We had two Financial Services Club meetings on the same night this week: one in London where Chief Executive of the Payments Council Maurice Cleaves talked about the landscape future for UK payments markets; and one in Warsaw where Lukas Dzuroska presented the top ten trends tracked in research by EFMA over the past year. I was in the Polish meeting, as it was also the first launch meeting for ValueWeb, and was intrigued to hear to the EFMA research.

Littered with global examples, EFMA have been running an awards program with Accenture for a few years now, to recognise global banking innovation. The examples included many of my favourites – Commonwealth Bank of Australia, DBS (Singapore), mBank (Poland), Deniz Bank (Turkey), Standard Bank (South Africa) and more – and showed ten key trends emerging in the past year, of how banks are absorbing innovation.

#10: Data Monetization

Banks are recognising that their data analytics can leverage market opportunity, for example NedBank in South Africa offering merchants far more business insights through market intelligence services. Customers are willing to pay for this, and the banks that offer such services are more sticky.

#9: Social Value Chain

Banks don’t need to do all the work as customer can, and they want to. Many banks are engaging customers in crowd sourcing ideas, with Widiba (Italy) picked as a great example. Widiba asked customers to design the features of the next generation bank which have now been delivered.

#8: Robot force

There are a few gimmicky robot services out there, particular in Japan where robots replaced tellers (I thought we had done the same in the UK until the teller moved and I realised then they were human), but it’s not just robo-advisors that are taking off. After all, take a look at UBS who offer a real-time portfolio analytics services on a personalised basis to all of their high net worth clients through IBM’s Watson (DBS do the same).

#7: The Banking of Things (BoT)

We know the Internet of Things (IoT) is coming, and it will need BoT based upon the ValueWeb to support it, but things are already emerging in this space. US Bank offers a link to light bulbs to flash you when something is happening on your account whilst Bradesco offers a connection between your car and your bank account. But the example that Lukas showed was ASB from New Zealand who have created a fun way to inform children about money called Clever Kash. Here’s the video:

#6: Intermediate Everything

It’s funny how I’ve about banks being disintermediated since the 1990s and yet they’re still here and they’re now bigger. I don’t believe banks will be disintermediated or, as we now call it, unbundled. Banks instead are reintermediating and rebundling everything and this trend proves it. There are various examples of this, specifically the idea of predictive analytics and partnering to remind you that you that it’s your partner’s birthday today, for example. The idea here – a stretch for most banks – is that the bank will not only know it’s their birthday, but will tell you what you brought them for Christmas and for last year’s present, and suggest things they might like this year. I can’t believe this one right now, but apparently Alfa Bank (Russia), CBA (Australia), Santander (Spain) and Caixa (Brazil) are already well on the road to making this happen.

#5: Distributed Payments

How about banking as a status symbol? Show off my contactless bracelet (La Caixa, Spain), biometric tracker (RBC Canada and HBOS UK), wearable suit (Heritage Bank, Australia), wearable everything (Barclays UK) and more. Hmmm … just seems to me that I can pay for something with just the flick of finger these days.

#4: Talking Transactions

We used to have boring transactional statements, but many banks are bringing transactions alive by integrating features and apps with other plug and play services, like Google Maps, Facebook and Instagram. An example of brining things to life is the Moven app, which alerts the user when they’re spending and getting above their budget limits by breaking the glass on their phone.

#3: Love those SMEs

SME – Small to Medium Enterprises or, if you prefer, small companies – have been relatively unloved by banks in the past. They are high risk until established and, even then, unless they get to a certain size – more than $100 million revenues – they can cause credit risk concerns. Those concerns can be overcome by partnering with the new mentors like Funding Circle or by doing things like the Kumsal services from Deniz Bank, Turkey. This is a platform that supports small businesses gain digital reach by offering a comprehensive suite of support from digital marketing to communications to operations to an overall online presence.

#2: Non-stop, Always On

The 24*7 bank is here, and it doesn’t cut the mustard to be 9 till 5 anymore. Equally, some banks are becoming more than just 24*7 by offshoring, with banks such as Standard Bank, South Africa, offering a single dashboard to let relationship managers connect with their clients via any media the client prefers to use including WeChat, Facebook Messenger, Google Hangouts, Whatsapp, etc.

#1: Everything is personal

I like this one as I’ve talked 1:1 Marketing since the 1990s, but it’s finally happening, with one-size fits all only applying to scarves these days. The fact is that we now have a fully enabled digital customer platform where back office cloud and analytics can deliver real-time experiences through APIs anywhere, anytime. The example EFMA chose for this category is Idea Bank, Poland, who offer an entire financial ecosystem for their clients from cloud-based internet banking to an Uber-styled ATM.

