I don’t know about you, but I’m completely confused about blockchains, sidechains and such like. I admit it. It’s beyond me and, if it’s beyond me, gawd knows how normal folk will make it out.

The reason it’s so confusing is that we’ve recently seen the rise of blockchain companies like R3, Ripple, Erethreum, Eris and more. What are they all doing and why do we need them? Surely a blockchain is a blockchain? Why do we need so many of them?

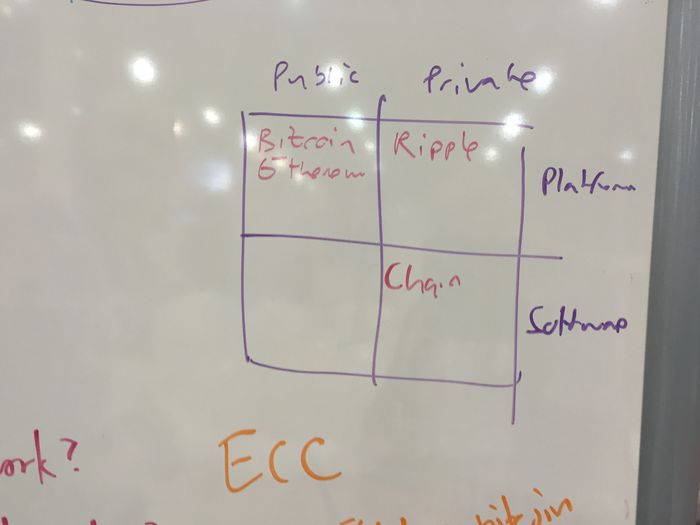

I asked this question around the exhibit hall of Money20/20 last week, and finally got a good answer from Chain. Chain are the partners of Nasdaq, and also working with several other leading light companies, and they pitched it that there are many types of companies developing on the blockchain protocol.

They even drew a chart …

… and split these firms into public and private blockchain developments that are either owned by the platform or offered as software. Chain focus upon private blockchain software developments which effectively means that the company provides software that allows firms like Nasdaq to privately clear trades in real-time. No bitcoin, no open systems. Just Chain, software and the bitcoin blockchain protocol to allow private, real-time clearing.

This kind of sets the scene, and then they drew me another chart that made this even clearer.

This is the pro’s and con’s of the blockchain world. Permission versus permissionless; trusted versus untrusted; controlled versus decentralised; structured versus democratised; etc.

The gist of all of this for me is that there are 100’s of developments on the blockchain. It is most likely that some form of controlled, permissioned system will emerge for the internet of value. Who will develop that system is the question, and what role will the current clearing systems take in that system? What will happen to the DTCC, Euroclear and TARGET2 structures? Will we need SWIFT, Fedwire, CHIPS or STEP2?

These are core questions about the future of our transaction processing systems and I don’t have the answers. Do you?

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...