pressure on cost to maintain payment margins

Add on to these challenges the technology changes:

- Big data technology to gain customer insights

- Analytics to understand customers’ needs, improve risk management and compliance, and boost efficiency

- Digital channels (Internet, mobile, tablet, social media) to push for digital convergence

- Rationalize legacy to provide better services and reduce total cost of ownership

... and the world is a dizzying array of opportunity and threat. (doubleclick picture for a larger image):

In retail banking, the changes are even more dramatic with more people owning a mobile phone today (4 billion) than a toothbrush (3.5 billion).

And that is just a start as the internet of things is coming, with all things communicating and having intelligence on the net.

The challenge here is that everyone expects everything to be available everywhere all the time, in real time, for free. How are we going to make money in this space?

Lazaro argued that the focus has to be upon creating increased value for the consumer from:

- Delivering truly incremental tangible financial value (greater return / less costs)

- Identifiable emotional (reassurance; customization)

- Physical benefits (speed)

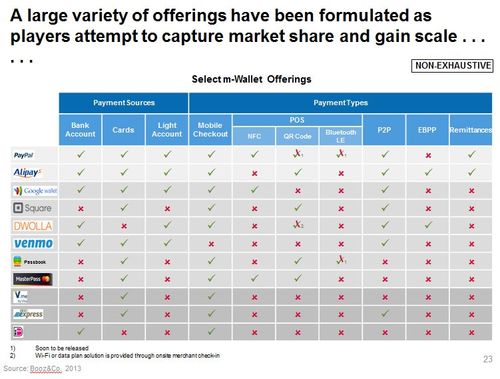

And then moved on to all the new players, incumbents and others making inroads into this core space through m-wallets and more:

His conclusion however is that this space is not being fundamentally changed.

If you look at all the new players, none have really made a significant impact apart from those who offer fully integrated end-to-end integrated capabilities like a PayPal or Starbucks.

Even so, there are major changes afoot and banks cannot be complacent to such change:

- new, innovative business models are hard to come by. emergence of non-card based instruments by trial and error

- end-to-end real-time, same day value clearing and settlement infrastructure essential

- conflicting demands (service vs price, anonymity/data privacy vs transparency) complicating evolution but driving innovation

- banks re-discovering and reconsidering the space. offering evolving to address retail demands:

- account switching, account masking, identification proxy services, light accounts

- big data for mass customisation

- price revolution due to new regulation, competition, customer expectation and shift back to transactional banking

Lazaro’s speech was well received and, in response, VocaLink and Bankgirot talked about how the back-end infrastructures are responding to these rapidly changing front-end interfaces.

The core is real-time everything.

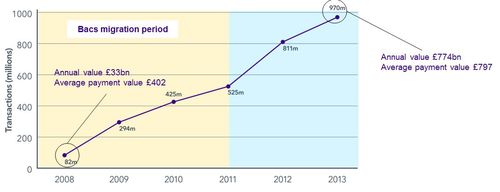

Richard Jones from VocaLink made this clear by starting with the UK experience of faster payments, which has risen rapidly especially after the BACS migration:

This growth is driven by consumers, businesses and government.

- Consumers have increased the number of single payments (probably cash and cheque migration) e.g. 33% growth in 2013 so that 60% of FPS volumes are single payments

- Businesses and government are taking advantage of the service:

- New services such as pay day loans

- Improvements to existing services e.g. ability to pay temporary / agency staff rapidly, rapid payment of settled insurance claims, etc

- Government emergency payments to citizens

- Consumers substitution for cash and cheque

And now there are new services like PayM and Zapp which enable P2P mobile payments and place banks at heart of mcommerce in the UK.

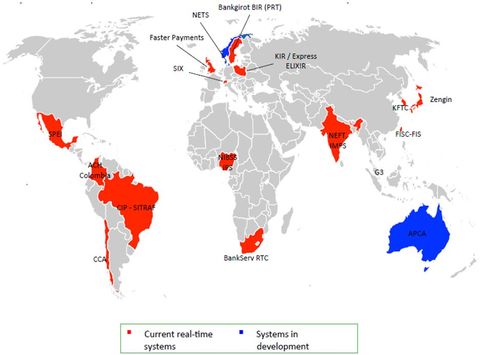

But real-time is not just a UK phenomenon but a global one.

... and this was made clear in the final presentation from Christina Friberg who presented the Swedish experience of real-time everything.

She began by specifically focusing upon the fact that their service offers real-time clearing and settlement in seconds – the processing is just 1 or 2 seconds – and it is available 24*7*365.

This is pushing boundaries further than most other country examples, as demonstrated by thte mobile payments service Swish .

With Swish you can transfer money via a connected mobile phone to any mobile number connected to the service at any time of day, year around. Funds are transferred in real-time account to account between affiliated banks to the service.

Key to the success and the customer adoption of the Swish service are:

- the simple and useful use case (real-time money transfer person-to-person),

- the very simple to use mobile app and

- the trust/security having all the big banks behind the service.

Danske Bank, Handelsbanken, Länsförsäkringar Bank, Nordea, SEB, Skandia Bank, Swedbank and the Savings Banks all support the service, and combine the Swish app with a specific digital identity app called BankID.

Launched at the end of 2012, the service ended 2013 with over 500,000 active users and more than 1 billion SEK (€113 Million) in transaction volumes.

All in all it was clear that the payments world is innovating and that banks and infrastructures are pushing the boundaries but, at the end of the meeting, all three presenters agreed that banks are not innovating enough.

The view was that here are two sorts of banks: those who see digital as another channel, and those who see digital as the foundation of their bank.

Unfortunately, most banks fall into the former category and not enough into the latter.

That will change though.

Sometime.

Somehow.

Someday.

Somewhere.

Oh no, I’ve drifted into West Side Story.

Time to return to Sweden and the British Embassy Pub, The Pickled Herring.

Far more notable.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...