Wrapping up thoughts on #Money2020, the Vegas show is by far the biggest of this monster event organising company. I’m guessing there were around 15,000 folks there this year, and everything but everything was being covered: AI, machine learning, mobile wallets, core banking, distributed ledger, blockchain, cryptocurrencies and just about every other aspect of making and taking payments.

Usually the keynotes on the plenary stage don’t impress me much, as they’re just product pitches, but a few did stand out this year. I was particularly impressed by the content of Oliver Jenkyn’s presentation. Oliver is EVP & Group Executive, North America for Visa and I usually hate Visa’s content. But Oliver began by talking about a messaging conversation he had with his ten-year-old daughter that finished with her asking:

“What will you do that will make a difference in the future?”

Good question, and one that I ask myself every day.

Oliver then related it to the fact that “there is more change in the next two years in payments than in the last ten”, and dived into how the Internet of Things or, as Samsung talks about it, the Intelligence of Things will change everything.

There will be a ten-fold increase in devices and volumes of transactions he claimed. Jenkyn’s noted that it took sixty years to rollout three billion cards and equip 44 million merchants to take card payments. In the next five years there will be thirty billion ways to pay and 440 million places to buy, thanks to your car, home and clothes being internet-enabled.

This is why Visa is changing. For sixty years, Visa has been developing within a closed architecture based upon Visa’s ideas with Visa’s technologies. That no longer works as it’s too slow and stifles truly innovative thinking. This is why Visa is opening up and now has API’s (Application Program Interfaces) and SDK’s (Software Developer Kits) to enable co-creation. The aim is that this will turbo-charge speed-to-market, lower costs and enable everyone to innovate for real-time access to the payments network.

