I heard a rumour the other day. The rumour goes something like: are you not surprised that banks grow into big beasts, as it’s government supported? Governments want banks to be big and regulated, because governments can then access the data the bank is keeping about their clients. IT’s access to data for tracking financial flows and movements that is at the core of government interests here.

The person was alluding to a collusion between large financial firms and government snooping. The idea being that a government can spot illegal activities through the financial system. Well, of course that’s true. That’s why governments use banks as their online police.

But what happens when consumers stop banks and governments tracking them through the system in this way? This is the idea of a self-sovereign identity scheme: I own my identity, and give access when needed and explicitly permissioned.

If a bank needs to do KYC, I give permission for a validation of my name, address and nationality to the bank to my identity data – just those parts they need to access – for a period of up to 24 hours.

I have other parts of my record available forever to certain organisations, such as my medial data records are accessible when needed by any registered doctor, but only if I am present with that doctor. This would cover any medical emergency requirements.

Otherwise, you have to ask permission to access my record and I give you limited access to what is needed.

This turns things on the head: what happens when customers own their identity, and therefore their data, and organisations have to ask for access? There is no government authorise right of access. You can only access if I authorise.

This gets interesting. It gets even more interesting when you consider how data is generated and strode today. As an individual, I create huge amounts of digital information about myself. Originally, back in the 1990s, companies believed they could leverage their knowledge of customers using data warehousing techniques. The industries targeted to use those technologies were those that had high frequency of contact with the customer – banks, retailers, telco’s – and the whole idea was to get an in-depth analysis of the customer data to cross-sell and leverage knowledge of their needs and habits. This was very crude compared to today’s world where those who have the most frequent contact with the customers are the firms that never see them – namely the internet giants of GAFA (Google, Apple, Facebook and Amazon) and BAT (Baidu, Ant Financial and Tencent).

These companies interact with us many times a day in most instances, and can collect and leverage huge analytics of our digital footprints, and they do. That’s what makes them sticky. By comparison, banks, retailers and telco’s are luddites with data. As Vernon Hill, founder of Metro Bank, said in the papers this week, the “banks’ IT systems are only one step above the quill pen”.

Even with their billions being invested in digital transformation, the banks major challenge is that it is like trying to turn an elephant into a duck. It just doesn’t fit.

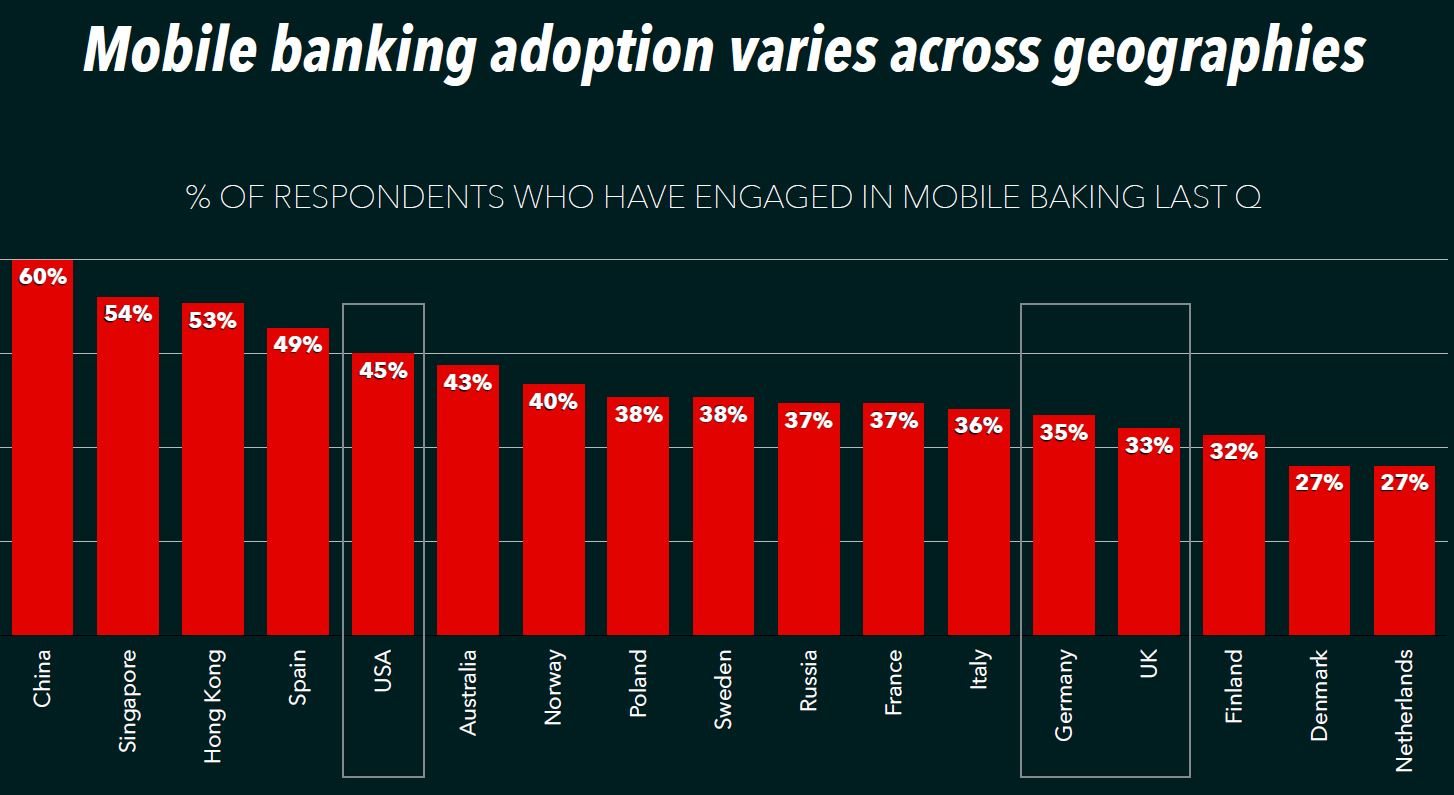

Meantime, the GAFA’s and BAT’s were built on data, and so they just get data in their bones. This has led to a really interesting new development, particularly in China. China’s consumers have embraced mobile services, so much so that they use mobile more than money.

Source: Bain & Co

This has led to a raft of new bank start-ups owned by the mobile network giants of BAT and more. Ant Financial has opened MYBank in China, and Tencent has WeBank. Baidu has Baixin Bank, a JV with CITIC. Xiaomi, one of China's biggest online smartphone sellers, bought a 30% stake in Sichuan XW Bank. Meituan.com, a website that specializes in group buying, also formed an internet bank called Jilin Yilian Bank.

It is natural if you are unshackled from history that a networked company would offer networked finance. The fact that GAFA haven’t done this is therefore surprising, or maybe not. The US banks fear GAFA and would naturally try to block them from access to their cartel-controlled marketplace by lobbying Washington. Mind you, they couldn’t do much about this if Amazon acquired a bank, could they? And this is just what was posted as a possibility by Banking Technology. It’s never going to happen in the USA though. Wal-Mart has tried to open a bank for the past quarter century and been blocked by regulators, so why would Amazon or any other commercial firm get a bank licence when everyone else has been blocked? American Banker expands on this theme further, but the bottom-line is that if banks do not leverage data to better effect, then they are leaving a wide open gap that someone’s is going to fill.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...