So my snarky little friend Ron Shevlin wrote a piece on Forbes claiming that Americans don’t want a digital bank. As the guy who wrote the book Digital Bank you might think I would take offence to such a statement, but no. I agree with his content, just not his headline. His content states:

10 years after the launch of neobanks in the US, just 3% of Millennials have their primary checking account at a digital bank … that percentage drops to 1.5% of Gen Xers, and 0.8% of Baby Boomers …

In contrast, more than four in 10 Millennials have their primary checking accounts at just three banks--Bank of America, JPMorgan Chase, and Wells Fargo … and a third of Gen Xers and Baby Boomers still keep their primary checking account at those three megabanks.

Ron is using a survey of US consumers performed by his firm Cornerstone Advisors, and goes on to say that consumers don't want a digital bank but that digital transformation is critical. This is why I agree with him. It’s nothing to do with giving the customer digital banking. It’s far more to do with giving the customer banking in a digital way.

“If there's anyone who you would think would be banking with a credit union, it's (my millennial daughter). But she doesn't--she banks with Chase. When I asked her why she said ‘Best mobile tools, Dad.’”

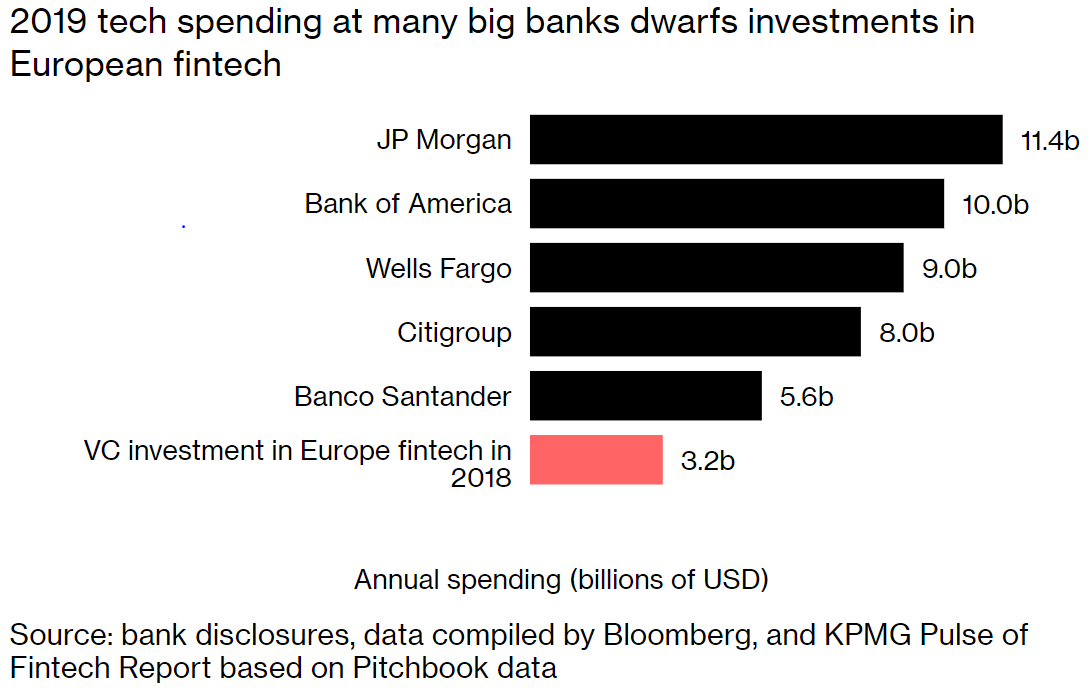

I agree with this, which is why traditional banks are throwing billions at trying to be transformed to digital, according to Bloomberg. The article notes that most big banks are spending more on digital than the total investment in all the FinTech start-ups:

It also notes that a lot of that investment is trying to manage a creaking ship rather than spinning innovation the way challenger banks are. I always remember the comment Anne Boden, founder of Starling Bank, made at one conference which is that she was achieving with $3 million and 100 people what would have cost $3 billion and 10,000 people in the old bank … or something along those lines, and it’s true. It’s hard to turn around a big engine old bank/

However, traditional banks fall into two main categories:

- those that are truly transforming to be digital;

- those who are talking about transforming to be digital, but are not.

The ones that are truly transforming to be digital include JP Morgan Chase who sent out a really interesting press release last year: This $11 Billion Tech Investment Could Disrupt Banking.

It begins:

There are two kinds of corporations emerging from today’s technology revolution: the disrupted and the disruptor. JPMorgan Chase is in the midst of a once-in-a-generation transformation into the latter.

Interestingly when I first cited this article, the sub-heading was that JPMorgan Chase has more technologists than Facebook and Twitter combined. Of JPMorgan Chase’s 165,000 staff (as of October 2018), 50,000 were technologists which equates to a third of the human army. That presents a slight issue in that why have more people in tech than Facebook and Twitter combined? Maybe that’s why they took that line out, as the answer is for control.

JPMorgan Chase is slowly changing the culture but, when you’re used to developing everything yourselves, it’s hard to transform into a curating partner of FinTech firms rather than a controlling copier of what they’re doing. It’s even harder to convince the 50,000 people involved in copying everyone to stop doing it and partner. After all, that would mean most of them would lose their jobs. Tough. It’s going to happen.

That’s why I place JPMorgan Chase in the firm transformational camp. They are transforming the bank slowly but surely. Two years ago, they had 235,000 people (October 2016); two years later, they increased the bank’s valuation by 50% whilst reducing staff by a third (October 2018); it would not surprise me if their value increase another 50% or more by October 2020, whilst staff would be down by another 25,000 or more, mainly from IT and technology roles no longer needed due to partnering and curating.

Meantime, the announcement that Santander are investing €20 billion in digital transformation over the next four years doesn’t cut it for me. Are they investing in digital projects or real organisational change? Are they in camp one or camp two? Are they talking the talk or walking the walk?

Banks that are truly digital have completely restructured and realigned their organisation, products and services around a digital foundation completely focused on the customer. Core systems have been refreshed and renewed, data has moved to the cloud and the IT function no longer exists. This is because technology is the business, it is no longer a function.

Does that sound like your bank? It will be interesting to see but, as Ron says, it’s nothing to do with customers wanting a digital bank. What they want is a bank that behaves in a digital way.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...