A new study of the 50 largest banking groups in the UK and Europe has revealed that although profits have increased, future profitability is at significant risk.

The UK & European Banking Study (EBS), shows that banks are operating in unstable market conditions fuelled by unsustainable profit-taking, crisis level valuations and dwindling market share.

While profitability (Return-on-Equity, RoE) improved throughout 2017 (from 3.9% to 7.1%), the report states that it is highly unlikely for banks to continue repeat these gains going forward. Profit improvements from reduced non-litigation and extraordinary costs have allowed net profits to surge, but it’s hiding the fact that maintaining sustainable recurring profits will be nearly impossible.

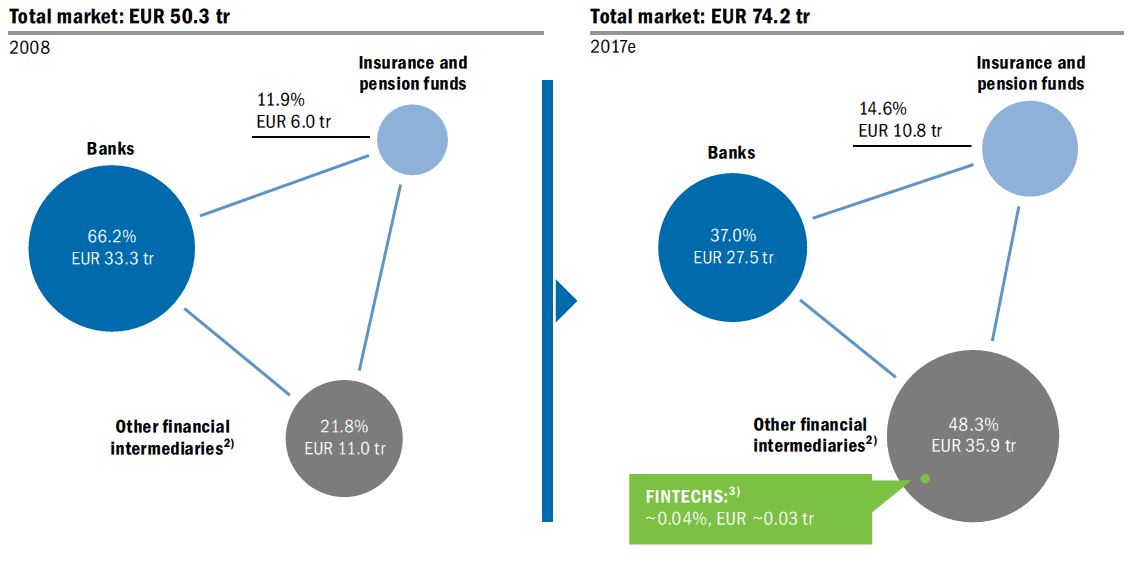

Banks are also losing market share to other financial intermediaries including shadow banks and non-banks. These intermediaries now hold almost half of the assets in the European financial sector moving from 22% in 2008 to 48% in 2017. Add-in insurers and pension funds, and this grip on what were bank assets increases to 63%, according to the study.

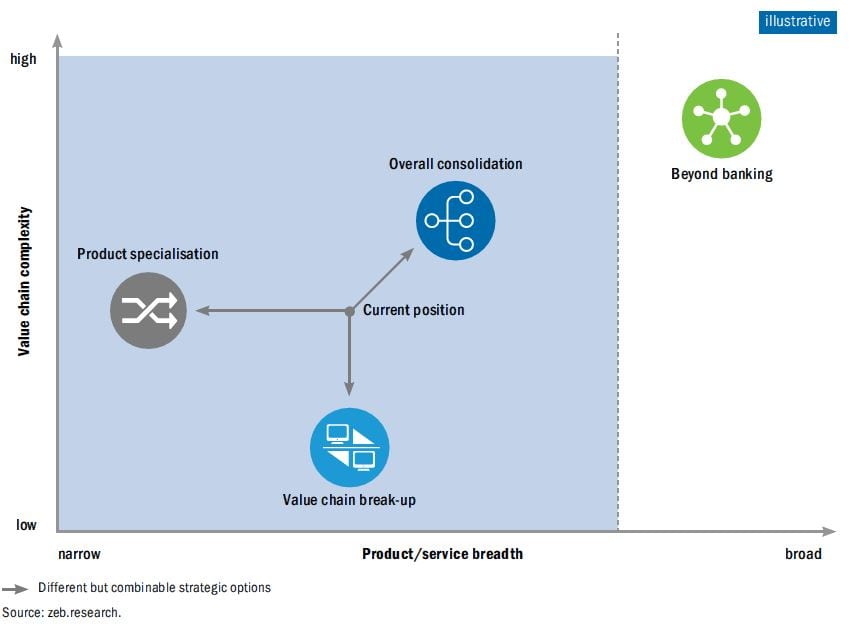

The study outlines four strategic options banks can choose to combat market conditions and produce value with true differentiation. They include: pursuing M&A, focusing on product specialisation, breaking up the value chain and participating in financial ecosystems or platforms.

Having read the report briefly, I liked some of the clear positions taken. For example, it is clear that market share and margins for banks offering traditional financial services are shrinking.

It is also clear that banks need to take a position. Strategically, they need to either be a marketplace, a specialist, an acquirer or a curator.

And it is clear that some banks GET IT, and are doing something about it.

But the final paragraph of the report is the one that resonated with me most:

“In our conversations with industry insiders, as few as one in five feel that their bank has made significant progress towards their target state. As one executive put it, they are waiting to see “Who will blink first?”, knowing they have to change, but lacking a clear vision of what they will change into.

“This approach risks ignoring the strategic threats: market share already reducing because of disintermediation, new market entrants challenging traditional models, and non-European rivals eyeing the European retail banking market.

“Even if banks return to adequate profitability it will be at the further cost of market share unless they update their strategies to meet the future of the industry. This calls for clarity over their own position and that of their competitors, an understanding of the strategic options available and the most likely industry trends. At this tipping point, banks must take decisive action to successfully navigate the road ahead or risk decline and irrelevance.”

Yep.

About the UK & European Banking Study:

The study is the produced by zeb, a strategy and management consultancy in financial services. This year’s report ranks every top 50 European bank, based on analysis of capitalisation, total assets and return on equity. The study shows why recent profitability improvements may be short-term and how market shares are under attack.

To learn more and obtain a copy of the new report, please visit https:// zeb.eu/ebs18.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...