I find it interesting that so many bloggers on Fintech deride the banks for being slow, clueless or stupid. So many blogs talk about how banks don’t do this, don’t do that; fail at this, fail at that; have no idea, cannot change; are stuck in the past or have their heads up their arse.

C’mon guys. Do any of you, or us, really believe this? Does anyone seriously believe that the day someone joins a bank, they have their brain removed? Does anyone believe that you can rise to the senior management of a bank and have no clue? Does anyone seriously think that a bank CEO has no idea?

These are intelligent people. These are intelligent businesses. So to say that bankers are stupid, clueless and are ignoring the challenges they face, underestimates the banks and shows the absurdity of the author’s thinking.

In reality, every bank executive I meet is concerned about their future. They recognise that the traditional structures of banking are changing; that their margins, and therefore profits, are disappearing; that they need to move from physical to digital; that Fintech is changing the market for good; that peer-to-peer, mobile and blockchain are key; that … well, you get the idea.

Their problem is that they don’t know what to do about it and consultants cannot tell them. They tell me they have spoken with the big consulting firms and that they are as much at a loss to all of this change as they are. It reminded me of the moment in 2006 I heard that YouTube had been bought by Google for $1.65 billion. In a presentation made a year later, the story was told of how the then CEO of McKinsey called in his global team and asked them what YouTube was. None of them knew or had even heard of it, because they were firewalled out.

In other words, we are living in fast cycle change where many bankers – and consultants – are finding it hard to keep up. Right now, by way of example, we see a mega battle playing out between Stripe and Klarna and yet most bank executives haven’t heard of either company, even though they are core to their business.

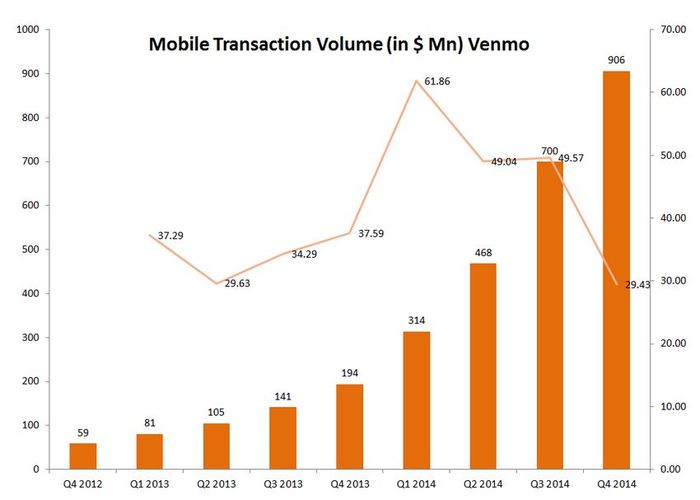

This is because of the very nature of Unicorns. Unicorns can appear within months and suddenly eat into our space. A great example is Venmo which, if it were an independent company and not now part of PayPal, would be a Unicorn. Venmo appeared as a result of a fun weekend amongst two developer millennials because one of the two friends forgot his checkbook. Now, just four years later, Venmo’s processing power is doubling year on year ($700 million processed Q3 2014 vs $1.6 billion Q2 2015) because it was designed by millennials for millennials and understands that developments can take place in hours (don’t even consider months).

Source: Let’s Talk Payments

This is the age of real-time almost free instantaneous change, and it’s hard for the overnight batch analogue generation to keep up. That’s why bankers don’t need to hire consultants or millennials. They just need to make sure they have a living, breathing culture of digital innovation.

I guess it was best wrapped up by a bank CEO yesterday who asked me, if I were in his shoes, what would be the first three things I would do. He runs a bank that is challenged by change, offers consumer loans, worries about P2P lending and distributes through branches.

I said to him that he firstly needs to build a vision based upon the premise that they will never see the customer face-to-face, only deal through screens and make no margin on their loans. I said that this vision needs to assume the consumer can get everything he does today for free elsewhere. Based upon this supposition: how is he going to make money?

You make money by delivering value in new forms, such as the Brazilian bank that is crowdfunding bulk buying of new cars in order to secure major discounts for their customers – and giving them competitive loans in the process. Like the Ukrainian bank that is overcoming the concerns about buying goods online by creating their own version of Amazon/Alibaba where you buy the goods online in the bank branch or at home and the goods are delivered to a secure locker in the bank branch. You only pay when you’re happy with the product and, as that happens to be when you’re in the bank branch, you can get a loan too.

These are the new models of banking where value is created through ancillary services to financial products, but not by the financial product itself. In a world where everything is free, banks have to be much cleverer at value generation, and not rely on old world products with fat margins that won’t exist in ten years.

Once you have a vision of how to make money when everything is free, then go build the vision. Communicate that vision. Share that vision. Live that dream. Make everyone excited and be passionate about what you believe. Finally, deliver the vision. Make it so, as Captain Jean-Luc would say.

So the three things I would do is create the dream, live the dream, deliver the dream.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...