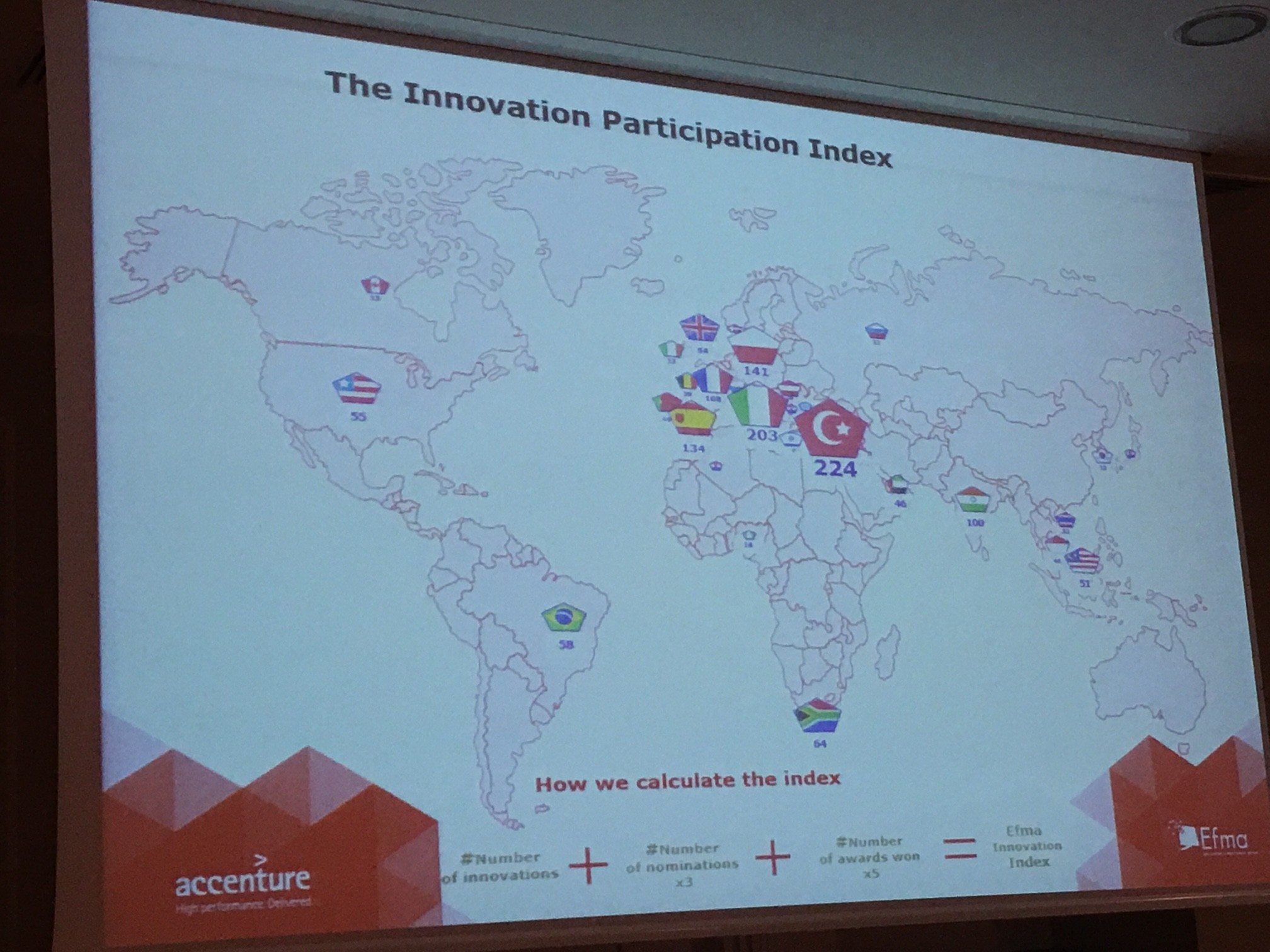

Idea Bank also won the award for best innovation at BAI Retail Delivery last year LINK and this is the most notable feature of both the EFMA and BAI Awards. Both focus upon innovation and both give the most awards to two countries: Turkey, Italy and Poland.

EFMA had 224 shortlisted innovations from Turkish banks in 2015, 203 from Italian Banks and 141 from Polish banks. A near fourth place is Spain with 134 nominations. Now you could say that this is because EFMA are European, but BAI had major placements for Turkish and Polish banks.

You may say that this is because these are the banks that enter these awards, but you would be wrong. It is because these banks are launching new, mobile first services, based upon fit for purpose back office systems implemented in the last few years. Unfortunately, most US, UK and large banks of developed economises look positively straight jacketed by comparison.

You can see more about the EFMA Innovation Awards if interested, over here.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...