These are extraordinary times. No one can remember anything like this, except maybe those over the age of 80. The last time anything like today’s world happened was the Second World War but, as I said the other day, they were fighting each other. We are fighting a thing.

The world has stopped.

What’s interesting in this moment of time is that money is a big worry for everyone. Everyone is asking questions about paying their bills. How do I pay the mortgage, the rent? How do I keep my house, my home?

These are fundamentals for all of us, and most governments have stepped up to the plate and said we’re here to help. You can cancel your mortgage payments, we will guarantee your earnings, you don’t need to worry. Just stay at home, self isolate, don’t go out, do what we ask.

Extraordinary times.

I must admit it did make me laugh when I saw this the other day:

As humans, we lean towards making light of darkness. This is a dark time. We are all being forced to stay home. 1 in 4 humans are locked in their homes right now, and have been told to not leave. Not go out. Stay home.

What’s amazing here is that many people don’t like it, but why? Worries about money? Worries about your job? Of course, yes. But there will be an end to this. Things will get back to normal. Tings will be ok. Sometime. Sometime soon, we hope.

What amazes me is that multi-trillion dollar budgets being rolled out by big governments everywhere. $2 trillion in the USA; $500 billion in the UK; €750 billion from the ECB; and more. Where is it coming from though? Is this quantitative easing gone rogue?

I have no answer, but luckily some clever people do. My favourite analysis came from Ben Chu, Economics Editor of The Independent, and so I’m sharing that here:

The Chancellor’s £330bn of loan guarantees are a contingent liability for the UK state. If the loans made by banks to suffering private companies are not repaid the state will have to compensate the commercial lenders.

What does count as direct government spending are the grants which are to be made available to smaller firms.

According to the Treasury these grants – along with the forgone tax revenues due to the business rates holiday – will add up to £32bn this year, or 1.6 per cent of GDP.

So the government isn’t actually providing as much support as it claims?

If take-up of the loan guarantees from firms is not high then this will be the case.

Yet the government is still working on its fiscal response.

There are likely to be more tax cuts and spending commitments for businesses in the coming days. Individuals are also likely to be targeted with support.

Fiscal spending seems likely to be go higher than £32bn in 2020.

Some economists say that government borrowing could even shoot up as high as it did in wartime.

During the two conflicts of the 20th century borrowing was more than 20 per cent of GDP.

That would be double the borrowing at the peak of the 2007-09 financial crisis.

How will the government pay for all this spending?

By borrowing. Raising taxes to pay for it would defeat the object of the support by sucking spending power out of the economy.

The government will issue more debt to the financial markets.

Will the markets lend the money?

Almost certainly.

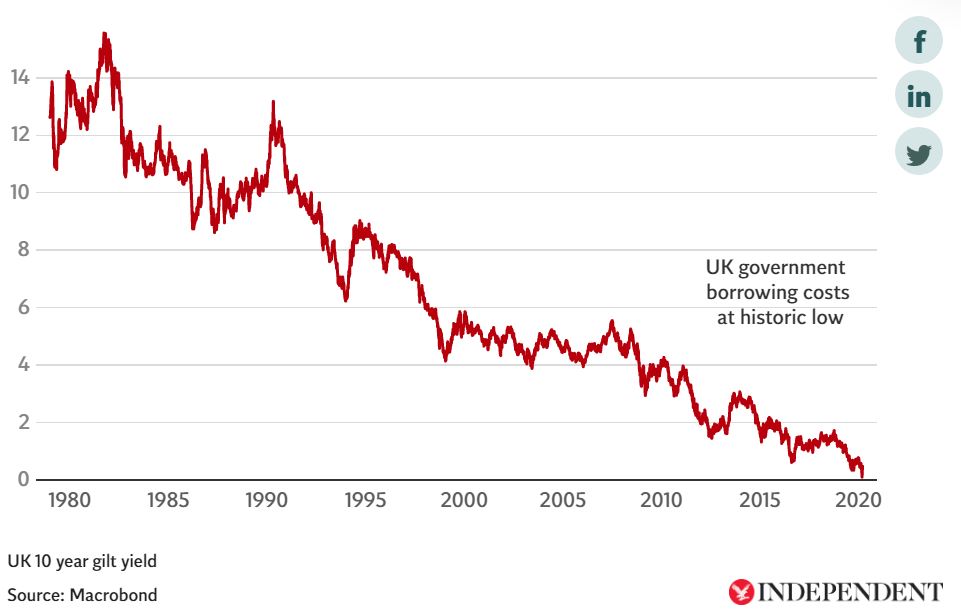

Indeed, the UK government’s cost of borrowing on the financial markets has collapsed to historic lows, a reflection of investors’ strong appetite for financial assets traditionally regarded as safe.

In theory it’s possible that markets would not buy the new debt issued by the government – or charge a punitive interest rate to do so – but analysts think that is very unlikely to happen.

The issue is that this is fine for America and Britain, but what about poorer countries? The rich can cover the exposures of a global pandemic but poor countries? Well, right now, they’re screwed. Let’s see what happens …

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...