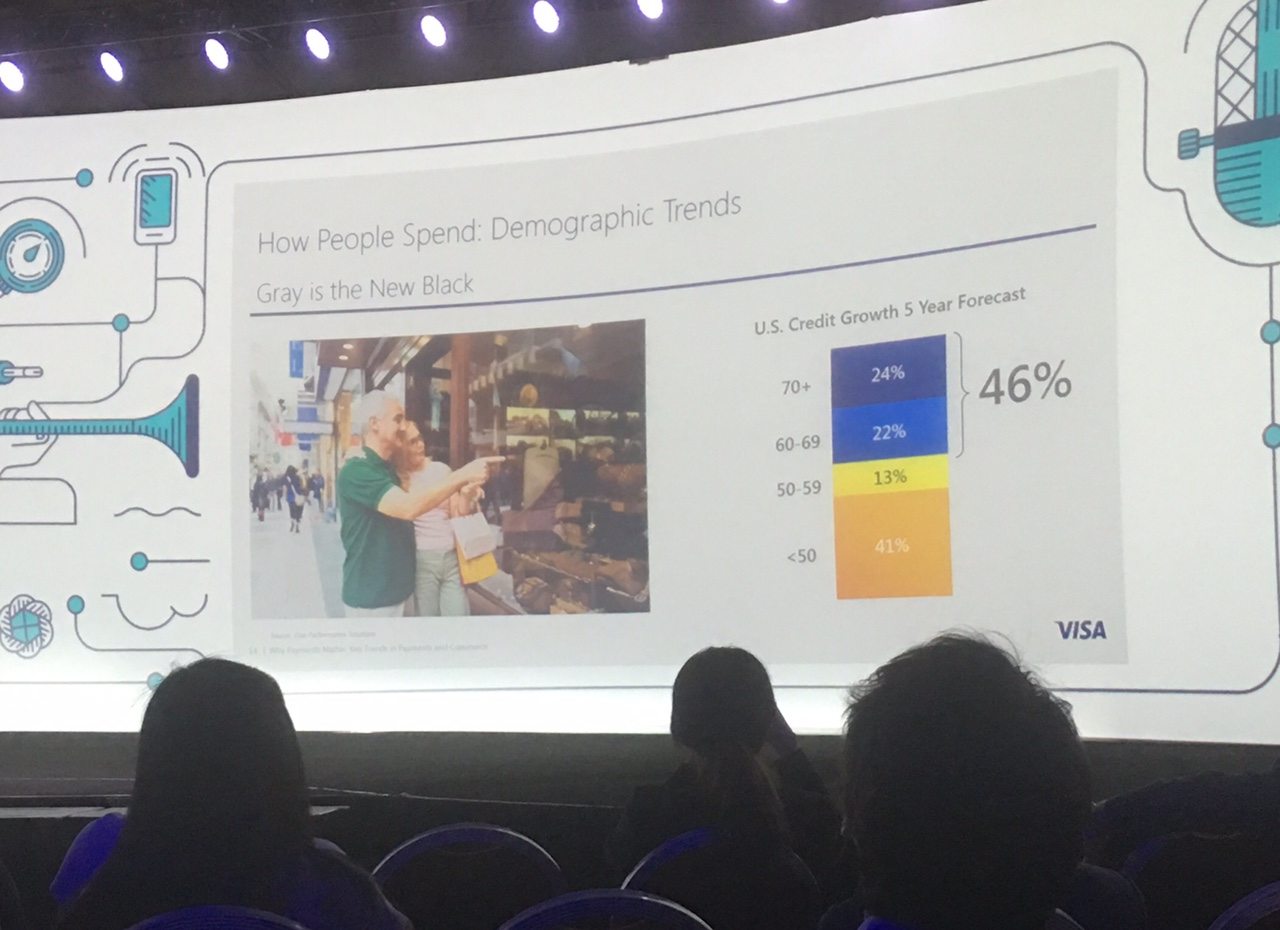

The stand-out part was talking about demographics however. It surprised me a lot that Visa see half of all credit growth over the next five years in the USA coming from the over 60’s.

In fact, a lot of talk this week has been about how young millennials prefer to avoid debt, save and use prepaid. Meanwhile, their parents are loading up on easy access to credit. I’m not sure if that’s meant to imply that the grey-haired customers in developed markets are thinking:

“You know what, we screwed the planet with fossil fuels, made a fortune from land and property, and can now blow the whole lot on having a good time before we leave this fertile Earth.”

In other words

Screw the kids!

Or something else, but it certainly seems to imply it.

