A last post about financial inclusion and banking. I pondered the thought of how people who get inclusion will gradually rise and upscale to full service banking. I see it almost as a ladder of steps from exclusion to banked as follows:

Step One: Financially Excluded (Hawala)

These are people who have no access to technology, the network or the bank. They fear banks typically, as the banking halls are for people in suits and very formal and deal much more comfortably with friends and family through hawala. Hawala is a traditional system used by many people in countries where the majority of the population are unbanked. It allows money to be paid to an agent, who then instructs an associate in the place you are sending money to pay the final recipient. Since the crackdown after 9/11 on terrorism, with hawala seen as a major part of this, there has actually been an opposite effect. For example, Somalia’s formal banking system broke down and now the hawala network handles around $1.6 billion in informal money transfers each year. In fact, according to the CIA’s World Factbook, Somalia’s economy pretty much depends upon the value transfers of livestock, remittances and money transfers and mobile telecommunications.

Step Two: Financially Included (Mobile Pay)

The first level of inclusion is the offer of basic payment services through a mobile telephone. This is not a mobile wallet, but just a USSD text messaging payment service. I was delighted to meet Kamal Budhabhatti, founder and CEO of Nairobi-based Craft Silicon at Dot Finance, and he taught me something I didn’t know (always a good thing): Craft Silicon are destined to be Africa’s first billion-dollar company. The company white labels their software to MNOs to provide USSD text payments, and handled USD$5.5 billion worth of such payments in 2017, a rise of 25% over 2016’s $4.4 billion. They can even find your location through USSD, a world first, and a significant step forward in enabling mobile payments across Africa. Mind you, that volume of payments is not all in Africa as Statista estimates:

- Total Transaction Value in the "Digital Payments" segment amounts to US$46,364m in 2018.

- Total Transaction Value is expected to show an annual growth rate (CAGR 2018-2022) of 14.0 % resulting in the total amount of US$78,368m in 2022.

- The market's largest segment is the segment Digital Commerce with a total transaction value of US$42,588m in 2018.

In this area, Zimbabwe stands out, where the Governor of the Reserve Bank of Zimbabwe John Mangudya, states that: “more than 96% of the USD$97.5 billion processed in the entire country in 2017 were through electronic and mobile banking systems”, and that “mobile payments constituted the bulk of payment streams in volume terms.” This system is driven by EcoCash. With a staggering 97.98% of market share for subscribers, the mobile money solution has cemented themselves as the dominant player of mobile money in Zimbabwe.

Step Three: Financially Served (Microfinance)

Once you get used to mobile payments, the MNO and microfinancing firms can start to leverage service. Microsavings, microinvesting, microinsurance and microlending are all growing in Africa and, as I said yesterday, it is like pouring water on stony ground. Plants and new life grow fast. In this case, micro, small and medium enterprises (MMSMEs) and new business.

I chaired another panel at Dot Finance with two hugely engaging characters: Sharon Arungu-Olende, Head of East Africa for Lendable, and Viola Llewellyn, CEO of Ovamba. Our focus was a discussion of MMSMEs and the fact that banks just don’t care about them. Sharon made the point that she was looking after trade finance for a very large bank in Kenya before moving to Lendable, and her job was to wine and dine her clients and get to know their businesses well. She had 20 clients, including firms such as Kenya airlines. A bank just could not justify having someone like her doing the same role for 2,000 small clients. So, they just ignored them.

That’s all changing with FinTech. Lendable now provide the data analytics on the credit risk of MSMEs in Africa; Ovamba then provide the liquidity to lend to those businesses, based upon data from Lendable and other sources. Ovamba are all about risk, not lending, as Viola pointed out. A bank is concerned about lending to an MSME in case they default. Ovamba is all about lending to an MSME and, if they default, help them start again. It’s a very different outlook.

