Making a statement

I was intrigued by a news headline that Lloyds Bank is turning bank statements into art.

Sounds ridiculous? Who gets a bank statement anymore? We use an app. But then I read the piece and was more intrigued as yes, it’s been created with an artist. The artist is Paula Zuccotti, who I only just discovered.

Interestingly she describes herself as an artist and ethnographer, and has several projects related to the way we live and finance. Two projects in particular caught my eye: the one with Lloyds Banking Group, called Making a Statement, and another with Finastra about financial empowerment.

The first idea was to take people’s transactions over a month and visualise them, but not in a PFM way. In a real way.

OMG! I love this. Here’s what you’ve been spending your money on. In a truly visualised way. It’s really good!

This is what banks need to add to their apps … so simple, but so cool. Paula! Amazing!

Then I discovered she did another project with Finastra. This is all about financial empowerment and has an interesting angle too:

Paula Zuccotti spent time with the individuals, with the aim of understanding the research subject from their point of view. Unlike focus groups or quantitative research, ethnographic studies are designed to build a deeper understanding of how the participants think and make sense of the subject under discussion. In her role, Paula took care not to make judgments about how participants respond, but to get a clear response that is not distorted by their own views.

Interesting. What did she find out?

Personalisation is at the heart of what people want: banking done “my way”. My way, within my limits and according to my timings. The bank’s role is to provide the knowledge, tools and the means to help people feel in control and at the centre of their financial life.

Personalisation. Something we’ve been banging on about for years, but what does it really mean?

To find out I reached out to Paula, and she kindly agreed to have a chat. Here’s what she said:

Chris Skinner: How do you see ethnography applied to banking?

Paula Zuccotti: The key thing to ethnology is how people make sense. It’s not about making sense of other people it’s about making sense of how other people’s sense. I mean the world of banking is so relevant because, particularly with the rise of fintech and non-banking, is that the banking industry talks to the consumer from the banking point of view. They always teach benefits to the consumer with a banking mentality. When you start the conversation with the consumer, and not thinking about the bank for the moment, but talking about their finances and their financial well-being, and what matters to them the most. The bank should really be understanding their worries and, particularly during COVID19, their financial situations. People are losing jobs, so this is a good time to get closer to people, closer to customers, and actually hear their voices, being able to translate a conversation to something that is meaningful and actionable for banks to turn into a conversation that way.

CS: Most people are very uncomfortable about money. I’ve seen some ways that people try and work around that, but I’ve not seen that many good ones. Have you seen any good ones?

PZ: Yes, I think we put money and finance together like they are the same thing, but if you take money out of the equation, you get a different view. You really should start by simply asking people: What are your hopes and fears? How did you cope with COVID and the pandemic? How do you find yourself today? What’s worrying you right now? You get a very different answer. You start to get an understanding of how the customer thinks. Then the conversation comes from a different place than talking money with people who might feel obliged to discuss how much money they have or how much money they spend. That’s not the kind of conversation I want to have with them. I want to understand how they feel about their finance, and what role institutions like banks could play in empowering them in other ways than just talking numbers of money specifically. So it could be about empowering them in their lives or how they connect or how they deal with each other in their communities or around where they live. The key is to approach this from another point of view.

CS: In the Finastra report it says that your role was to listen and not to make any judgement but did anything really surprise you. Did any behaviours make you go ‘wow’?

PZ: People behave according to the culture that they live in. Therefore, you not only need to understand them but also understand them within the context of their culture. The way people go about their finance in Africa is different to how they deal with money in America or Middle East or Asia. We could look at the proliferation of e-wallets and all the conversation based around sending and receiving loyalty points. In some cases, like in APAC, this completely deviated from the focus on healthy financial well-being. It was not about helping people with their finances but more ot do with promoting the idea that if you use the e-wallet to pay now, then you can get something for free. It surprised me how people want to change the way they were spending using an e-wallet instead of cash and, in America , we had conversations about people using the different loyalty points and facilities and opening 10 or 20 bank accounts moving money here and there all the time. It was like trying to play a game of shifting spending and savings to get the best return. It became a game of chasing that level of banking management, with consumers having to juggle ten or more bank accounts. So a lot of things surprised me from what I found and where I’m looking at, as it’s different from what I’m used to and that’s telling me that there is another perspective that I need to understand. It’s not like the other one is telling me something strange, where I can write just one report, as we are seeing that human behaviour makes the difference in each community around how they view money, finance and banking.

CS: Did you pick up any vibes from your interviews around the world about attitudes towards cash, because everyone I talk to these days is saying “I don’t like cash anymore because it’s dirty, it’s got germs”?

