It's obvious that gamification is a game changer - apologies for the pun.

Gamification is huge.

The games industry is bigger than the movies these days, with Call of Duty, Halo and World of Warcraft, leading the charge but we must not forget Angry Birds, Candy Crush and the range and reach of Flappy Bird.

The gaming industry generates around $100 billion revenues per annum (dependent upon whose figures you look at, and how the stats are calculated), and is being pushed hard by mobile gaming (around half of games are now played on mobiles).

This is why banks need to put games high on their priority list for retail consumer banking but, unfortunately, most banks do not have such things high on their agenda.

After all games are for kids but that's where they're getting it wrong. Games are for everyone.

In fact, a large and growing number of women between 25-55 are gaming and making games such as Candy Crush a great business. Candy Crush has around 700 million players a day, mostly female, generating almost $1 million a day through in-app game sales.

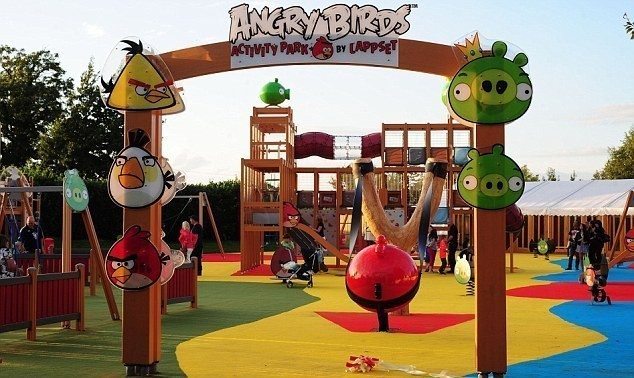

And games gradually extend into other areas. For example, just look at how Angry Birds has gone from a digital game to a physical game to a theme park (45% of Rovio, the maker of Angry Birds, revenues are from merchandise sales).

Gamification offers two specific innovations for banks.

One is that they can be used to change or train behaviours.

As I blogged a while ago, Zombie gaming taught me to use Spare Change, the predecessor to Facebook Credits.

Once you've learned how to use a virtual coins in a gaming world, it's only a short hop, skip and a jump to using game coins in the real world.

This is the lesson learned from the Chinese experiences with QQ coins.

Initially deployed for gamification and personalisation of digital space, the coins rapidly transitioned into usage for pornography and gambling.

In other words, a game teaches you behaviours.

One of those behaviours is how to develop a value exchange in a virtual currency.

Once you have the knowledge of how to do a value exchange in a virtual currency, then you can build an alternative ecosystem around the virtual currency.

This is how bitcoin is taking off, by learning how to use bitcoins in a digital space, leading to using bitcoins everywhere.

But let's not leave it there as there is another way to look at games for banking.

Using games to teach customer new financial behaviours.

I only see a few players in this space today - Barclaycard, mBank, Garanti, Moven and fidor immediately come to mind - but this will move into the mainstream bank structures over time.

The idea being that you want to incentivise customers to save or not spend, to budget better, to recognise behaviours that will push them into unnecessary credit or fees, and related changes can all be achieved through gaming.

In other words, banks could make banking fun and entertaining and a little bit addictive, if they made the games to support key objectives with customers.

That is why Singapore based PlayMoolah won SWIFT's innotribe start-up challenge in 2012.

But then one final piece in the gamification world that surprised me the other day.

I'm enjoying a game called Real Racing and, for the first time, I get an in-app advert from a bank.

This is from a new UK bank called Think Money, who obviously think different.

Applying for their account is a piece of cake too.

Similarly, I get an ad in the app for bitcoins the other day ...

… from Bitstamp ...

… a Slovenian based exchange and, as the ad says, fully SEPA compliant!

I know that this is simple in-app advertising but how much priority are traditional banks making of such areas?

Very rapid change in behaviours, based upon simple consumer psychology using games as entertainment, not only gets new business but it also gets new business models.

It works and, as can be seen, some financial institutions are waking up to the opportunity that gamification offers as an educational tool, as an engagement tool and as an acquisition tool.

If your bank hasn't created a post of Chief Games Officer (CGO) yet, then I'm pretty sure they might soon ... except that it will probably get confused with Collateralised Game Obligations.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...