However, there is still a massive gap between access to funding for MSMEs and funding available. In 2013, the IFC estimated the developing world funding gap for MSMEs between formal and informal financial systems to be $2.1 trillion - $2.6 trillion. That gap is being bridged through the new mobile money corridors, as the volume of digital transactions is enabling the capture and analysis of payments data at a level never seen before in informal businesses. This has led to the rise of many alternative lenders including d.light, Watu Credit, M-KOPA Solar, Ovamba, PEG Ghana, Raj Ushanga House, SunCulture, and Tugende. They are all using this convergence of technology to reach more customers and lower the cost of servicing them, with the market for East African alternative lenders expected to reach $15 billion by 2020, according to Daniel Goldfarb, CEO of Lendable.

Interestingly, Ovamba’s business model is slightly different. As mentioned, they focus on risk and so they don’t actually lend to MSMEs. They buy. Ovamba holds the assets that MSMEs sell, and then deliver them on demand. This model works, and is targeted at the 84% of African MSMEs who have little or no access to capital, leaving a $368 Billion Gap in financial needs.

What Ovamba does is underwrites and pre-funds every transaction and take ownership in full of assets, instead of taking a mortgage or lien. Enforcement in case of non-payments is therefore simplified. All transactions are executed at rates of 66% of the value of the liquidation value of the goods – providing significant security for investors (who have earned double digit Euro returns transactions).

Amazing business and no wonder Africa is becoming one of the hottest regions in the world for start-ups.

Step Four: Basic Banking (Deposit Account)

At some point, these start-ups may want to get a bank account. I guess they’d do that because they’re growing up and want to do more complex things. Viola pointed out that Ovamba would be happy to work with the banks, but many aren’t interested and, if they cannot find a bank partner, then they would be providing these basic banking services themselves. As she put it: “work with us or we will eat your lunch”. She’s very meek and humble.

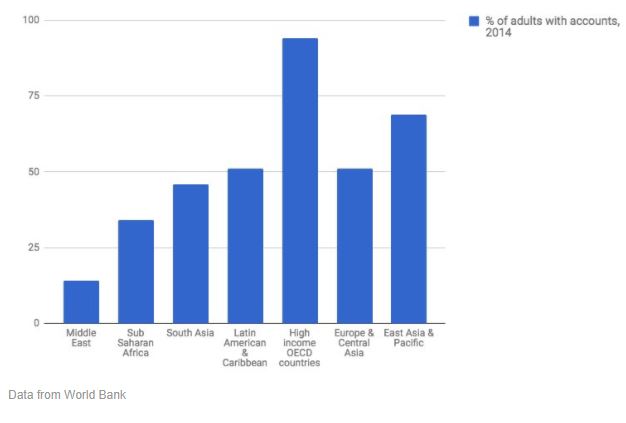

However, in many countries in Africa, people find it difficult to get a bank account because they just don’t have enough money. That will change as it is quite clear that once you can get access to funding via FinTech and mobile, you can become more entrepreneurial. Today, a third of Africans have a bank account.

Source: Business Insider

Tomorrow, most Africans will have a bank account. It just won’t be called a bank account. It will be a hybrid between a basic bank account provided through a mobile service and a mobile wallet. I think the best example of this is Kenya’s banks response to M-Pesa. First, they tried to block the mobile service through the regulator and, when that failed, they launched competitive products.

The banks came together and launched the Integrated Payment Services Limited, also known as Pesalink. Kenyan banks chose to cannibalize their over-the-counter cheque and electronic money transfer services. Pesalink allows partnering banks to offer these services through USSD or mobile banking apps.

The banks then integrated Pesalink into their banking apps and USSD services and, not to be caught out, the mobile network operators reached an agreement that mobile users should no longer experience differences in costs while moving money across networks. The result is that the monopoly M-Pesa had for mobile money – 90% of the market in Kenya in 2015 – was impacted heavily by Equitel, who took 22% of that market in just one year.

