Blimey!!! When you start debating nuances of things with the Bitcoin community, it doesn’t ‘arf get into a pedants dream.

In this case, we clarified some of the dialogue about the blockchain and bitcoin yesterday. The net:net of that discussion is that you have to a have a native currency to use the blockchain. It doesn’t have to be bitcoin, but as that’s the one with five years of development, why would you use another one?

This then moved into a discussion of money, and what is money.

Some of the Bitcoin folks claimed that I didn’t understand what money is, and pointed to a couple of articles that show how they define it.

They define it as a track of debt. A record of exchange. A proof of contract.

Most Bitcoiners talk about the Yap islands, where Big Stones are the record of value, and point to a book by Felix Martin Money: the Unauthorised Biography .

They claim that money does not derive from government or barter systems, but is purely a record of debt.

I completely disagree. They claim I don’t understand money. I claim they don’t understand money.

You see, their definition of money covers all forms of exchange of value in communities from beads and shells to digital tokens: Money is transferable credit, and transferable credit is money. It always has been, it always will be. They even lump in accounting ledgers as money, which is a stretch too far.

That’s not my definition of money and, in terms of banking, this is an important delineation as this is what banks deal with.

My definition of money is cash or, to be more exact, the central bank definition of money which is M0. M0 is a "measure of the money supply which combines any liquid or cash assets held within a central bank and the amount of physical currency circulating in the economy (also referred to as narrow money)."

It is bank notes and coins. That is money. It is legal tender and trusted because it is backed by government. Anything else is a commodity of value. Gold, oil, gas, airmiles, beads, shells and bitcoins are all stores of value, but they are not money.

As Investopedia defines it, and this concurs with my view of the world: Money is the circulating medium of exchange as defined by a government. Money is cash, and the money circulating in the economies of the world based upon that currency.

By way of example, the first appearance of money, in the form of a nationally recognised exchange, is way back in Ancient Sumer when the priests discovered that the barter system had broken down. Farmers were producing an abundance of goods and some farmers now had excess and could not exchange or trade their produce. As a result anarchy broke out, with regular fights between the farmers over their goods and produce.

The priests saw the issue and invented money. Effectively, they created a national currency called the Shekel (nothing to do with today’s Shekel) and the farmers could cash in their excess or unwanted crops for Shekels which were then tradable with the women in the Temples who represented the Goddess Inanna on Earth.

In other words, money was invented at the same time as accounting (the second oldest profession) and prostitution (the oldest). That is what I call money – coins, notes and cash. All the other forms of value exchange before this – crops, beads and shells – were commodities that were recognised to have value, and were value stores, but these were not money in the definition of the term.

That is a matter of record and is why I assert that money was invented by governments to control societies.

In fact, this is where the reason for the definition is key. Money is controlled by government. Bitcoiners believe they now have money without government.

That is a fundamental friction and why I refer to bitcoin as a tradable commodity, but it's not money.

Now, there are many other forms of value exchange and recording of debt, such as Yap Stones and IOUs, but a Yap Stone or IOU is not money. It is not a freely tradable currency that can be exchanged for goods and services that is nationally recognised. It is purely a record of value store. That is one thing, but it is not money.

Equally, bitcoins, Gold, Silver or airmiles is not money, but a commodity that has value. Money, in its financial definition, is bank notes and coins that are tradable in a nationally or internationally recognised currency scheme.

This is where the Bitcoiners are confused: the difference between money and a store of value. It’s important from a banking perspective as we deal with the processing, transfer and management of money as our core, and are trying to see how bitcoins fit into this.

In this area, banks deal with money and then provide secure mechanisms for the currencies, stores of value, commodities and other tradable instruments. The latter are founded upon money, and are exchangeable into and out of currencies through work around the monetary systems of the world. That is where banks provide the exchange mechanism. The focal point here is then that, gradually, Bitcoin could circumvent this exchange mechanism, by taking the role of trusted third party away from the banks.

So the real thing here is that bitcoin becomes a fantastic digital exchange mechanism of value as well as a digital value store. That is why Bitcoin is a fundamental change.

Meanwhile, for the record, please stop mixing up your terminology Bitcoiners. Money is common legal tender, and takes the form of cash (bank notes and coins). It was created by governments (priests) to control societies (farmers) and bring stability and civilisation. Using money you can then buy value stores, such as bitcoins, gold and oil, that are tradable. These tradable commodities work across borders as stores of value in a physical form (gold and oil) and in a digital form (exchange traded funds and bitcoins), and overcome the need to use currency exchanges to translate one nation’s money into anothers.

Oh and by the way, we’ve just agreed to run a session asking: What is Money? with the Barclays Escalator on 27th January, debating the nature of currencies and value exchange, the role of fiat money and community currencies, and asking what all that means to the block chain. Leading the debate will be the ever present Dave Birch of Consult Hyperion. See you there.

Postscript:

When I refer to cash, I mean M0. I am specifically excluding trade finance that leverages M0, e.g. financial instruments and tradable commodities such as bitcoin and gold.