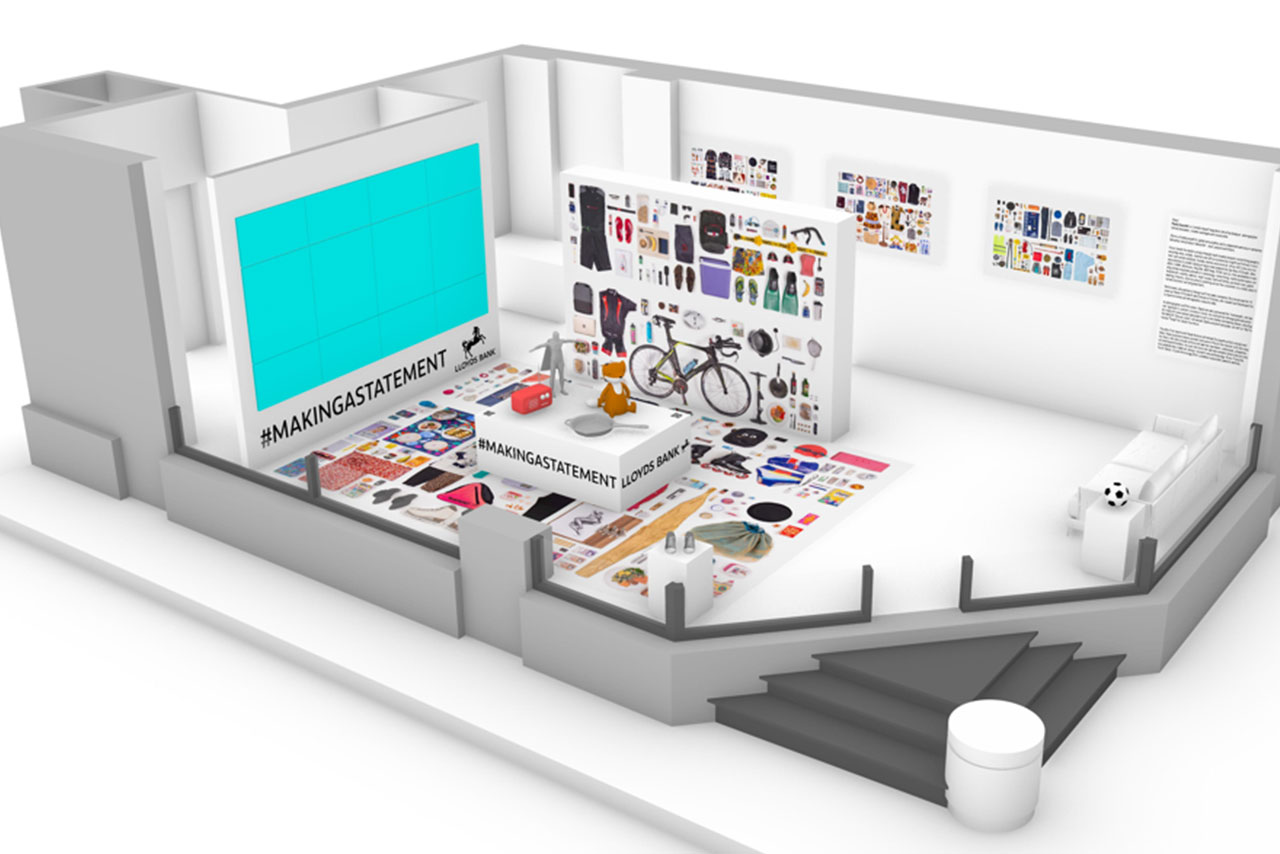

PZ: It’s incredible, it just became not convenient for everyone. The germs spreading around when COVID19 happened meant that many people told me they no longer wanted to use cash . This was true everywhere from Norway to Nigeria. Because of COVID promoting the avoidance of cash there has been a movement driving that way, but that movement was there even before COVID. It means that all shops and other places taking payments can do so everywhere, for example street vendors in Africa taking payment in the form of QR codes. So, a lot of things were driving people away from cash before COVID, but COVID just sped it all up. It just meant that contactless and QR payments became very convenient and could be taken on main street and the corner shop. It was just better. We had conversations where, in some developing nations, that is still not the case. Places like Brazil are cash heavy . But going back to Making a Statement, the aim was more to discuss what people were trying to buy than what they buy with. It was visualising everything from their mainstream purchases to their guilty pleasures. It is visual storytelling that we rarely relate with.

CS: How did you come up with the idea of visualising a bank statement?

PZ: The idea is based on the original concept that I published in 2015 in a book called Everything we touch. That book tracked people around the world for 24 hours and asked them to record everything they touched that day from dawn to dusk. By showing you everything they touched you could see their different cultures and activities, and that’s the original concept. Then the team behind Making a statement wanted to take that idea of everyday objects in somebody’s life through a bank statement. The idea is that each statement shows a month of someone’s life. So imagine if I’m doing a photograph of your bank statement, it would be replicating your bank statement. So bringing back to a bigger artwork you will find the pair of jeans or the pair of shoes that you invested in, next to mothkiller that you bought in the supermarket that you don’t even think about.

CS: You should patent that idea as everyone is now going to copy it. Over the next few years what do you think financial institutions should be thinking about with ethnography.

PZ: You know the Lloyds Bank activitation was the team actually thinking about how they can encourage customers to think differently about their financial behaviour and to have a better relationship with money. Engaging with your statement in the app or online was the idea, and that helps to engage customers in a conversation . With regards to the wider question, the challenger banks understand the conversation in the way that they approach consumers. They understand the dialogue that needs to take place, and they are understanding when people want to be bothered and when not. In the future there is definitely something there to be gained in a visual way to engage with customers and their experiences. For the next few years it’s about giving people knowledge.

-- END –

I find it interesting when meeting ethnographers. Do you know any? Ethnographers created the Egg card and Zopa; ethnography is a key backbone of IDEO, a global design and innovation firm; ethnography is all about life. Money is part of life, but it’s not our lives. It’s the enabler to live our lives. We need to remember that and visualise the things that mean something to us – not things that are generic, homogenous and impersonal. That’s ethnography for you!

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...