I was asked to talk about the role of social media in banking this week, and was a little irritated by the question.

Why?

Because social media has a very strong role in some banks.

Take any large American bank and they’re blogging, twittering, facebooking and more (Wells Fargo, Citi and Bank of America being good examples).

Take many of the Asian banks, and they’re doing the same (Siam Commercial Bank, Standard Chartered and Commonwealth Bank of Australia being good examples).

And in our own hemisphere, banks from Russia to Spain are doing interesting social stuff.

Then we come to the UK.

Bah, humbug!

Who needs to be social.

The reason I mention it is that sure, First Direct and Barclaycard have done some interesting online social services, but the core mainstream UK banks are seriously deficient in a major way.

Not one of them has an official company blog or, if they have, they’ve hidden it.

This is because I researched a little bit for my presentation by seeing if any of them had one.

And they haven’t.

Now I was reminded of this because, five years ago, I introduced a leading UK bank to Wells Fargo’s Head of Experiential Marketing, Tim Collins, to discuss social media.

Tim was already well into blogs and virtual worlds, and was expanding the bank’s footprint into facebook at the time.

They asked him why he bothered?

His answer was simple: “if you’re not part of the social world of conversation amongst your customers, then they will talk about you negatively and you have no voice to respond. If you engage in the online conversation, then it becomes far more civilised, interactive and interesting.”

There were lots of things discussed.

For example, the UK bank said they tried an internal blog for three months but got so much negativity they shut it down.

Tim responded by saying that Wells Fargo had the same thing from customers at first but, by having a team monitor their social media 24 by 7, they always responded to any negativity straight away with a response explaining why it happened that way.

Customers were far more polite and calm when they saw their rude postings garnered a civil reply; hence it led to being engaged in a conversation. Through conversation, the bank learned a lot more about what frustrated customers. The result is better products and services.

However, it is quite clear that the bank cannot engage in such activity half-heartedly, as you need to be responsive and therefore have people dedicated to social media interaction.

Like a call centre, it’s a response team to online questions and issues.

He also said that now other customers often reply to rude postings, and that their best service agents are their own advocates.

I hear this from many other banks now too.

Finally, Tim talked about the reasons why they first got into social media and it was in part related to one customer who had created a website called wellsfargosucks.com.

Unfortunately, that website came up as the first result in any google search.

Therefore, in order to ensure the right image of the bank was presented, the bank sees social media as a key method of moving the right message to the top of the search results rather than leaving it to negativity from media or anti-bank activists.

So now I come back to my UK bank social media research.

Here’s what I found.

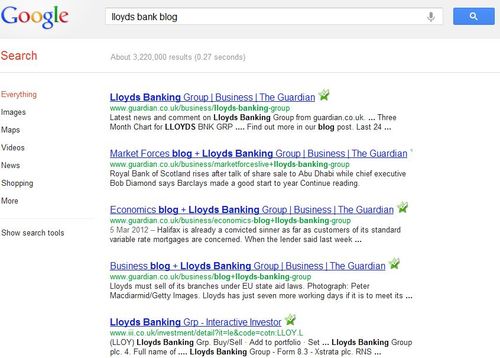

Lloyds Bank – no blog, and mainly investor discussions.

HSBC – no blog, one negative headline in top five search headings.

Santander – no blog, a few negative headlines but at least they put an advert against their name.

Barclays Bank – no blog but great search results!

NatWest – oh dear, dear, dear.

At least Lloyds and HSBC have some blogs related to graduate recruitment. Still a poor show, but better than nothing.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...