Oh and just for the helluva it, a blog post from almost two years ago:

January 23, 2013

Money is meaningless

I’ve blogged and presented about this subject many times before, so rather than repeating all that, here’s a summation with a new twist.

Money is meaningless because we no longer deal in money.

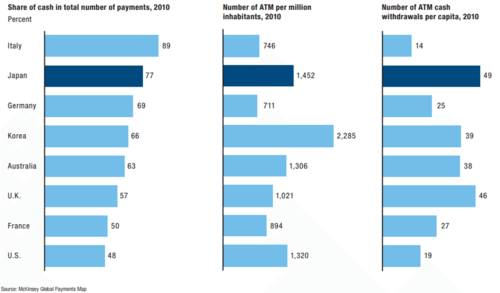

When we use the word money, most of us would envisage some brand new shiny, crisp notes coming out of a cash machine, but cash is declining fast.

Sure, there’s still a lot around,

Source: McKinsey Payments Report 2012

But cash in the economy is decreasing

Source: the Payments Council

And is primarily used for small value transactions

Source: the Payments Council

This is because electronic payments are taking off

Source: ATKearney

And now contactless and mobile payments are attacking that small value domain.

So cash disappears and is replaced by electronic, digitised transactions.

So money in the form of cash is less meaningful and that regular old nugget used in many presentations about the gangsterWillie Sutton, who was asked: “why do you rob banks”, and he answered: “because that’s where the money is”, is so last century.

Sure, Sutton is right, but he robbed banks physically, taking the cash out at gunpoint rather than by cashpoint.

Today, the gangsters take the money out byte by byte.

Money is meaningless because the data is meaningful.

It’s the data that gangsters need to rob, not the money.

Data is where it’s at.

That’s why the majority of cyberattacks target financial institutions.

According to RSA’s December 2012 Online Fraud Report, 284 brands were targeted in phishing attacks during November 2012, marking a 6% decrease from October. Of the 284 brands attacked 45% endured 5 attacks or less. Banks continue to be the most targeted by phishing, experienced nearly 80% of all attack volumes.

Sophos regularly report details of bank cyberattacks. Here’s the headlines from just the last three months:

- Leading US banks targeted in DDoS attacks

- US senator blames Iran for cyber attacks on banks

- HSBC recovers from DDoS attack, after internet banking services disrupted

- Fake Apple invoices lead to Blackhole exploit kit that drains your bank account

- Unmasked! Alleged mastermind of "Project Blitzkrieg" online attack plot against US banks

- US-wanted "bank hacker" is all smiles as he is arrested at Bangkok airport

- US woman arrested for bank robbery brags on YouTube about robbing a bank

And McAfee Labs researchers recently debated the leading threats for the coming year and show that it’s only going to get worse:

- Mobile worms on victims’ machines that buy malicious apps and steal via tap-and-pay NFC

- Malware that blocks security updates to mobile phones

- Mobile phone ransomware “kits” that allow criminals without programming skills to extort payments

- Covert and persistent attacks deep within and beneath Windows

- Rapid development of ways to attack Windows 8 and HTML5

- Large-scale attacks like Stuxnet that attempt to destroy infrastructure, rather than make money

- A further narrowing of Zeus-like targeted attacks using the Citadel Trojan, making it very difficult for security products to counter

- Malware that renews a connection even after a botnet has been taken down, allowing infections to grow again

- The “snowshoe” spamming of legitimate products from many IP addresses, spreading out the sources and keeping the unwelcome messages flowing

- SMS spam from infected phones. What’s your mother trying to sell you now?

- “Hacking as a Service”: Anonymous sellers and buyers in underground forums exchange malware kits and development services for money

- The decline of online hacktivists Anonymous, to be replaced by more politically committed or extremist groups

- Nation states and armies will be more frequent sources and victims of cyberthreats

So when we talk about our wonderful new internet age, the key is to realise that it’s the data where the money is, not the bank, the branch or the cash machine.

Or that’s my take on it anyway.

And if data is meaningful, then we could start a lengthy chat about Big Data and such like … but that’s far too overhyped for a discussion on the blog today, as I’ve had this debate so many times in the past. See these blog entries if you want more:

- I just met Big Data;

- Banks don’t need big data, just PFM;

- Data is a currency … we just haven’t realised its value yet;

- Data is a currency ... just like salt;

- Money is meaningless, as data is now key;

- The battle over information, and how information warfare is the new game;

- The fact that banks should move from being safekeepers of money to beingsafekeepers of data;

- Why banks should worry about Google, Apple, Facebook, and how these guys do data management better than banks;

- The fact that banks need to radically shake up and wake up to the data challenge; and

- How Amazon would organise itself as a bank, in terms of how bank silos inhibit their competitiveness.

So, for now, I’ll move on to talk about why capitalism is dead.

Oh, that’s tomorrow …

This is part two of a three part series:

- Part One: Mobile is not important;

- Part Two: Money is meaningless; and

- Part Three: Capitalism is Dead

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...