Following on from my discussions of solutions versus product people and vertical alignment versus horizontal, the question came up as to how to think strategically.

How can you really get inside the customer’s head?

What keeps the CEO awake at night (literally in the case of Lloyds Banking Group)?

And all those other strategic account questions which, if you could answer, would give you a real inside track lift to become more of a trusted advisor rather than product pusher.

This is a question I’ve dealt with for a long time and is why I do what I do.

I’ve also answered this question, thanks to reading management practitioner’s books and theories for years and implementing these ideas in reality.

Starting with In Search of Excellence and through Reengineering the Corporation to the Disciplines of Market Leaders, the Innovator’s Dilemma, Blue Ocean Strategy and The Experience Economy, I’ve pretty much seen ‘em all and done ‘em all.

Now we talk about customer-centricity, engagement banking and Bank 2.0.

I’m not saying these things aren’t useful – it’s always good to have some assistance in thinking clearly about change and how to change – but most of the management fads all boil down to the same thing: basic common sense thinking.

Y’know, Management By Walking About was one of the fads of its time.

Surely, managers should walk around their business and see what’s going on?

Process Improvement has been a big focal point.

What do you want? Processes to stink and get worse?

It’s all common sense.

So here’s my common sense way to get inside the head of your C-level client contact.

First, use future thinking to see what pressures are out there to challenge them.

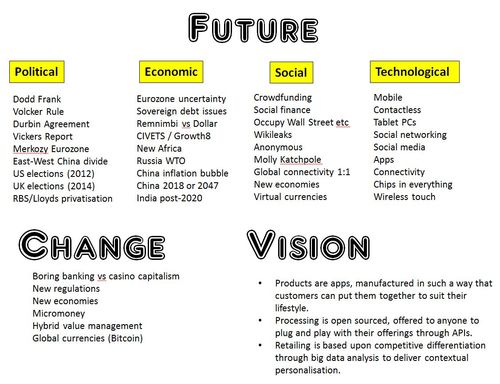

I use forces of change for this based upon the simple acronym: PEST.

PEST represents the Political, Economic, Social and Technological changes over the next 3-5 year horizon that may seriously impact the client’s business, as outlined yesterday.

In banking, you can put these together into a generic (non-exhaustive) shortlist as follows:

POLITICAL FORCES FOR CHANGE IN BANKING

- Dodd Frank

- Volcker Rule

- Durbin Agreement

- Vickers Report

- Merkozy Eurozone

- East-West China divide

- US elections (2012)

- UK elections (2014)

- RBS/Lloyds privatisation

ECONOMIC FORCES FOR CHANGE IN BANKING

- Eurozone uncertainty

- Sovereign debt issues

- Remnimbi vs Dollar

- CIVETS / Growth8

- New Africa

- Russia WTO

- China inflation bubble

- China 2018 or 2047

- India post-2020

SOCIAL FORCES FOR CHANGE IN BANKING

- Crowdfunding

- Social finance

- Occupy Wall Street etc

- Wikileaks

- Anonymous

- Molly Katchpole

- Global connectivity 1:1

- New economies

- Virtual currencies

TECHNOLOGICAL FORCES FOR CHANGE IN BANKING

- Mobile

- Contactless

- Tablet PCs

- Social networking

- Social media

- Apps

- Connectivity

- Chips in everything

- Wireless touch

Once you have this picture, it’s quite clear to see the landscape of challenges for the CEO of most banks, and how they must change:

SUMMARY CHANGES IN BANKING

- Boring banking vs casino capitalism

- New regulations

- New economies

- Micromoney

- Hybrid value management

- Global currencies (Bitcoin)

Leading to some form of vision in banking, vis-à-vis my prior blog entries about APIs and apps:

VISION FOR FUTURE BANKING

- Bank products are apps, manufactured in such a way that customers can put them together to suit their lifestyle.

- Bank processing is open sourced, offered to anyone to plug and play with their offerings through APIs.

- Bank retailing is based upon competitive differentiation through big data analysis to deliver contextual personalisation.

This pretty well summarises the basics of how I work with some banks on strategy, and some technology firms on strategic account planning:

The trick then, and the harder question for the bank or the strategic sales director, is to pin down how all of this translates to their organisation’s strategy.

What will this bank need to change, and which solutions will guarantee to deliver this change for them on time and at the lowest risk?

I would share more, but this is the stuff that is the basics of creating bank strategies and strategic solutions sales … probably something that will become a basic training process over time.

Maybe it should be today?

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...