Of all the Kenyan banks leading the charge against M-Pesa is Equity Bank, a bank started in 1984 to serve the needs of the lowest-income customers in Kenya. Equity Bank launched products to rival M-Pesa back in 2014, and even announced their own MNO, Equitel. M-Pesa claim the bank just copies what they do, but they copy it very well. A great example is their mobile app where the bank has integrated Pesalink with their SIM menu, which they can as they own an MNO, Equitel. Pesalink integration has encouraged many Kenyans to switch accounts. Posting their Q3 2017 results, this paragraph says it all for me:

“The Group’s innovation and digitization strategy led to 91% of all transactions moving from the fixed cost delivery channels of brick and mortar of bank branches and ATMs to variable cost delivery channels of mobile, internet, mobile App, Agency and merchant banking. Of the total 341.3 million monetary transactions, only 30.3 million transactions passed through the branches and ATMs with the rest, 311 million transactions passing through the third-party channels. This shift in delivery channels resulted in a reduction of 11% in staff costs while registering a modest increase of 2% in total costs maintaining a cost income ratio of 51.6% at the Group despite the 15% reduction in Net Interest Income. Digitization saw an increase in remittances by 54%. Mobile innovation Equitel helped the Group capture 25.6% of the value of national money transfer in Kenya and 33% of the national market share of Mobile Commerce.”

Step Five: Full Banking (Loans, Mortgages, FX, etc)

I guess where I see things developing over time is that you won’t tell the difference between a bank and telecommunications firms, except by the sophistication of their banking products. When in Rwanda last year, I always remember our taxi driver saying that he used the mobile money services for paying for things generally but, when it came to complex services like moving money abroad or getting a mortgage, he would talk to the bank. Equally, for larger businesses, banks would still want their relationship managers like Sharon to talk through their structured finance products and trade finance needs.

The end result is that I think for the two-thirds of Africans who are unbanked or underbanked or, as I prefer to put it, unserved or underserved, they will grow through the mobile money and microfinance system into astute business owners with their basic financial needs fully met by the MNOs. Some of those MNOs will work with banks to provide their product needs: remittances, FX, loans and savings; whilst some of those MNOs might be operated by a bank, such as Equitel.

Only a small percentage of Africans will rise to needing full banking services and, for most of those people today, they are the ones who already have bank accounts and are unlikely to give those up to use an MNO instead. However, for most of the basic needs – payments – all Africans will use mobile, as it is too easy and compelling a service to ignore.

As you can see, when I say look to Africa for true innovation, you can see what I mean just from this small write up. More to come later, I’m sure.

Finally, if you want to know the real situation of mobile money in Africa, have a look at this GSMA Intelligence report:

At the end of 2016, there were 420 million unique mobile subscribers in Sub-Saharan Africa, equivalent to a penetration rate of 43%. The region continues to grow faster than any other region; the CAGR of 6.1% over the five years to 2020 is around 50% higher than the global average. The region will have more than half a billion unique mobile subscribers by 2020, by which time around half the population will subscribe to a mobile service. The total number of SIM connections in the region reached 731 million at the end of 2016, and will rise to nearly 1 billion by 2020.

Less than a fifth of under-16-year-olds (who account for more than 40% of the population in most countries in the region) have a mobile subscription, while women were 17% less likely than men to own a mobile phone in 2016. The uptake of mobile services by these underserved groups will, in large part, drive subscriber growth in the future. Four of the most populated markets in the region – DRC, Ethiopia, Nigeria and Tanzania – will account for nearly half the 115 million new subscribers expected by 2020.

In 2016, mobile technologies and services generated $110 billion of economic value in Sub-Saharan Africa, equivalent to 7.7% of GDP. Mobile’s contribution to GDP is expected to rise to $142 billion, equivalent to 8.6% of GDP, by 2020 as countries benefit from improvements in productivity and efficiency brought about by increased take-up of mobile services. The mobile ecosystem also supported approximately 3.5 million jobs in Sub-Saharan Africa in 2016. In addition to the mobile sector’s impact on the economy and labour market, it makes a substantial contribution to the funding of the public sector, with $13 billion raised in 2016 in the form of taxation

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...