I’m hearing murmurs of a financial crisis rising again. It’s just rumours and gossip, but sometimes there’s no smoke without fire. My forecast for another major global financial crisis was that it wouldn’t occur until the 2040s but, as James Dimon noted, a financial crisis generally appears around every seven years. Not a big one, but a crisis nevertheless.

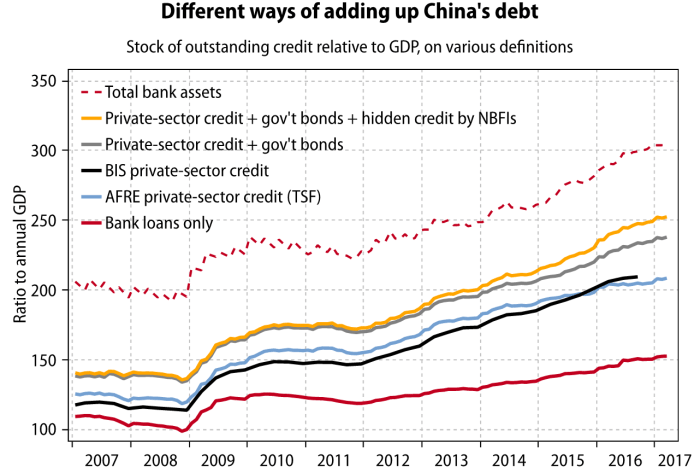

What is the rumour about this one? Well all roads seem to lead to China, and that’s where the concerns lie amongst many. The double-digit growth economy is starting to slow to a meander, and that spells trouble for all. In addition, high levels of corporate debt, a debt to gross domestic product ratio of 277% and a staggering $8.5 trillion shadow banking exposure, are all causes for concern.

Moody’s just downgraded China as a country, and there are many worried that, like Europe, it could end up in a sovereign debt crisis of just turn into a stagnating slowdown like Japan. Anatole Kaletsky, Chief Economist and Co-Chairman at Hong Kong-based Gavekal Dragonomics and an economic journalist and commentator for 30 years, including at the Financial Times, believes it’s pretty much certain that China will experience a financial crisis within the next decade. Speaking with Australia’s ABC News, he says:

“I think there is a risk, to almost near certainty, of a banking and financial crisis in China sometime in the next decade, but I think it's very unlikely to arise for the next couple of years. Debt is certainly building up in both the private and the government sector. Mortgage lending has been growing very, very rapidly over the last year to the point where Chinese household debt is getting up to the levels that we see in developed countries, in Europe. So debt levels are building up, but they are not yet at the levels that triggered crises in other open, market-oriented economies in the past.

“For the next few years, the Chinese can avert a financial crisis through the combination of fairly rapid changes in monetary policy, a great deal of direct bank regulation and credit regulation, which they still can do because so much of the banking system is state controlled, and the fact that the underlying growth of the economy remains pretty rapid because China is still developing rapidly into a modern consumer led economy.

“I think for the next two, three, perhaps five years, it's possible for the Chinese authorities to keep all these balls in the air at the same time. At some point, the juggling act will fail, because fundamentally and structurally the economy is getting weaker.”

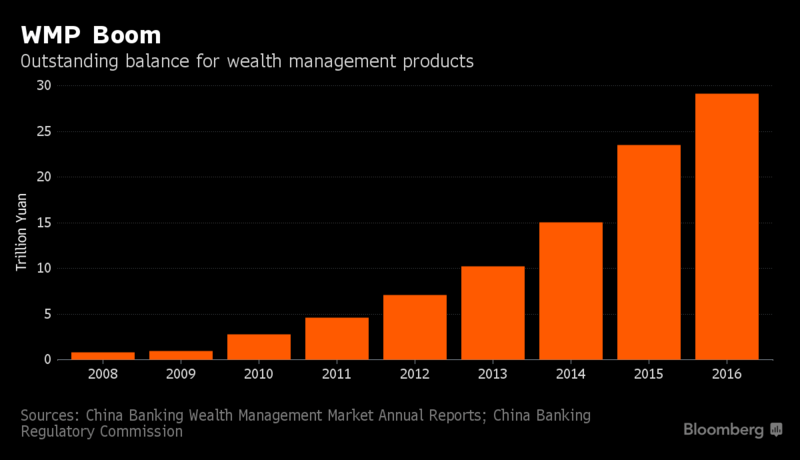

The one thing that may avert such a crisis is that China is a nation of savers with almost $9 trillion in wealth management products, most of which has been accumulated in just the last few years.

In addiotn, the state did have trillions of dollars in reserves but, unforuntlaty, those reserves are dwindling due to the stagnating economy and the need to prop up the failing Yuan exchange rates.

What’s the most likely outcome?

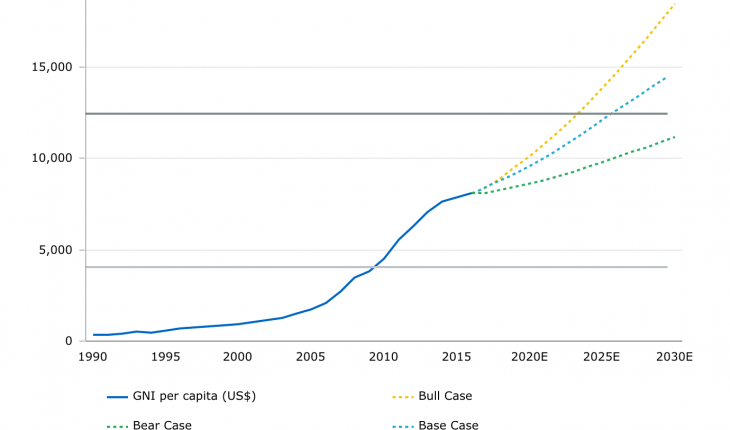

Morgan Stanley has a published a paper called “Why We Are Bullish on China.” The report makes the most cogent version of the bull case for China and predicts that average GDP growth rates over the next ten years will exceed 5%, turning China into a high-income country by 2027.

Morgan Stanley forecasts that “China will break out of the middle-income trap and join the rarefied ranks of high-income society” with per capita income of above $12,500 by 2027.

China’s economy would then be about US$17.5 trillion, close to the level of the US economy.

Chetan Ahya, Morgan Stanley’s Co-Head of Global Economics and Chief Asia Economist, believes that China can avoid the worst scenarios of a crisis based upon three major factors:

- China’s own savings have funded its build-up in debt, which has gone into investment, rather than consumption;

- The government enjoys strong net asset positions both domestically and externally. Both provide adequate buffers against shocks; and

- Strong external macro positions, including a current account surplus, high levels of foreign currency reserves, and lack of significant inflationary pressures, leave China with plenty of leeway to manage domestic liquidity conditions.

That said, “China has borrowed a lot from the future, and the payback will be in the form of a significant slowdown in growth rates,” Ahya says.

All in all, the future is uncertain for China but, at the very least, if the economy does hit the fan, be prepared and maybe that’s why so much has been invested in bitcoin and cryptocurrencies in Asia of recent days. Be prepared.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...