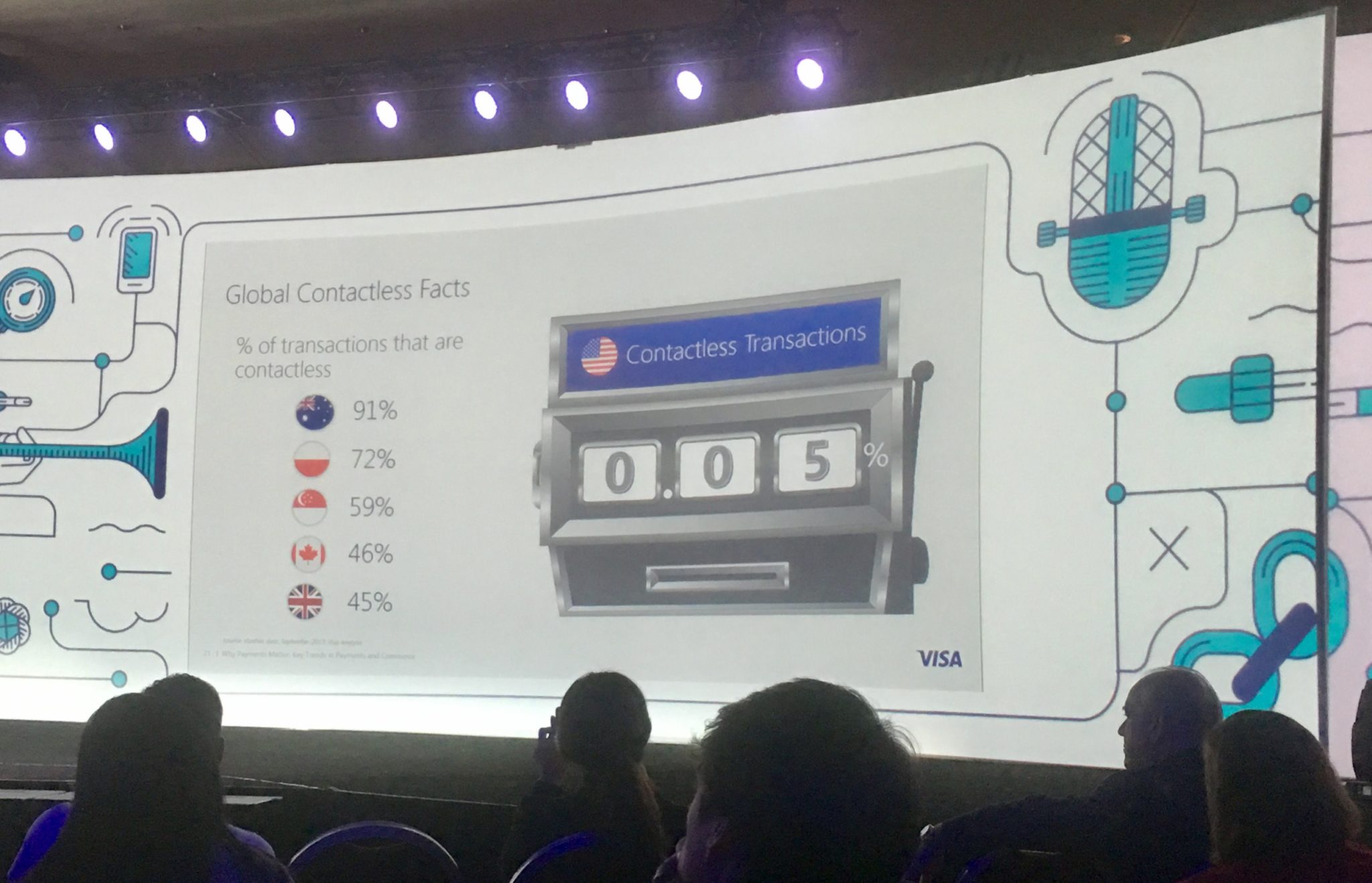

Then Oliver put up his final slide that was also a shocker. Certain markets like Australia and Poland are leading markets for contactless payments, with 91% and 72% of all transactions made via tap and pay on the terminal. Even little old Blighty gets a shout-out with 45% of transactions now made via contactless payments. But in the big and bold USA, that figure nosedives to just 0.05% of transactions today.

Wow!

No wonder Ali Paterson’s payments race – a challenge to get from Toronto’s Sibos to Vegas’s Money2020 using just one payments service – found the contactless guys came last!

What is surprising is that it’s just 0.05% of transactions, even though 40% of terminals can take a contactless payment. It just goes to show that like weaning Americans off magnetic stripe and paper checks, the customers and merchants need some education.

Another presentation that was a good one came from Abra. Abra is a bitcoin based payments wallet that allows monetary transfers from Texas to Timbuktu in near real-time for almost free. I really like what they’re doing, and have picked them out before as one of my standout start-ups in blockchain use cases.

Bill Barhydt, Abra’s founder, started with positioning bitcoin itself. According to PYMNTS.com’s Karen Webster: “bitcoin has only two proven use cases after eight years: criminal activity and speculation”, Bill quoted. Following that with the quote from Robert Metcalfe – he who co-invented Ethernet – saying that he predicted “the internet will soon go spectacularly supernova and in 1996 catastrophically collapse” back in the early 1990s. Yep. Never make predictions, especially about the future.

In fact, a lot of people in the blockchain world are likening today with bitcoin as being like the internet before Tim Berners-Lee, and they’re right. We are in the pre-worldwide web phase of online payments, and things are changing rapidly.

I can’t finish this section off without a shout to my friends Brett King and David Birch who starred on stage, alongside Steve Ellis of Wells Fargo, debating about the role banks would have in our world of money in a decade. Brett proposed that their importance would be diminished; Steve argued it would be just as important to have banks in banking. I had to leave before the end, but would personally say that banks will not disappear, but need to adapt. Like any major industry shift – and this is one as demonstrated by Abra’s comments – there is a significant change to industry. Bill Barhydt predicts that banking and money will be impacted as much by bitcoin and blockchain as retail, entertainment and other industries have been by the internet.

I agree with him and always hark back to Charles Darwin on this one:

“It is not the most intellectual of the species that survives; it is not the strongest that survives; but the species that survives is the one that is able to adapt to and to adjust best to the changing environment in which it finds itself.”

This is the key and the banks that haven’t addressed their ticking time bomb of rotten core systems will be the ones that go the way of Kodak, Nokia, Blockbuster, Tower Records et al.

There were lots of other great moments during the week I’ve been here in Vegas, not least the touching t-shirts with #VegasStrong on them. It’s only a few weeks since the terrible shootings took place at the Mandalay Bay and most live acts in the evenings made some reference to the impact this has had. IMHO, it is a terrible, terrible thing but, like the Bataclan nightclub shootings in Paris, it’s a one-off and no reason to abandon a place that, other than that one incident, is safe, safe, safe.

Ah well, it’s now time to head home and indulge in a short weekend before coming back over here (Dallas) for a keynote alongside George W. Bush next week. The world moves on and you many of us reflect that George W. seemed pretty stupid back in the day, until you see who is in the Oval Office today. Anyways, better not go there as that could stir up a little hornet's nest.

Talk more next week …

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...